The rise of cat bonds: how insurers shield themselves from climate risks

The global catastrophe bond market has swelled to a record $40 billion. So how do they work, and why are investors embracing these securities en masse?

Catastrophe bonds, or cat bonds, as they are generally known, are rapidly gaining momentum among investors around the world.

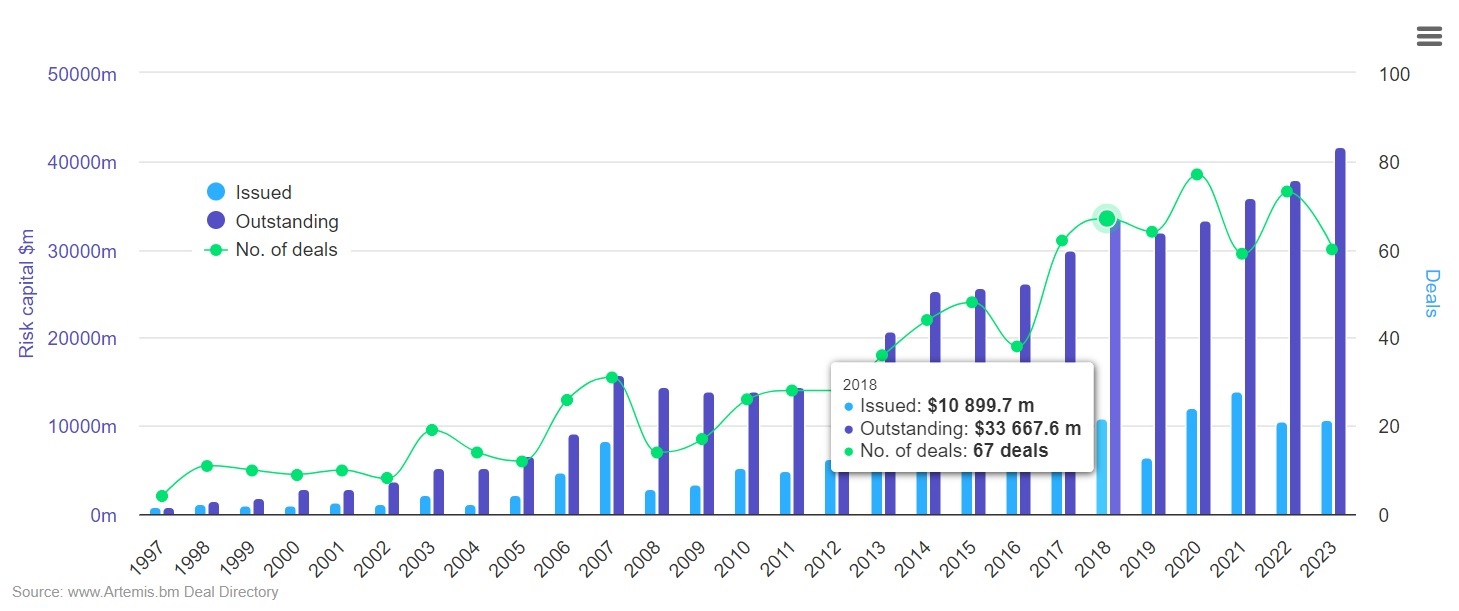

In fact, the global cat bond market has swelled to a record $40 billion. And even though that may still be a fairly small share of the overall bond space - estimated to be worth around $140 trillion - the new record does mean a doubling of the cat bond market in just ten years time, as reported by Net Zero Investor yesterday.

At present, the catastrophe bond market is growing at a compound annual rate of around 10%, according to a market analysis by Artemis.

And it seems investor appetite does not stop there.

The World Economic Forum expects the space to grow by another $10 billion in the next two years alone, to $50 billion at the end of 2025.

The main driver behind this growth? The horrific images we regularly see on our television screens, from floodings in Pakistan and China to fires in California and Australia.

As the number of natural disasters increase, and events intensify, more and more insurers use the securities to shield themselves against losses from consequences of climate change such as natural disasters.

Wildfires, hail storms and unprecedented heatwaves in Europe and the U.S. this summer have pushed insured losses from natural disasters, thereby helping cat bonds' total value to hit the $40 billion mark.

Morningstar summarised the success of the cat bond in a recent report: "The appeal of this market is its lower correlation to traditional bond and stock markets due to the unpredictable nature of weather-related disasters, and potential for higher returns."

The concept is as such: "if a disaster doesn’t occur, the investor will receive their money back plus interest," explained Mara Dobrescu, director of fixed income research at Morningstar.

Also, if a catastrophe does take place, the investor can lose some or all of its money, depending on the cost to the reinsurer.

Aon Securities highlighted cat bonds in a recent report, calling the space’s growth “an impressive feat”.

“Whilst the cat bond market has observed rate hardening, it continues to diversify and attract both new and repeat sponsors, with relatively larger increases in traditional (re)insurance pricing placing the ILS market in a more competitive position year on year,” the firm noted.

Transfer risk

With extreme weather events like these on the rise, in what is arguably a direct consequence of climate change, insurance companies are looking for new ways to protect themselves from the growing financial risk.

But they are not new: cat bonds were first issued in the 1990s at a time when the insurance sector was licking its wounds from a range of costly disasters, such as Hurricane Andrew, which had devastated large parts of Florida and the Gulf coast and driven some insurers out of business.

Since then, the cat bond market has experienced tremendous growth and pulled in large amounts of fresh funding with first-time investors entering the space.

The World Economic Forum singled out American insurer USAA in a recent report as a good example: the firm raised $300 million in November 2021 to cover risks including US tropical cyclones, earthquakes and severe thunderstorms.

What is important to note is that it is not merely insurance firms that use cat bonds.

The World Bank priced a bond in July 2021 that gives the government of Jamaica protection of as much as $185 million against losses from multiple storms during three Atlantic tropical cyclone seasons.

Also in October 2021, the Los Angeles Department of Water and Power raised $30 million to shield the city from wildfire losses in California.

So how do cat bonds work in practice? Basically, they allow insurance firms to transfer the risk of natural disasters covered by their policies to investors, unsurprisingly this comes with a price.

The money raised with these bonds is set aside to cover potential losses. If events are detailed in any agreement - insured losses from a tropical storm reaching a specific level, for example - the insurer gets to use the money to offset what it has paid out to policyholders.

In that case, it no longer has to repay the holders of the bond, who are then likely to see their investment evaporate.

However, if the natural disaster that is covered by the bond does not actually take place, which is often the case, the investors get their money back in full when the bond matures, usually in three to five years.

And, along the way, they collect regular interest payments.

Complex market

Due to the complexity and uncertainty of this market, catastrophe bond strategies are typically more suitable for sophisticated investors with long investment horizons and no immediate liquidity needs.

The fund universe is "lumpy" - as Artemis researchers put it: funds managed by GAM, Schroders and Twelve Capital take up the lion’s share of assets, which could raise potential capacity concerns.

On average, funds in the catastrophe bond cohort delivered on their promise of outperforming the broader global bond market and delivering low correlation to most traditional asset classes.

"Reinsurance companies try to assign reasonable probabilities to the occurrence of a specific event, but they lack any consistent predictability."

“This higher risk and potential for individual bonds to experience significant losses means diversification is key when investing in a catastrophe bond strategy," Dobrescu pointed out.

"The challenge for this asset class is that despite the years of data on such naturally occurring events, reinsurance companies try to assign reasonable probabilities to the occurrence of a specific event, but they lack any consistent predictability, particularly as climate change introduces additional uncertainties,” she added.

Another challenge is that fund managers charge relatively high fees to investors on most share classes, while there are no passive options currently in the catastrophe bond space.

Reinsurance

Finally, let's zoom in on the main method that insurance companies use to offload risk, reinsurance, when they acquire policies from other insurers that limit their losses in case of a disaster. This is generally seen as a responsible method to make sure companies do not take on too much risk at once.

But reinsurers, just like any insurance firm, do not always pay out after every claim. And the policies they sell typically last merely a year or two, max.

Catastrophe bonds, on the other hand, are set up to remove ambiguities by setting out clear triggers for payment and allowing insurers to lock in the price of protection for a longer period of time.

The main appeal for investors is that these bonds pay higher interest rates than most other varieties, so they can potentially generate more income.

Another advantage is that, because catastrophe bonds are linked to specific disasters, they offer returns that are mostly unaffected by economic cycles or any volatility in the financial markets.

This makes cat bonds a source of income when other investments go downhill.

Also read

The silence score: how active are the world’s biggest investors on climate stewardship?