Road to 2030: investor confidence and short-term renewables targets

Renewable energy’s financial viability depends on its political one. For investors, 2030 renewable energy targets - politically crafted and commercially executed - matter more than ever

It’s that time of the year again. Climate policy and those who shape it are in the spotlight. On 2nd December, at COP 28, 116 countries signed a pledge to triple renewable energy by 2030.

For renewable energy investments, these pledges matter. The answer to the question; “what portion of power generation will come from renewables by 2030?” – is simultaneously commercial and political.

For allocations into renewables to pick-up, pledges must be credible. Any hint of policy uncertainty is determinantal to revenue expectations for a wide range of renewable energy players from wind turbine manufacturers to solar farm operators.

As the case of UK Prime Minister Rishi Sunak’s green U-turn proved, markets could get jittery when politicians don’t stick with the plan or alter it in ways that suggest a wavering will.

Before investors pour their capital into a renewable energy asset, they must first convince themselves that they believe in its political story. 2030 targets offer a litmus test of investor confidence.

End of the decade

In January this year, Norges Bank– a Norwegian asset owner – paid €600 million to acquire a 49% stake in a portfolio of assets that include solar farms and onshore wind farms in Spain. According to Norges Bank, the portfolio could serve the annual electricity needs of 700,000 Spanish households.

Interestingly, some of these assets are not online yet. Nine projects will only be completed by 2025. Which means the expected design of the Spanish grid in 2025 is of vital importance to Norges Bank’s investment hypothesis.

On paper, the politics play into the logic. Spain is bound by targets set in Brussels under the aegis of the European Union. The country also has its own strategy that envisions a 74% share of renewables in electricity generation - by 2030.

Short-term targets like Spain’s matter relatively more to investment decisions than long-term visions. Most developed countries have set a target of net zero by 2050 or sooner. It is hardly exciting anymore to see a head of state make promises with a 2050 timestamp.

2050 is so far away that these targets are almost always politically affordable. Assuming an average political cycle of about five years, 2050 is a long way off.

2030 targets on the other hand are too close to take lightly. The end of the decade is close enough for households, firms, investors and voters to base their decisions on what it might look like.

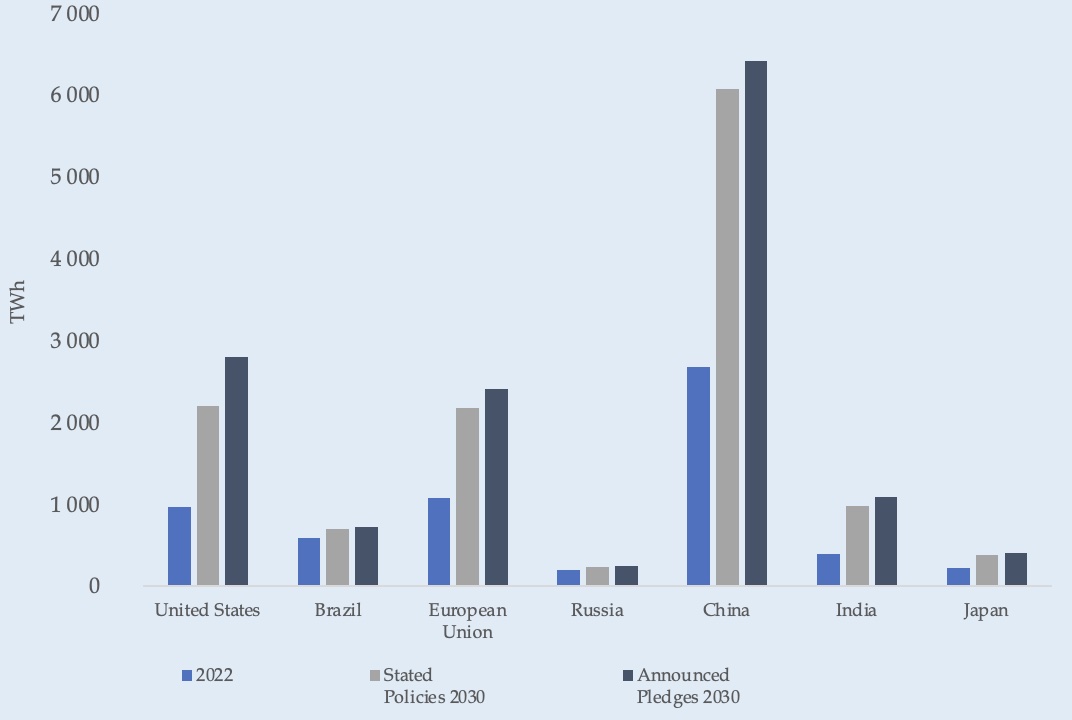

2030 vision

Nowhere is this more visible than in renewable energy industries.

The data in the graph above shows how different countries compare on their 2030 renewables targets. Some are more ambitious than others but not all ambitions are backed up by policy – which is why there is a gap between “announced pledges” and “stated policies”.

According to the International Energy Agency, stated policy scenarios are “designed to provide a sense of the prevailing direction of energy system progression, based on a detailed review of the current policy landscape”.

In the US, for instance, considering stated policy scenarios instead of announced pledges, reduces 2030 renewables capacity by more than 602 TWh – roughly 60% of America’s current renewables capacity.

It is likely that the Inflation Reduction Act (IRA) changes the outlook significantly. However, the politics of the IRA are far from settled. The IRA is fundamentally Democrat in its identity and the next Presidential election will determine how much of it survives.

The invisible hand of policy

Politically crafted 2030 renewables targets have tangible, commercial ramifications. At times these are explicit, but it is more likely that they play a more subtle Adam Smithian role in private market decisions.

Australia offers an example of the invisible policy hand. Tilt Renewables, an Australian renewable energy developer began work on a wind farm in the state of New South Wales back in 2021. In 2022, the Albanese government announced an aggressive renewable energy expansion plan – 80% by 2030. The Australian House of Representatives even passed a bill to cement the target into law.

The bill was important. “We will move quickly to enshrine Australia’s 2030 and 2050 targets in legislation, providing the certainty industry and investors have been seeking”, said Prime Minister Albanese.

In theory, Albanese’s certainty should increase demand for electricity produced by Tilt Renewable’s wind farm. There is some truth to that. In June 2023, AGL Energy – one of Australia’s largest energy distribution companies signed a 15-year power purchase agreement with the Rye Park wind farm.

By the time the PPA lapses, Canberra will change its leadership thrice.

The end of the decade is not far away. The credibility of 2030 renewable energy targets will be a test of political will and commercial character. Countries such as the US, China and the EU have set ambitious targets for how green their grids will be in seven years.

Ambition, alas, is a necessary but not sufficient ingredient of investor confidence. Investors and politicians differ in the time frames they think in. Policy certainty then, is more complex than it looks.