COP 28: fossil fuel subsidies - will history repeat itself?

COP 28 will revive an old debate about subsidies, it is a vital signal to read

COP 28 is just around the corner. On the 30th of November, heads of state will gather once more to discuss a shared vision of global climate action. This time they will be hosted by the UAE – one of the world’s most oil-rich regions.

The relevance of COP to investment decisions is obscured by its reputation of being a slow-moving political scuffle. Yet, it is far from obsolete. Decisions taken at COP indicate political will or the lack thereof, they are signals that markets will read, interpret and respond to.

Of all the signals COP could send to allocators of capital – few exceed the weight of subsidies. Signals can be green (renewables subsidies) or red (fossil fuel subsidies) and in recent years, governments have thrown their weight behind both. In this subsidies, Net Zero Investor takes stock of these signals and why they matter for investment decisions.

In this feature, the focus is on fossil fuel subsidies – which surged to a record high of $7 trillion globally last year.

Catching the bounty

In some way, shape or form – subsidies have been around since the 18th century. “Bounties” as Adam Smith referred to them. Their modes, intensity and targets changed over the years, but their fundamental features persist – they represent a state-led market intervention designed to protect and promote. Financial transfers or benefits are the most common form – tax breaks and price support for instance.

Notably, by protecting and promoting, they are prone to lobbying and influence. Adam Smith, in his analysis of Scottish fishing subsidies in 1750 quipped:

“It has, I am afraid, been too common for vessels to fit out for the sole purpose of catching, not the fish, but the bounty”.

In other words, subsidies are significant economic incentives that corporates respond to. Subsidies can have several negative consequences – including a significant fiscal cost and a distortion of economy-wide incentives to decarbonize.

Why and who do governments subsidise?

Fossil fuel subsidies have a variety of motivations and consequences. Typically, they have been used to shield consumers from energy price inflation. Consumer subsidy programs often surge as a response to an energy crisis.

2022 was no different. National responses to energy price inflation following Russia’s invasion of Ukrain meant a global fossil fuel subsidy roll out of $7 trillion – more than government spending on education or health.

One approach to understanding subsidies is to look at the target energy source. The more a fossil fuel source is subsidised, the harder it is to phase it out.

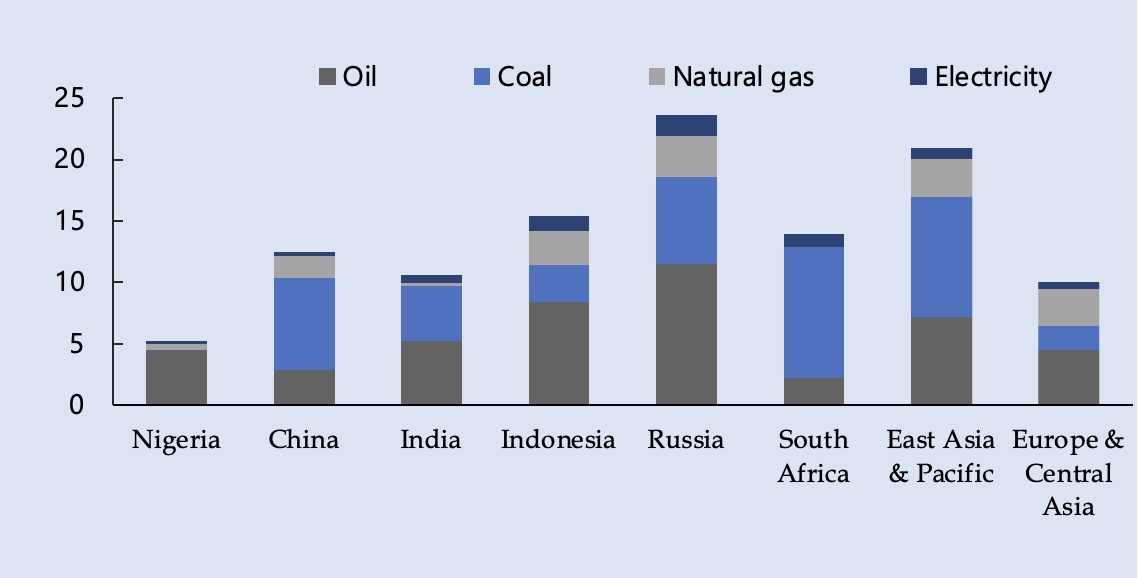

In the chart below plots subsidies for a sample of countries – each of which have a fairly fossil-fuel intensive energy mix. Oil and coal tend to account for an overwhelming share of the subsidies. In Brazil, India and Indonesia – oil subsidies exceed coal. In China and South Africa – the opposite is true. Chinese coal subsidies in 2022 amounted to 7% of its GDP ($1.3tn).

Dilemma of dichotomies

The challenge for any COP presidency is that a vision for climate action has been anything but shared. Ever since its first meeting in Berlin in 1995, the COP mechanism has been riddled with division. Consensus on phasing out fossil fuel subsidies is stubbornly elusive and politically expensive.

COP is a conflict of dichotomies – developed vs developing and energy importers vs energy exporters. Developing countries disagree with developed ones on whether the responsibility for emissions is current or historical. Developed countries, by some estimates, are responsible for 79% of historical emissions. Developing countries are responsible for 63% of current emissions.

Politicians from net energy importing countries want to shield consumers from high energy costs, the exporters might want to protect producers. Moreover, a politician credited with lower energy prices is likely to stay in office for longer. Which means reducing fossil fuel subsidies is not politically popular.

When COP 26 President Alok Sharma delivered an apology two years ago – he did so following a breakdown of negotiations on phasing out coal. China and India had pushed for a change in language. “Phase down”, they said, is the best they could do.

This time is different

Ultimately if governments support, for reasons as varied as they come, their fossil fuel sectors – the investment case for renewables takes a hit. The future profitability of renewables depends quite heavily on what politicians expect their energy grid to look like in the long term.

The problem however is that project life-cycles exceed political ones. The average solar farm has an expected life cycle of over 25 years, the average politician occupies an office for five.

There is, however, a glimmer of hope. The International Energy Agency in its 2023 flagship report observed that this time around, the energy crisis led to increased momentum in clean energy investment. Large emitters like China significantly expanded their renewables deployment. The EU is now confident that renewables will make it more energy secure than fossil fuels ever did. Several countries have rushed to incentivise clean energy investment in a quest to keep up with the American IRA. Perhaps this time is different.

At the end of COP and all throughout, a signal will be transmitted from the UAE. It could be red, as it was in Glasgow, it could be green, as the IEA predicts or it may well be amber – a mixed signal on why and who governments subsidise.