Managing the manager: Spirit Super’s path to emissions reduction

Revising asset management mandates is becoming an increasingly vital part of transition planning.

Spirit Super is one of Australia’s smaller asset owners – the super fund manages about $27 billion and has 335,000 members. Other superfunds typically have larger portfolios – Cbus Super and Hesta Super manage well over $48 billion. AustalainSuper and UniSuper both manage over $65 billion.

Yet, despite its smaller size the fund has big emissions reduction plans. In 2021, Spirit Super set an ambitious target: reduce emissions intensity of the investment portfolio by 50% before 2030.

The scale of the ambition reflects the Spirit Super’s self-image: “big enough to make a difference and small enough to care”.

In its latest market update, the fund said its ambition was anything but misplaced. It claims to have made significant progress in reducing financed emissions across scope 1,2 and 3. Spirit attributed progress to “investment decisions”.

The fund’s chief investment officer Dr. Ross Barry told Net Zero Investor what that meant. At the heart of his fund’s progress are two factors: a scrupulous revision of asset manager mandates and increased asset allocation into renewables.

.......we’ve collaborated with managers to explore ways in which they can reduce our attributable emissions without materially impacting the scope of their stock selection activities and alpha expectations

Their Approach, Our Needs.

As the 2030 date moves closer, the mandates that shape how asset managers invest an asset owner’s capital is proving to be an ever-so-critical piece of the puzzle.

In May, Faith Ward - chief responsible investment officer at Brunel Pension Partnership took to LinkedIn to put the asset owner – manager relationship under the scanner.

“We will be particularly focussing on how managers have voted at key AGMs in Europe as proof points for our understanding of their approach and our needs”, wrote Ward - who also serves as the chair of the UK Asset Owner Roundtable.

Ward’s words raise an important point – a manager’s approach might not necessarily reflect an asset owner’s need - particularly those related to emissions reduction.

The two face different incentives to alter portfolios, often driven by a difference in investment horizons. A difference of horizons translates quite unsurprisingly into a difference of appetite and approach.

At Spirit Super, revising asset manager mandates were a key part of reducing financed emissions.

“This [emissions reduction] is primarily due to revisions to some of our listed equity benchmarks and several mandates where we’ve collaborated with managers to explore ways in which they can reduce our attributable emissions without materially impacting the scope of their stock selection activities and alpha expectations”, said Dr. Barry.

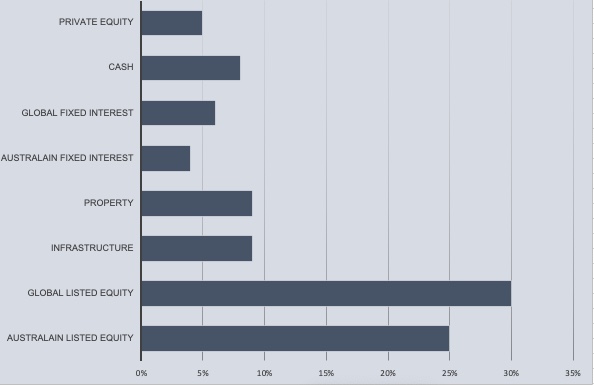

Spirit’s Allocation Mix

Spirit Super offers its members six investment options to choose from, all of which are pre-mixed. One of these is the “sustainable” option. The fund says the option is best suited for those with an investment horizon of over seven years and a moderate appetite for risk. In return, members get a responsible investment-led portfolio, more than half of which is allocated to equities.

Spirit Super’s board approved an ESG policy in March 2023 wherein it outlined its investment beliefs. The policy conveys the board’s optimism about investing in and focusing on decarbonisation.

“One of these beliefs is that the Trustee should be a responsible, active asset owner and to play a leadership role if and where it has sufficient capability and conviction”, the plan notes.

If and where has largely boiled down to here and now. In recent years, the fund has expanded its exposure to renewables assets both at home and abroad.

In 2021, through an IFM global infrastructure consortium, the fund invested in Naturgy – a Spanish utilities company with a renewables pipeline of 25GW across wind, solar and hydroelectricity.

Through its “impact investment” platform, Dr. Barry says the fund will further increase its allocation to renewables:

“Another key area of reduction has been from carbon abatements associated with our growing renewable energy generation and storage portfolio and other transition-oriented investments across our broader impact investment platform”, he says.

At least 15% of Spirit Super’s portfolio will be allocated to impact investments. It is hard to imagine that asset management mandates will not be part of this conversation too.

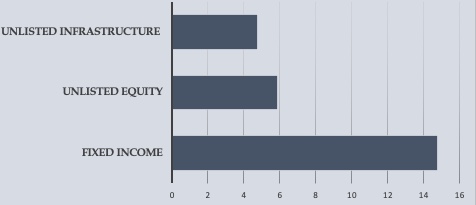

The data below shows that for fixed income, unlisted equity and unlisted infrastructure – external managers play a key role in the “sustainable investment option” portfolio.

The asset owner – asset manager relationship is riddled with what economists refer to as the “principal-agent” problem – aligning incentives of managers with the expectations of asset owners is arduous and far from plain sailing. Yet, as the Spirit Super example shows, reimagining mandates and monitoring the results is now being seen as part of what it means to be an active owner.