Timing peak oil: are we heading for a delayed or timely transition?

Analysts are deeply divided when global demand for oil is likely to peak. NZI examines why asset owners are still struggling to manage the uncertainty around the transition timeline

The effects of climate change are notoriously difficult to predict. While non-linear tipping points – such as the possible collapse of ocean systems – affect people and planet in complex ways, views differ even on the economic impact of the ostensibly more straightforward temperature increases. Analyses, even from respectable, well-meaning sources, tend to come with serious caveats: If the world heats to 2 degrees, the impact would be this BUT (and but is probably the most important word in the sentence), the model doesn’t capture tipping points or potential knock-on effects, like mass migration, war, and social instability. In other words, it is at best a rough estimate and probably not even close to the truth.

Physical impact asides, the transition timeline is also riddled with uncertainty. It is still unclear how and when policymakers will enact measures to combat climate change in line with the Paris Agreement. Although most governments have now set net-zero targets, implementing them requires extensive and ambitious policymaking, such as robust carbon pricing, and banning certain pollution-heavy economic activities. Industry pushback in the form of concerted lobbying activities is never far from the legislature.

There is also the fear of right-wing groups weaponizing climate policy for their own ends, presenting climate action as the quixotic crusade of a top-down elite who are happy to squeeze the purses of ordinary citizens in their pursuit of a carbon-free chimera. Presidential hopeful Donald Trump’s election slogan “Drill Baby Drill” epitomises such fears, while the recent farmers protests in Brussels show that many EU citizens do indeed feel strongly that environmental protection does indeed come at their expense and they ought to rail against it.

The sticky question of oil demand peaking

From an asset owner’s perspective, knowing how and when the transition will happen is essential for appropriately managing climate-policy-related risks and opportunities. The peak in global oil demand is arguably one of the most critical dates on the transition timeline. A drop in demand brought about by the advent of carbon-free technologies has severe negative implications for oil and gas companies and marks the beginning of the end of the fossil fuel era. Determining when it will happen may impact a fund’s approach to net zero, especially those asset owners that continue to hold equity or fixed income assets in oil and gas companies.

Asset owners take wildly different views on this simple yet critical date on the transition timeline. Those that align with the controversial Organization of the Petroleum Exporting Countries (OPEC) position that oil demand doesn’t peak until the 2040s, making for a seriously delayed transition, are likely to want to hold onto oil and gas assets for longer and even invest in expansion to meet rising demand.

Those that support the International Energy Agency (IEA) forecast that reaching net-zero by 2050 means oil demand peaks this decade are likely to think very differently about their net-zero investment strategy, especially how they support oil and gas. Thinktanks such as Carbon Tracker highlight the financial risk of taking the wrong view. If the transition happens faster than investors are planning for, investors could be straddled with stranded assets and equity in de-rated oil and gas companies as these once immensely profitable enterprises morph into unwieldy dinosaurs.

"It’s all about the detail, and detail is often what we lack.”

Yet even the seemingly simple task of putting a date on oil demand peaking is beyond asset owners and perhaps even the most seasoned policy analyst.

“We haven’t set a specific date for oil demand peaking,” said Fredric Nyström, head of sustainability and governance at AP3.

This is because AP3 “doesn’t have the expertise” to make this kind of detailed and complex analysis. Instead, AP3 aims to avoid the risk of stranded assets and de-rated oil companies by limiting its exposure to oil and gas. It is also “very selective” about the limited oil and gas investment it does make. This approach is built around an awareness of the financial risks of oil companies as well as an ethical responsibility to combat climate change.

“Whether oil demand peaks in 2030 or 2040 will have a limited impact on our portfolio,” Nyström added.

While AP3 doesn’t feel able to set a date for oil demand peaking, it does run “scenario analyses” that look to quantify the impact of certain transition scenarios on its portfolio. Nyström is sceptical of the merits of such exercises, given the “significant data issues and the uncertainties that are inherent to climate risk”.

“It can be very difficult to find company specific data to make the results from these scenario analyses truly meaningful,” he said. “Both the physical risk of climate change and the associated transition risk affect different companies differently, even those in the same sector. The more widely available sector-level information can be useful as a starting point but not so helpful in the long run. It’s all about the detail, and detail is often what we lack.”

Net Zero Investor's Nature Positive Investment Forum

24 April, London Stock Exchange sign up here

Like AP3, Universities Superannuation Scheme (USS), one the UK’s largest pension schemes, doesn’t set a date for oil demand peaking, believing such a date is still impossible to determine even with the best available information. However, it is highly conscious of the importance of attempting to chart the transition timeline.

In the wake of critical reports last year that suggested pension funds and their asset managers systematically underestimate climate risk, USS decided to work on four separate narrative scenarios, each with a distinct transition dynamics that takes a different view not just on oil demand but related topics like EV adoption. Developed in collaboration with the University of Exeter, those scenarios range from optimistic, with drivers working in harmony and rapid decarbonisation, to pessimistic, where a toxic political climate compounded by dysfunctional markets frustrates progress. The aim is to present a “richer, broader, and more realistic range of possible scenarios” that the fund can use to inform its investment decisions.

USS’s scenario analyses

Scenario 1. Roaring 20s – policy and markets align

Scenario 2. Green Phoenix – market-driven, while policy lags

Scenario 3. Boom and Bust – policy steps up after fossil fuel surge bursts

Scenario 4. Meltdown – policy failures compound weak growth

“The fact that some asset owners are preparing for a delayed transition, and some for a timely transition, reflects the significant uncertainty around not just government policy but also technological development,” said Robert Campbell, senior financial analyst at USS. “Our decision to work with four different scenarios is an attempt to navigate through this uncertainty.”

The transition timeline is a complex subject with many moving parts. In addition to the big question of when oil demand will peak, other questions include: Which industries will receive support for the transition and in what form? What are your assumptions for the cost curves of emerging technologies? What are your assumptions around the extent to which hard-to-abate sectors, like aviation, chemicals, and cement, will find ways to reduce their emissions? Who are the climate leaders and laggards in each sector?

“We’re not going to trick ourselves into thinking we can make a single point forecast when there is so much uncertainty,” Campbell added. “We want our analysts exploring risks and opportunities creatively, flexibly, rather than having tunnel vision about a particular scenario mandated by us.”

Maybe in the future, USS will have the confidence to hone in on a single scenario, but for the time being, the fund believes the “open-minded” approach is more appropriate.

Further down the rabbit hole

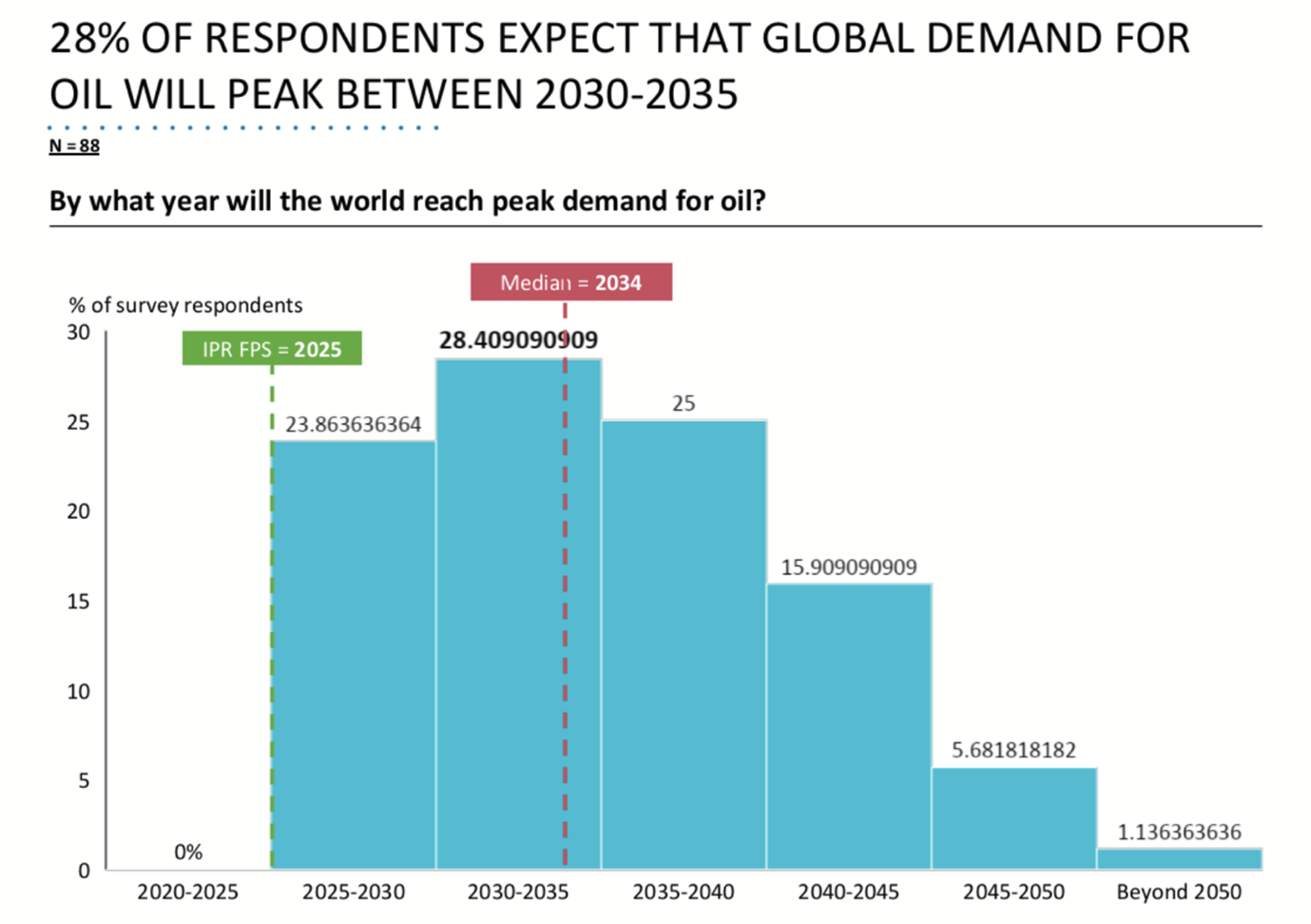

The sticky question of when oil demand will peak is just one particularly bright spot in a constellation of transition-timeline-related uncertainty. The UN-affiliated thinktank Inevitable Policy Response (IPR) shared with Net Zero Investor the previously unpublished results of a survey conducted last year with financial services professionals. The divergent responses to the relatively simple question once again shows how much uncertainty lingers over the transition timeline.

Inevitable Policy Response (IPR) itself forecasts that oil demand will peak in 2025, plateau for a period of five years, then start to drop off in 2030. It claims that its forecast is based on a thorough and up-to-date analysis of current policy trends worldwide.

If the IPR forecast turns out to be correct, the implications of this survey present serious financial stability concerns, since the median respondents don’t expect oil demand to peak until 2034, and almost half until after 2035. But if oil prices begin to drop in 2030 due to weakening demand, asset owners that still hold oil and gas assets may find themselves incurring financial losses, as stranded assets and unprofitable oil businesses signal the end of the fossil fuel era. This is especially true for oil and gas companies that have high extraction and production costs and depend on oil prices remaining high to stay profitable.

“Part of the problem is that there is so much difference – around 17 years – between the OPEC and the IEA scenarios,” said Jakob Thoma, research director at IPR. “This creates a confusing environment for investment professionals to work in. The truth is probably somewhere in the middle, which is where our forecast ends up.”

Pension funds, which often lack in-house expertise to pick a position on these complex topics, often turn to their investment consultants for guidance. Mercer, for example, advises institutional asset owners including a number of Local Government Pension Schemes in the UK. In the context of net zero, it sees its main role as helping pension funds set and implement net zero targets, though doesn’t take a position itself on when oil demand will peak.

“Sometimes our pension fund clients come to us because they’re thinking of setting a very ambitious net zero target,” said Vanessa Hodge, partner and UK sustainability integration lead at Mercer. “However, just as there are risks in transitioning too late, so too are there investment risks in moving to a net zero portfolio too early.”

The risks of "getting to net zero too early" consist of “massively constraining your opportunity set” and “introducing concentration risk”, as the fund narrows its scope from a market cap index of thousands of stocks to “just a few hundred.”

Again, the main message here is getting the transition timeline right is an impactful yet uncertain business that neither asset managers nor asset owners can pin down confidently.

Lobbying, lobbying, lobbying

Then, in the background, there is a relentless sea of noise, as the oil and gas industry makes concerted efforts to push back the transition as far as it can. On paper, most major oil and gas companies have commited to net zero by 2050; in practice, they continue to invest in expensive new expansion projects that only become economically viable in a delayed transition scenario; in public, they aim to take control of the transition narrative and spin it in a new direction, specifically one that allows for oil demand to grow well into the 2040s, in line with the OPEC’s forecast.

Saudi Aramco CEO Amin Nasser’s recent speech at CERAWeek, Houston, is a good example of the kind of narrative war that is currently being waged. Nasser cited the supply constraints caused by the Russia-Ukraine war and the recent energy crisis as proof that the “current transition strategy is visibly failing” and that moving away from hydrocarbons is prohibitively expensive and ultimately bad for developing countries and consumers. He supplemented his argument with targeted pieces of disinformation, such as EVs being unable to exist economically without subsidies (Fact check: BYD’s sub-$10,000 Seagull electric car sets a very low price bar). From a list of “hard realities” he concludes that the long-suffering global consumer is better off with fossil fuels, glossing this new oil-rich direction of travel for the transition with a mix of soft and triumphal words: “a multi-source, multi-speed, multi-dimensional road to reality”, that’s on the “right side of history, where everyone’s hopes and ambitions can actually be met”.

“The main challenge for the oil and gas industry is that they have to transition away from a high-profit to a low-profit business model, as the margins for renewables tend to be quite small,” said Nyström. “But, regardless of what oil majors say, the transition is happening and will continue to happen, even if the timeline itself remains uncertain.”

USS and University of Exeter call for 'radical shift' in measuring climate risk

Minsky moment: are pension assets at risk due to flawed climate analysis?