Nuclear renaissance: net-zero solution or dangerous gamble?

An increasing number of countries and investors warm to the idea of more nuclear power but uncertainty around its role in meeting net-zero targets has reinforced old divisions

The EU sustainable finance taxonomy debates pitted pro-nuclear states like France against anti-nuclear states like Germany. It stirred controversy and brought questions around the future of nuclear energy into the public arena.

While some countries have opted out of nuclear power in light of safety and environmental concerns, others still see a strong role for nuclear in their energy transitions.

Ultimately, the EU included nuclear in the taxonomy, helping to bolster its status as a sustainable energy source.

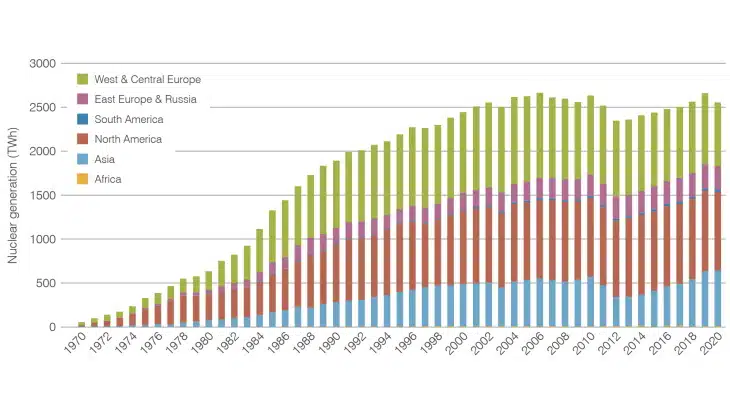

The EU debates exposed a trend that is both new and old: while various studies, such as the new Capgemini report, claim that nuclear power output needs to be tripled by 2050 to meet net-zero goals, there is still no universal consensus on even the basic role of nuclear in a clean energy system.

“We're in the middle of a nuclear renaissance, but the role of nuclear still isn’t clear and enthusiasm is patchy,” said Peter King, global energy transition and utilities lead at Capgemini. “Different countries are at very different starting points.”

Pro-nuclear countries like France, China, the US, India and Canada have announced plans to build new plants as part of their net-zero road maps.

According to Rystad Energy, investments in nuclear are projected to reach $46 billion in 2023, up from $44 billion in 2021.

Meanwhile many countries, such as Norway and Australia, which previously opposed nuclear, have started to warm to the idea of it, spurred on by the realisation that renewables may not be able to meet all their energy needs, especially in the power-hungry industrial sector.

The official International Energy Agency position is that nuclear, as the second-largest source of low-carbon energy today, can make a significant contribution to achieving sustainable energy goals and enhancing energy security.

Norway explores nuclear

A good example is Norway's sovereign wealth fund – the Government Pension Fund Global (GPFG) – managed by Norges Bank Investment Management (NBIM). In addition to engaging with portfolio companies that own conventional nuclear power generation assets, the fund is actively researching, analysing, and monitoring new investment opportunities related to nuclear power, both in fission and fusion.

Consisting of 70% equities and 30% fixed income, the GPFG’s equity investments span around 9,000 companies in numerous countries, industries and currencies all around the world, and include listed companies with nuclear power generation assets.

“NBIM does not have an official policy specifically related to companies with nuclear power assets but assesses them in the same manner as other companies with our goal of generating the highest possible return at an acceptable risk,” a spokesperson for the fund told Net Zero Investor.

In the past two years, the fund has conducted deep-dive studies on both small modular reactors (SMRs) and fusion power to identify investment opportunities and to understand their potential role and impact on the future energy system.

“With a few exceptions, there are limited investment opportunities in terms of listed SMRs or fusion companies as of now, but we are actively monitoring and engaging with companies that are considering a future initial public offering,” the spokesperson concluded.

The fund’s mandate was amended on 1 January 2020 to include investments in unlisted infrastructure for renewable energy of up to 2% of the value of the fund.

This mandate defines renewable energy infrastructure to cover production, transmission, distribution, and storage of energy based on renewable energy sources, and thus currently excludes nuclear power.

“Norway has started to think about nuclear, which would have been unheard of a few years ago”, said King.

“The question is how do you decarbonise a large-scale, industrial economy without nuclear?” he added. “Currently, we don't see a technology that is both green and able to support the scale and the demands of a large-scale, industrial economy.”

Institutional Involvement

Like other energy infrastructure assets, institutional capital tends to come in at the post-construction phase, once the project has been sufficiently “de-risked”, said Capgemini’s North America nuclear transformation director, Paul Shoemaker.

Only governments build and fund large nuclear power stations – a trend that has continued into the “nuclear renaissance”.

The Ontario Municipal Employees Retirement System (OMERS), for example, owns a 48.3% stake in the Bruce nuclear power plant in Ontario, Canada, but wasn’t responsible for its construction.

The Bruce power plant generates approximately 30% of Ontario’s electricity.

Another way into nuclear for institutional investors is via green bonds. In 2021, the Bruce power plant became the first nuclear company in the world to issue green bonds, a sign of the acceptance of nuclear, at least in Canada, as green.

The green bonds were used to finance the extension of some of its generating units and increase output of existing units.

In November, the French power company EDF launched Europe’s first nuclear green bond, based on the Bruce model. The $1 billion bond is being used to “refinance EU-Taxonomy aligned nuclear energy capital expenditures in existing French nuclear reactors in relation to their lifetime extension”.

Moreover, some sustainable energy transition funds may include nuclear in their portfolios. In 2021, Brookfield Asset Management raised $15 billion for the Brookfield Global Transition Fund.

Brookfield’s vice chair Mark Carney claimed the fund provides “significant scale of capital with catalytic long-term investment the world needs to help put our planet on a sustainable net-zero pathway”.

The Ontario Teachers’ Pension Plan is one of the fund’s leading investors and founding partners. Public Sector Pension Investments and the Investment Management Corporation of Ontario also committed an undisclosed amount.

In addition to investments in renewables, sustainable agriculture, recycling and carbon capture technologies, the fund bought a massive 51% stake in Westinghouse, a US nuclear engineering company active in the nuclear supply chain.

“That stake was framed as kind of a bet on the nuclear renaissance and the role nuclear will play in the transition to net zero,” said Patrick DeRochie, senior manager at Shift Action for Pension Wealth and Planet Health.

Unlike say Norway or Australia, Canada has always been nuclear friendly, with certain provinces using it more than others.

For example, nuclear generates around 50-60% of the Ontario’s power supply, while the national average is 16%. Canadian provincial governments are also investing a lot of public money in nuclear.

SMRs may prove to be an exception to the “government builds, private companies operate” rule, according to Shoemaker

Due to the smaller scales and different price points of this emerging technology, more independent companies could take a role in building and operating them.

In the US, private funding for SMRs mostly comes from the “billionaire club”, such as Bill Gates and Sam Altman, who have plenty of venture capital to spare.

One caveat is that a high-inflation, high-interest rate macroeconomic environment tends to favour traditional large-scale nuclear constructions over SMRs, according to Shoemaker.

Scepticism

The two main arguments against nuclear power is that it carries significant environmental risk, especially in waste disposal, and uranium – an essential ingredient for nuclear energy – isn’t renewable.

Regarding the green bonds used to extend the life of the Bruce power plant, DeRochie noted serious safety concerns, given the plant’s location on the shores of the Great Lakes, which is the world’s largest fresh water supply.

He also worried that the preference for nuclear is taking the focus away from renewables, which tend to be underfunded in Canada.

“We haven’t seen the kind of growth in renewables in Ontario as we have seen in other jurisdictions,” he said.

Solar, wind, and tidal account for only 6% of Canada's energy sources, though hydro is a long-standing energy source and makes up 60%.

Another problem is waste. For example, in Canada, the Nuclear industry is trying to convince local communities to host long-term waste storage facilities, but has met with stiff opposition, especially from indigenous communities.

Radioactive waste is hazardous because it contains or emits radioactive particles, which if not properly managed can be a risk to human health and the environment. Those highly toxic by-products can remain radioactive for tens of thousands of years.

Two of the world’s biggest nuclear accidents – the Fukushima nuclear disaster (2011) and the Chernobyl disaster (1986) – released a significant amount of radioactive isotopes into the atmosphere, with negative consequences for people and the environment.

Since the 1950s, when early commercial nuclear power stations started operating, more than 250,000 tonnes of highly toxic nuclear waste have been accumulated and spread across 14 countries worldwide.

After years of negotiations and political roadblocks, Finland spent approximately €2.6 billion building an underground nuclear waste storage facility.

While Finland’s solution might be the world’s first long-term storage facility, doubts remain whether it will truly last 100,000 years – the minimum required storage time.

As for the role of nuclear in the net-zero transition, the development timeline poses challenges, as nuclear projects tend to be costly, lengthy, and riddled with safety concerns and regulatory issues.

“Because of the time it takes to build these projects, you don’t have electricity coming online for another 10 to 15 years,” DeRochie said. “From a climate change perspective, that’s deeply problematic, because the science tells us we need clean electricity and emissions reductions right now, without delay.”

Shoemaker, who comes from the nuclear industry, disagreed with this “frequently voiced timeline concern”. “Just because the next generation of nuclear power may not be ready before 2050 doesn’t mean we should discount it,” he said.

“When it comes to something as complicated as the energy transition, we need to look at all the solutions, not pit one technology against another.”