Jason Fletcher on climate investment: aligning government policy with investor aspirations

Jason Fletcher, former CIO at London CIV examines how the next UK government could scale up investment in the energy transition

The UK has a general election coming up, which is widely expected to be held at the end of this year. Regardless of its outcome, it is likely that our next government will want UK asset owners to invest more in renewables and productive capital.

Surely this aligns with the long-term aspirations of asset owners and the Great British public. We ought to come up with a solution that delivers a more robust domestic economy, better planet stewardship and decent pensions for our workers in old age. What lessons can we all learn from previous investment booms and from other nations’ investments in renewables? Will long-term investors make decent returns from renewables and the energy transition? Which mandates, policies and nudges should the government be applying to investors and vice versa?

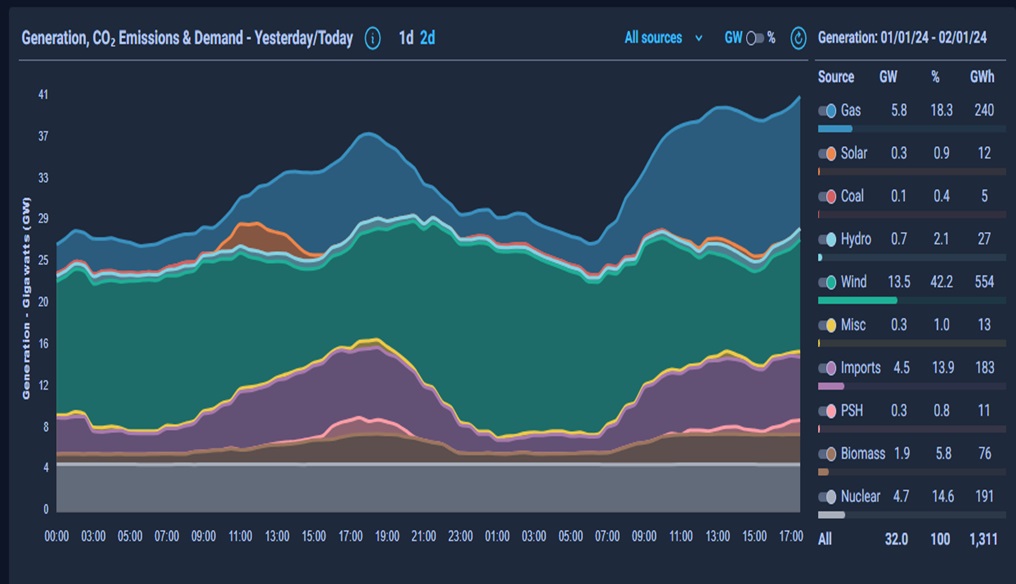

The UK generated 38% of its electric power from renewables in 2022 up 5% from 2021 (broken down as wind: 26.8%, solar: 4.4%, Biomass: 5.2% and hydro: 1.8% source: LSE / Grantham institute). On sunny, blustery spring days in 2023, we proudly generated 80% of our electricity from renewable sources Wind and solar now vie for the position of cheapest sources of electricity and will no longer rely on government subsidies.

Overall, the UK has performed relatively well in its transition to renewables. The leading nations for renewable generation are Paraguay 100%, Namibia 100% and Iceland 100%, all places which have a natural advantage in thermal or hydro power. But the UK’s renewable generation at 38% is ahead of the developed world at 28% including biomass and excluding nuclear.

The UK leads in wind generation playing to our natural advantage of consistent winds. We also arguably invented electricity generation with Michael Faraday’s demonstration of the electric motor in 1821 which is also testament to the leading research that our universities still provide. The renewable sector in the UK employs 250,000 people (skillset transferred from generating electricity from the North Sea fossil fuels) and currently amounts to £70bn of GDP.

Despite these successes, we will struggle to meet our 100% renewable target by 2035 unless we see substantial new investment into the energy transition. Sadly, this expansion has slowed recently due to new oil and gas field licenses, un-favourable tax/subsidy changes and the delays of planning consents and grid investments. Planning permits are a very British problem (NIMBYism and the crown estate) that we need to resolve right now. According to the BBC, we have £200bn of renewable investment capacity that may need to wait up to 10 years to get connected to the grid. This is a common challenge shared with other nations struggling to retrofit grids for these new sources of energy. Providing enabler technology could be where the UK could get a competitive advantage in grid technology, utility battery and pump storage.

RENEWABLE INFRASTRUCTURE SUMMIT

12/03/24, London | Asset owner knowledge sharing & due diligence

Will investments in renewables and energy transition be profitable or productive? Let’s consider the investment boom in aerospace following the first flight in 1903. The Wright brothers did not make much money from their exploits, they had countless crashes taking considerable personal risk and had the backstop of family wealth to continue their research and development. Their first financial contracts/venture investments came from the US Army and a French engineering consortium. They only got patents for the flight control system which were in dispute up to 1920 long after Orvill sold the company. They made some money from licensing and pilot training schools. Most of the investment in Aerospace came from the Military and the space programme in the US. Lessons to be drawn from this are that to be successful you need to take early venture risk, focus on your competitive advantage, research, training, services and parts. Whatever you choose you need to be in it for the long run.

Given the COP28 pledges, the rest of the world will also be racing to add renewables using both private and public capital. The US has pledged U$700bn in their Inflation Reduction Act (IRA). The United States’ competitive advantage is in its domestic market, research and development and the willingness to invest in early-stage venture capital. It was a leader in thin film solar (First Solar) and EV cars (Tesla) but has lost out to Chinese manufacturing prowess in both these industries.

China is not only the biggest power user in the world, it also dominates in renewable manufacturing. The UK cannot and should not compete with these two monoliths. We do not have U$700bn spare to spend and will never compete with the Chinese manufacturing efficiency. We and others have focused on giga (“ginormous” sounds much more immense) battery plants for the auto sector. The UK needs be cautious here unless there is a local market or transport barriers (windmills are now the size of St Pauls and not easy to transport around) that make local manufacturing worthwhile. Focusing on the auto sector is also a crowded market, perhaps we should be looking elsewhere at enabler technologies and services.

The biggest hurdles to a brighter future in the UK are limited investment in early-stage research and development and planning restrictions. The British low-risk appetite is also a concern. Government and investors need to have skin in the game on the upside and downside. The government also needs to encourage risk-taking through tax and allowances. More importantly it needs to protect risk takers (the Wright brothers had family wealth to fall back on) as we know that entrepreneurs need to be able to withstand failures before they hit the jackpot.

From an investor perspective, key investment hurdles are the definition of fiduciary responsibility and government tinkering. Some investors argue that adopting ESG objectives conflicts with their fiduciary responsibility disregarding risk and the long term. To me global warming is a financial risk in the long run. Quite apart from that is the question whether we actually have a world to retire into. Investors need stability from government, so I would urge whoever is in charge at the end of this year to stop changing the rules and tinkering with taxes and incentives.

The main risk is that we invest in something that is unprofitable, unproductive, or where we do not have a competitive advantage. However, taking no risk at all will end in global warming and a smaller economy (the full lose-lose!) We need to leverage our research capability capturing the value add and employment through licensing and sharing our expertise, rather than simply selling our best ideas to the highest bidder when it becomes viable. To get UK funds to invest more in UK productive equity/ energy transition assets (thanks to Canadian and Australian investors for holding the fort here) we need to reverse the reduced DC contribution rates from employers and ensure that DC superfunds have the confidence to invest for the long-term.. We need to limit the switching/ cash out options to ensure that members and funds are aligned in investment time frame. The government would also help by offering more efficient legal structures for investing in private and venture capital.

The UK needs to carve out our competitive advantage in wind generation, university research, enabler (battery and grid management) and new technologies. We need to think long term beyond the end of the next two elections and ensure that government and investors are nudged in the right direction with incentives that support the energy transition. Support can come in the form of “carrots” (allowances and tax breaks) but also the “stick” of carbon taxes. Both actions would ensure that we can properly assess the real long term, risk-adjusted return after cost of new oil and gas projects.

Taxing carbon emissions and integrating into the carbon credit system would be a powerful nudge. A “ginormous” benefit would come from re-investing that carbon tax into the UK energy transition perhaps focused on grid technology. Taxing imported carbon emissions (EU 2024 and UK 2027) would also ensure we have a level playing field with domestic manufacturing and in the interests of fairness ought to be invested into emerging nations renewables remembering that climate change is a global not a local issue.