How to navigate the profit problem in sustainability

Reaching out to pension holders and understanding membership demographics may help ease the tension between long-term and short-term fiduciary duties

Understanding the relationship between sustainability factors and returns can play a critical role in capital allocation decisions.

While a study from Morgan Stanley found that “sustainable equity funds” outperformed regular funds by 4.3 percentage points in 2020, Reuters reported that ESG funds fell 9.2% in January 2022, against a 5.3% drop in the SPX, driven mainly by declines in the tech sector.

A study from Vanguard Funds found that “ESG funds have neither systematically higher nor systematically lower raw returns or risk than the broader market.”

Fidelity found that ESG Funds outperformed the market by a small margin, though they note that there’s no assurance that this will continue.

At the more negative end of the spectrum, an article in Harvard Business Review claims that ESG funds generate inferior returns.

These mixed reports suggest that sustainable investments may not always deliver superior results – at least in the short term and under current policy frameworks – and can depend on specific factors, such as declines in the tech sector.

Fiduciary duty

Sometimes a lack of clarity over a pension fund’s primary fiduciary duty can hold back capital allocation in positive impact projects that have a more complex risk-return profile.

For example, the ongoing LGPS Consultation on Investments underscores the UK government's desire for Local Government Pension Scheme (LGPS) Funds to increase their investments in Levelling Up and Infrastructure projects.

While the consultation acknowledges the fiduciary duty of Pension Fund Committees in making investment decisions, money management sources suggested that without clarity on their primary fiduciary responsibility, caution may hinder decision-making, limiting opportunities for local investments with broader community benefits.

At Net Zero Investor’s recent DC roundtable, asset owners said their main duty was not to maximise profits but provide a reasonable risk-adjusted return.

This begs the question: how can long-term asset owners aim for long-term sustainability without compromising their fiduciary duty?

Consensus among pension holders

For some pension funds, the answer may involve reaching out to pension holders and gaining a consensus that a pure short-term profit motive shouldn’t be the determining factor in a capital allocation decision.

Such is the case for Australian Ethical, an investment management and superannuation fund that surveyed its constituents to find out the extent to which they would accept a potential reduction in returns to guarantee that investments would cause no harm to koala bears.

The firm recently divested from Lendlease over concerns a planned housing development in south-west Sydney threatened the koala population.

Demographics may facilitate consensus building. Just over half of REST members are under 29-years old, which means REST has an unusually strong imperative to ensure long-term risk management and a liveable world for its pensioners. That can give it more flexibility to prioritise sustainability.

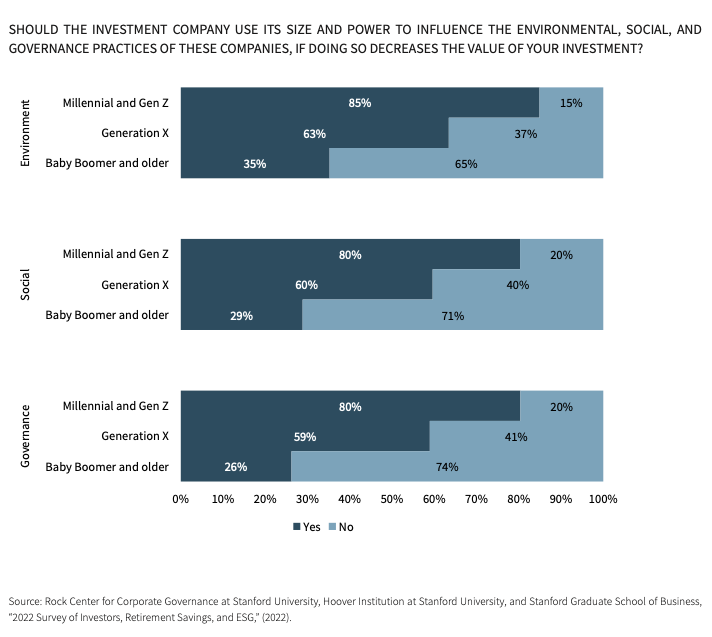

Millennials and Gen Z are more likely to prioritise ESG factors in investment decisions, as many surveys in recent years have demonstrated. Results from the below survey suggest that younger generations tend to worry less about whether ESG investments are profitable or not.

Hans Stegeman, chief economist at Triodos, notes that a short-term profit-oriented economy “may continue” for another ten years before some terrible ecosystem collapse provokes a financial crisis.

“If we don't give up short-term returns and invest more in sustainability, then we go into collapse mode,” he said.

The problem, he adds, is that the purely profit motive continues to be a powerful driving force for capital allocation decisions, even when climate change and ecological crisis are unavoidable. Asset owners urgently “need to discuss their fiduciary duty with their participants, clearly communicate the difficult reality, and make some hard investment decisions that align with their members’ expectations”.

This might take the form of a relatively binary either/or question: “Do you want short-term returns that compare with the historical average but could be risky in the long-term and worsen the poly-crisis era? Or do you want to invest in a future that supports radical decisions and actions but might have lower short-term returns?”

Positive and negative externalities

System change would help support sustainability-focused capital allocations. There has been much debate around pricing in negative externalities, such as pollution, into the economy, as a way of ensuring policy support for sustainable business models.

Pricing in positive externalities is another attractive option for Jacqueline Jackson, head of responsible investment at London CIV.

“For investors, sustainability still needs to be investable,” she said. “This is where policy could come in.”

If a company creates positive social value, and that can be measured in a robust way, then governments could reward those companies in ways that are either financial or non-financial to ensure those solutions remain investable.

For example, a company that creates health benefits will end up reducing health service costs. That cost saving to the government could be remunerated in some way, such as through subsidies.

“It doesn't make sense that governments wouldn't reward companies that create a social benefit, especially when those benefits create real cost savings for local authorities,” she added.

Thinking beyond profit

Stewart Wallis, former international director of Oxfam, and chair of the Wellbeing Economy Alliance, told Net Zero Investor, that profit considerations need to extend beyond the balance sheet.

“In Alberta, 7% of the population live in poverty, creating an estimated annual cost of 9 billion Canadian dollars,” he said. That same Canadian province also has a 9 billion Canadian dollar bill annual bill for air pollution and another 9 billion for extreme weather events. These numbers illustrate the large sums that already being expended because of “systemic mismanagement of the economy”.

Furthermore, the legacy costs of clearing up tar sands already stand at around $260 billion and are likely to rise.

Wallis is adamant that system change is urgently needed to address this mismanagement. “Aiming blindly at GDP growth, no matter the cost, is not a viable or sensible strategy,” he added.

Public versus private

Making publicly listed companies less profit-oriented can be challenging, sources said.

“The shareholder logic intensifies the pressure to maximise profits,” said Katrin Wohlwend, sustainability project manager at ABS bank. “Failing to meet to shareholder expectation can ruin a company.”

Wallis said family companies and privately-owned companies tended to have wider objectives than listed companies. The problem with a listed company Is “the whole way the finance system pushes them”.

“A listed company pursuing wider ethical objectives is at the mercy of its current shareholders,” he said. There are several examples of listed companies making a profit for many years while pursuing wider objectives, but when hedge funds and different shareholders get involved, overnight the whole ethos can change.

For Wallis, the ultimate solution to the profit problem in sustainability is for asset owners to invest in system change, to back governments and policies that aim to achieve sustainability goals.

With the right kind of policy frameworks in place, there's no reason why asset owners “can't make a reasonable return and probably a safer return”.