SEC ‘no action’ requests: the justifications

How do companies justify avoiding a climate-related shareholder proposal?

No-action requests are mechanisms through which companies notify the SEC of their intention to avoid a shareholder resolution at their annual general meetings. Since January 2023, 19 no-action requests have targeted climate related shareholder resolutions.

In a series of articles, Net Zero Investor is focusing on three pieces of the puzzle: the proposals, the justifications and the SEC’s response.

Having covered an overview of the key topics among no action requests, part two of this series focuses on justifications.

According to US regulations, companies can only avoid discussing a resolution under limited conditions. Moreover, companies must demonstrate why their case fits these conditions. It is these justifications that the Securities and Exchange Commission (SEC) examines closely.

Interestingly, the success of justifications varies – some are more convincing than others.

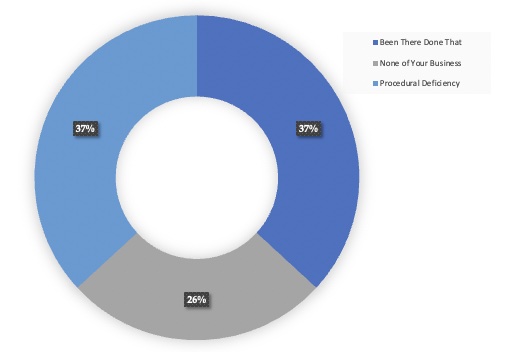

Procedural deficiency

Let’s start with the justification that has been relatively successful in keeping climate change away from AGMs: procedural deficiency.

Submitting a shareholder proposal is anything but straightforward. It requires compliance with a wide range of rules. Small margins of error can make a large difference.

One such rule specifies that shareholder resolutions must be submitted along with proof of beneficial ownership. This usually means that the filers of the proposal must have held a certain amount of stock for long enough.

If their ownership cannot be established, companies write to the shareholder asking for proof. This is known as the “deficiency notice”. The Shareholder must send over credible proof within 14 days. If not, companies are permitted to avoid the resolution.

Last week’s edition of this series mentioned technology solutions provider CDW Corporation’s journey down this road. American “corporate gadfly” John Chevedden’s proposal about climate lobbying was successfully removed from the AGM agenda. The reason? Chevedden’s proof of ownership arrived 15 days later. Which technically, is outside the 14-day window.

The SEC agreed. “Whether or not the proof of ownership letter is sufficient proof is irrelevant, because it was sent to the company more than 14 days after the date the deficiency notice was delivered”, it concluded.

Several companies have used procedural deficiency to justify avoiding climate-related shareholder proposals. Among them: Chevron, CDW Corporation, CNX Resources, Exxon Mobil, Levi Strauss, NextEra Energy and United Parcel Service. Over 50% of them have done so successfully.

Been There, Done That

Another tactic companies have used is to say that the issue has already been addressed. The rule, Rule 14a-8(i)(10), states that if a proposal has already been “substantially implemented”, it need not be discussed at the AGM.

It was put into place back in 1970s. At the time, the regulators felt it was prudent to “avoid the possibility of shareholders having to consider matters which already have been favorably acted upon by the management”.

Utility company Ameren is among a group of seven companies that have used this justification to avoid a climate-related shareholder proposal.

The shareholder proposal at Ameren asked the company to disclose scope 1 and 2 emissions reduction targets aligned with the Paris Agreement. Misalignment, says the proposal, could be a costly strategic error.

“Following the passage of the Inflation Reduction Act in 2022 more investment in clean energy sources is likely. However, Ameren currently plans a generation mix dominated by fossil fuels well into the future”, the proposal reads.

Ameren argued that since the proposal asked for emissions reduction targets, it has already been addressed through numerous company documents. However, the SEC found that the proposal was not as much about disclosing targets at it was about the alignment of the targets.

As part of its judgement, the SEC attached evidence of misalignment. It concluded that:

“[Ameren’s] use of its 2005 emissions as a baseline is a fatally flawed effort to rationalise less aggressive near- and medium-term reduction targets, which cannot reasonably be seen as aligned with sectoral pathways”.

For the most part, the SEC has not bought the logic of this justification. In only one case (American Tower), has the SEC agreed with company management. Here too, the question was about alignment.

[Ameren’s] use of its 2005 emissions as a baseline is a fatally flawed effort to rationalize less aggressive near- and medium-term reduction targets, which cannot reasonably be seen as aligned with sectoral pathways

None of Your Business

Finally, some companies have argued that the proposal deals with an issue that is not for shareholders to decide.

There is some basis for this. Corporate governance rules in the US place certain tasks under the purview of company management. Effectively, this means they fall outside shareholders’ oversight. This is known as the “ordinary business standard”.

Amazon has used this justification to avoid a proposal that asks management to report the carbon footprint of its employee pension plan. Amazon’s 401 (k) plan manages over $17 billion. According to company management, if shareholders decide how these funds are managed, it would amount to micromanagement.

The SEC disagrees. In the SEC’s view, the proposal is not about pension plans, it is about climate change. “As such, the focus on the retirement accounts’ impact on climate change and the impact of climate change on the employees as retirees, transcends ordinary business”, the SEC concluded.

Insurance groups The Travelers Companies and Chubb have also used this justification. Here too, the SEC did not agree.

This justification is by far, the least successful.