Mixed responses across industry as ISSB takes charge of TCFD reporting

Industry insiders respond with a mixture of praise and disbelief as the ISSB has agreed to take over the responsibilities of the TCFD next year

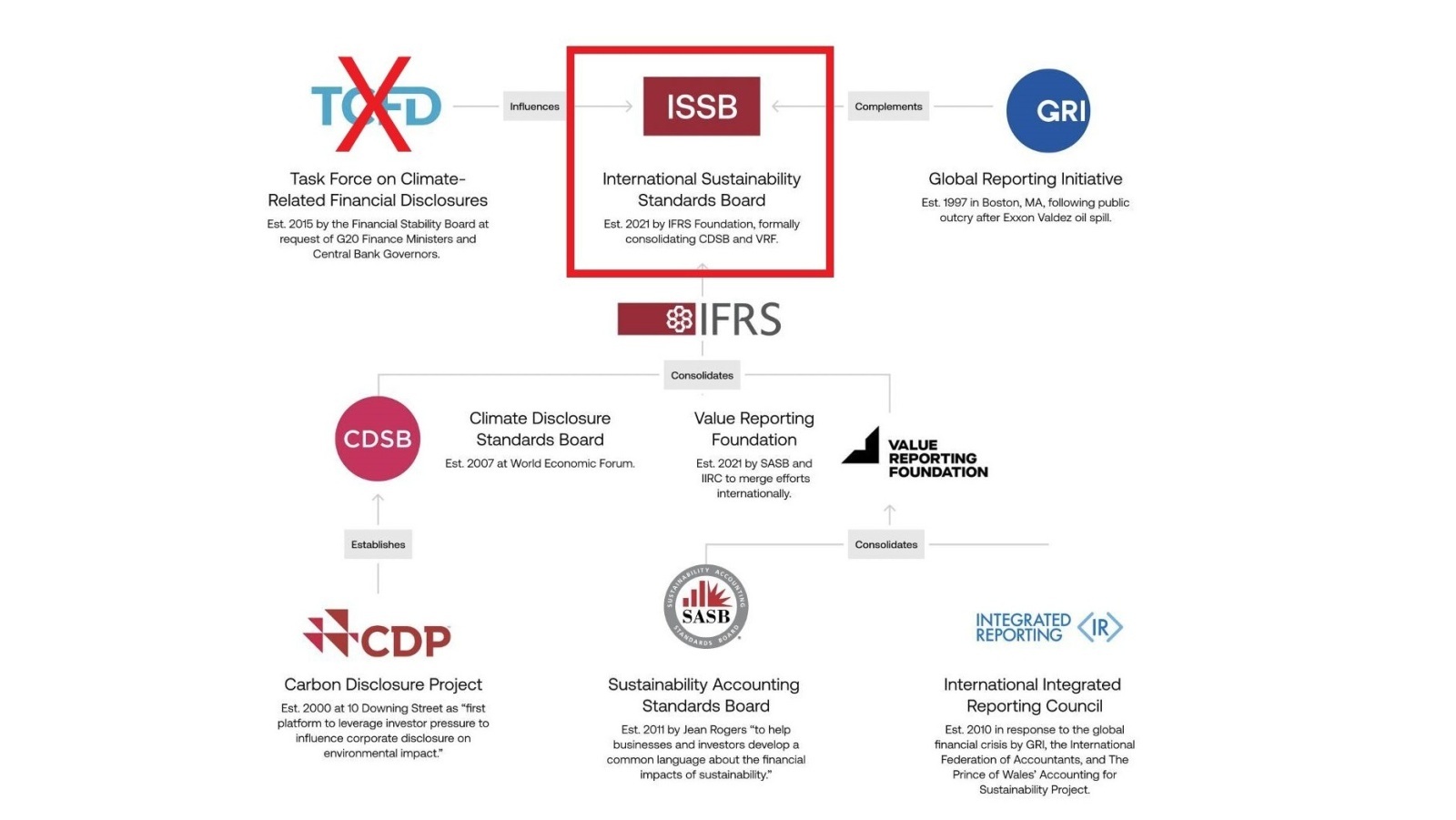

The International Sustainability Standards Board (ISSB) confirmed yesterday it will take over the responsibilities of the Task Force on Climate-related Financial Disclosures (TCFD) in 2024.

The move, which follows a formal response by the Financial Stability Board (FSB), marks a major change in the sustainability reporting landscape as it means a major consolidation of frameworks.

The announcement comes only weeks after the ISSB rolled out new global standards for sustainability and climate reporting.

Responding to the announcement, many insiders across the investment community question today what the change means for businesses and their investors.

Speaking to Net Zero Investor, Catherine Chisem of climate consultancy EcoAct, said: “The ambition of merging the TCFD and ISSB is something that should be lauded. The current landscape of reporting for companies and institutional investors is complex and fragmented and any step towards harmonising these frameworks is necessary and sorely needed.

“Investors can expect to feel the real impact of this in how regulators and governments interpret and mandate climate-risk reporting. While short-term impacts may be limited, in the longer term it represents a first step towards frameworks for reporting on climate risk gradually converging."

Andrew Griffiths, director of policy & partnerships at PlanetMark and chair of the Institute of Directors' National Sustainability Taskforce, took to LinkedIn to share his views.

"This is huge news because it massively simplifies the landscape for sustainability reporting and disclosures at a global level, with only Global Reporting Initiative (GRI) being left alongside IFRS," Griffiths wrote.

"This news really cements the IFRS Standards S1, sustainability disclosure, and S2, climate disclosure, which fully incorporated TCFD requirements, as the framework of choice for companies making climate-related disclosures globally," he added.

Griffiths said he "wouldn't be surprised if we saw this final standalone body merge into IFRS in the next 12 months."

"Personally I find this quite worrying. The ISSB has been moving at a snail's pace and the IFRS Foundation is still trying to figure out how to do business between the IASB and ISSB."

Meanwhile, Tim Dee, a sustainability reporting and technical accounting expert and regional lead for the UK and Europe at the Association of Chartered Certified Accountants, called the development "worrying".

"Personally I find this quite worrying. The ISSB has been moving at a snail's pace and the IFRS Foundation is still trying to figure out how to do business between the IASB and ISSB," Dee said.

He added: "The bodies it merged with last year, SASB and the Value Reporting Foundation, including the Integrated Reporting. EFRAG meanwhile has accomplished approximately six times as much as the ISSB in the last year, with significantly less funding."

However, Sarah Whale, a financial business consultant at London-based advisory firm adam&eve, welcomed the announcement.

"Simplification is a great start," she said, adding that "I made a conscious decision to not train myself in all the different frameworks. I am glad I didn't devote time and money to that. GRI will inevitably merge I think."

"The feedback I am reading is that ISSB doesn't go far enough but I believe that will come," Whale shared.

"This is huge news because it massively simplifies the landscape for sustainability reporting and disclosures at a global level."

Meanwhile, Sarah Carré, the founder and CEO of People and Planet and head of membership committee at the Jersey Association of Sustainability Practitioners (JASP), wrote on LinkedIn that "I cannot express how disturbing I find this ESG land."

She wrote that "divorced from sustainability that the world needs, ISSB's definition of sustainability is false, still focused on single materiality, no consideration of social or ecological thresholds, planetary boundaries."

Carré urged the bodies to "use these frameworks to manage risks to enterprise value creation" but said "don't call them 'sustainability' standards giving the impression that reporting will create impact."

She expects the change "will expand licences to tick boxes, including the consultancy giants who are going to make a fortune on implementation support when they should be calling this out."

Also read

Setting standards: How the ISSB plans to revolutionise climate reporting

Ralph Thurm, a Netherlands-based sustainability reporting consultant, and the founder and managing director of A|HEAD|ahead, also rejects the changes.

"A massive new conflict of interest. Does nobody see this?"

Thurm argued that "TCFD's modalities, that had some safeguards against corporate capture due to FSB's status and government membership, is replaced with a system in which corporations will monitor themselves, as the IFRS is run by, for, and with corporates."

"How could this be a positive story?"