No-action requests: the SEC’s careful balancing act

Thus far, the SEC has primarily protected shareholder interests, making it harder for companies to avoid climate-related proposals

“Even gold medallists need to practice and hone their craft”, wrote the chairman of the Securities and Exchange Commission (SEC), Gary Gensler, as he outlined the body's latest strategic plan. The SEC’s craft is ensuring that everyone in the capital markets is playing by the rules.

In this three-part series, Net Zero Investor is investigating so-called 'no action' requests, a key component of the SEC’s regulatory craft.

No action requests are filed by companies when they intend to avoid a shareholder resolution from their annual general meetings (AGMs). Companies are only permitted to do so under limited conditions.

This year, 19 no action requests have targeted climate-related shareholder proposals. The previous edition of this series examined the justifications companies use. Part III focuses on the final piece of the puzzle: the SEC’s response.

The SEC can respond in two ways – it could either agree with the company’s justification or it could disagree and recommend an enforcement action if the company still goes ahead and excludes the proposal from its AGM.

In a way, the SEC’s response is aimed at striking a balance between shareholder rights and corporate governance. The balance is currently at 70/30, in favour of the shareholders. The SEC disagrees with company requests a lot more often than it agrees.

The 30%

Roughly a third of all no-action requests have received a positive response from the SEC. This means that the SEC agreed that there are reasonable grounds for the company to avoid a climate-related shareholder proposal.

As highlighted in Part II of this series, the SEC has tended to agree with the company when the request is submitted on grounds of procedural deficiency.

The grounds are less substantive i.e. it has less to do with the actual proposal and is focused instead on the procedure of submitting a proposal.

Non-compliance by a shareholder with rules that govern this procedure, often result in successful avoidance of climate-related shareholder proposals. Chevron, CDW Corporation, CNX Resources, Exxon Mobil, Levi Strauss, NextEra Energy and United Parcel Service have successfully convinced the SEC on such grounds.

However, procedural deficiency is not the only justification the SEC agrees with.

At insurance group Chubb, the SEC agreed that a climate-related shareholder proposal was micromanaging the company.

The proposal asked for phasing out underwriting of fossil fuel exploration projects in a bid to align the company with the goals of the Paris Agreement.

Chubb’s letter to the SEC reads, “the proposal seeks to micromanage the company by probing too deeply into matters of a complex nature upon which shareholders, as a group, would not be in a position to make an informed judgment”.

The SEC agreed. It amounts to micromanagement, it said, if the recommendation included a specific method of addressing the issue.

“A proposal may be excluded if it seeks to micromanage the company by specifying in detail the manner in which the company should address a policy issue, whether or not the proposal is considered to involve a significant social policy”, the SEC concluded.

The rule under question is known as the “ordinary business standard” and is a commonly used justification in no-action requests.

A proposal may be excluded if it seeks to micromanage the company by specifying in detail the manner in which the company should address a policy issue.

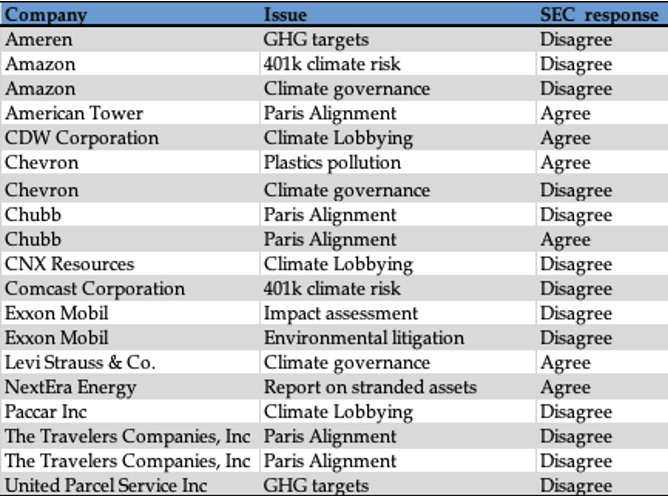

The 70%

The table below outlines the range of issues that no action requests have targeted and the associated response from the SEC. 70% of the time, the SEC has moved to protect the shareholder’s interest.

For example, the SEC has disagreed with fossil fuel giants who argued that the shareholder proposal was resurfacing an issue that has already been addressed.

At Chevron, shareholders proposed a new “board committee on decarbonization risk”. On its part, company management claimed that similar proposals were filed in 2019 and 2020, neither of which received significant support. The rules state that if a recent proposal that raises a similar issue received less than 15% of the votes, it can be avoided.

The SEC did not agree. In its judgement, the central claims of previous proposals were not identical i.e. the issue had not been substantially addressed in the past.

“The Proposal does not address substantially the same subject matter as the proposals previously included in the company’s 2020 and 2019 proxy materials”, wrote the SEC.

Allowing Exxon to exclude my proposal would represent a major blow to shareholders' rights.

At Exxon Mobil too, the SEC’ moved to dismiss the company’s claim. The proposal sought information on the risk that environmental litigation poses to the company. Exxon’s claim was that the filers of the proposal had exceeded the one-proposal limit.

The filers were Andrew Behar (CEO) and Anna Marie Lyles (Treasurer) of shareholder advocacy group As You Sow.

Since Behar and Lyes filed the proposal, Exxon Mobil made the case that it was “indirectly” filed by As You Sow, which had already filed a proposal.

In a letter addressed to the SEC, Lyes wrote “allowing Exxon to exclude my proposal would represent a major blow to shareholders' rights”.

Lyes’ letter speaks to a wider sentiment – excluding climate-related proposals from AGMs could constrain investor stewardship at the big polluters.

So far, the SEC has stepped in to prevent exclusion, but the balance between shareholders and companies is challenging to strike. Every instance of the SEC’s agreement, justified as it is, sets a precedent.

As this series has shown, it is not entirely unimaginable to expect companies to take note and maximise their chances next time around.

Gensler’s message is worth recalling – in order to find its footing, the SEC will need to practice and hone its craft.