How are the UK’s master trusts tackling the net zero challenge?

The UK's rapidly growing master trust market could become a key player in the transition towards a net zero economy

The UK’s master trust market is at a crucial turning point. Having been launched just over a decade ago, when the UK government announced the automatic enrolment of millions of UK workers into collective workplace pension scheme, their assets have grown exponentially, and they are now on the lookout for exposure to more complex investment strategies.

For the past ten years, cost was the decisive factor the bulk of defined contribution providers and they almost inclusively invested in listed markets, predominantly through index-based strategies. But this could be about to change as DC assets gain critical mass and policy makers are pushing for more DC investment in illiquid assets.

At the time of writing, master trusts still account for a minority of the £1.2trn in defined contribution assets in the UK, managing just over £105.3bn in assets, according to the UK’s pension regulator TPR.

While the number of master trusts on the market has shrunk to 34, they manage the retirement savings of approximately 23.7mn UK employees. This means that by 2029, their assets are expected to increase to £461bn and will then account for almost half of the UK’s defined contribution market.

RENEWABLE INFRASTRUCTURE SUMMIT

12/03/24, London Stock Exchange | Asset owner knowledge sharing & due diligence

Given this growth trajectory, and with the majority of defined benefit schemes now closed, UK master trusts are on track to become a dominant force in the UK institutional market within the next decades.

Consequently, their ability to decarbonise their portfolios will be an important factor, if the UK is to reach its net zero targets. But where do master trusts stand on tackling climate?

Net zero targets - significant differences

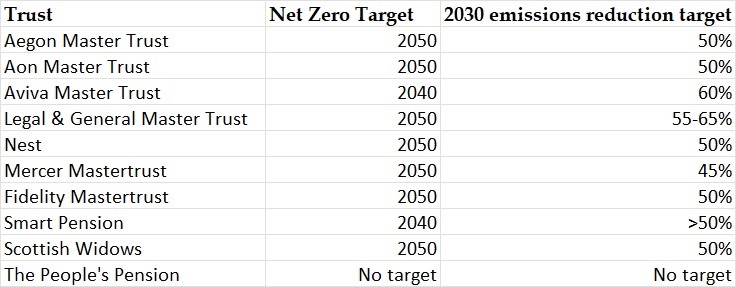

Net Zero Investor took a closer look at the climate ambitions for the 10 largest master trusts operating in the UK market, based on the information provided in their TCFD reports. Almost all now have a net zero 2050 target, Smart Pension and Aviva go even further, they aim to offer net zero investment portfolios by 2040.

Meanwhile, The People’s Partnership, provider of the People's Pension is the only master trust in our list which does not yet have a net zero target, but a spokesperson for the master trust told Net Zero Investor that its climate change policy is “aligned with the scientific consensus of keeping warming below 1.5°C compared to pre-industrial levels.”

In its TCFD report, the People’s Partnership stresses that the master trust has a net zero ambition but that the exact implementation was still under review, given the complexity and uncertainty around carbon data at a portfolio level.

While most master trusts now have a clear phaseout target, there are significant differences in their approach to short-term targets – specifically the 2030 target.

On average, trusts say they will reduce 50% of their portfolio emissions by 2030, on a 2019 baseline. However, some funds are more aggressive (60% is what Aviva says it will achieve) while some are less aggressive (Mercer says it targets 45%). Some even have a 2025 plan – Nest master trust is aiming to achieve a 30% emissions reduction by 2025, Smart Pension says it will cut portfolio emissions by 50% by 2025 in the default growth fund.

Positive and negative screening in default portfolios

Some master trusts such as Nest offer their members a choice to invest for example in an ethical fund, but with more than 90% of DC members enrolled in default funds, they tend to be decisive for net zero ambitions.

Given the younger age profile of the average UK DC membership, DC master trusts tend to be more heavily invested in equities. For members that are 20 years away from retirement, the average DC default fund tends to invest 70 of its assets in listed equities, according to the Investment Association. At the time of writing, only very few DC master trusts, Nest in particular, have ventured into private markets.

This means that their decarbonisation efforts are at this point predominantly focused on screening and tilting of their portfolios in listed markets.

Screening can be either positive or negative. Positive screening means companies that satisfy a certain range of criteria are included. For example: Aegon offers a short-term commercial debt portfolio “uses proprietary climate transition research to identify companies that have robust, credible plans to transition towards a low carbon economy”.

In contrast, negative screening works based on exclusion. A case in point is the Mercer master trust which decided last year to divest from companies than derive > 10% of revenues from thermal coal production.

“Although we prefer integration and engagement, we want to avoid profiting from activities that do not align with our members’ values and so we exclude these from our investments”, the company says on its website.

Thematic tilting

While screening can determine to pool of investible assets, tilting determines the distribution of capital across this pool. This means a portfolio is weighted, a given percentage of funds are subjected to the theme or asset class. In effect, this should result in a tilt of the portfolio towards a given investment theme.

For example: Nest applies a climate tilt across its developed and emerging market equity portfolios which reduces exposure to the companies it considers to be the most exposed to climate risks.

Aegon also offers a Climate Focus Equity portfolio which invests a minimum of 80% of its capital in “companies across the globe with exposure to the theme of climate change solutions”.

Themes that guide the tilt vary based on the trust and sometimes the fund. Common themes include solutions, green technology, and renewable infrastructure. Some less common themes are deforestation (Legal and General) and just transition (Aon).

A flipside is that the tilt can result in a sectoral focus of these portfolios. Common sectors covered include industrials, materials, technology, and infrastructure.

Because DC master trusts tend to be predominantly listed in developed market indices, tilting more heavily towards sectors with a lower carbon footprint can leave them more heavily exposed to the US tech sector which could become a concentration risk.

Drivers of change

While these steps to tackle climate change have so far been modest, there indications that defined contribution funds could become important drivers of change in the energy transition.

One driver of change are DC members, who are expressing a desire that their pensions are invested for a greater good. A recent survey by Legal & General Investment Management (LGIM) among more than 4000 DC members saw a clear majority expressing support for greater investing in private markets if those investments delivered better ESG outcomes. Investments in renewable energy were listed as a top priority for scheme members.

Rita Butler-Jones, head of Defined Contribution (DC), at LGIM comments: “Despite the financial pressures and systemic challenges we are currently seeing around the world, it’s clear that ESG remains central to many members’ attitudes about how they want their pension to be invested.

However, the survey also showed that less than a quarter (22%) of DC members are willing to pay more for investments in illiquid assets irrespective of performance. "The onus is on us to demonstrate where we believe illiquid assets can play a meaningful role in aiming to deliver better overall member outcomes – and in the process, unlock the potential power of DC capital to invest in the UK and beyond" Butler-Jones adds.

Increased public appetite for investments in renewables coincides with the UK government’s push for greater pension fund investment in private markets.

In July last year, the British chancellor gathered executives for nine of the country’s largest master trusts to sign the so called “Mansion House Compact” a pledge to invest at least 5% of their default portfolios to private markets.

However, the pledge does not specify that these assets should invested in renewables and government’s promises of higher investment returns have been questioned by industry practitioners.

Regardless of their allocations to private markets, DC master trusts could become an important force on stewardship and engagement in listed markets. With most of their investment activities outsourced, their ability to intervene has so far been limited.

However, master trusts are increasingly demanding that managers step up their game on tackling climate change. For example, the Fidelity master trust says: “We monitor fund managers’ engagement and voting activities in line with our sustainable investing policy and will be seeking to assess the extent to which engagement on climate-related topics has been undertaken by the fund managers used in our default strategies”.

Similarly, Nest and the People’s Partnership have played an active role in the UK Asset Owner Roundtable to discuss potential misalignment between asset owners and managers. Meanwhile Scottish Widows has been instrumental in introducing split voting at BlackRock.

Despite being still relatively small in size, many DC master trusts are already punching above their weight when it comes to stewardship on climate change. And with their assets on track to grow, they are likely to become a force to be reckoned with.