CA100+ pledges enter phase two: are companies on track to hit their 2030 targets?

Setting climate targets won’t impress investors anymore. Staying on course to deliver, will. Data suggests most companies might miss the mark

For investors with a net zero agenda, active ownership is tricky business. Investing in companies includes, inter alia, doing what many East Asian governments did in the 1980s: picking winners and engaging with them for the long-term.

Telling the good apples apart is arduous and complex – the differences in many cases can be marginal. To guide the allocation of their faith and cash, investors have hitherto relied on the act of disclosure and intensity of ambition.

Over the last five years, fossil fuel giants, miners or steelmakers who said they would reduce operational emissions faster than peers made for stronger portfolio candidates.

Now, the gears have shifted. Earlier this year Climate Action 100+, a global network of investors managing over $68 trillion in assets, announced a “Phase Two”. After five years of reasonable success in getting the big emitters to commit to an emissions reduction plan, a new era of active ownership lies ahead.

This new era focuses, more than ever before, on the implementation of corporate transition plans. The key question being – is a company on track to achieve what it said it would?

Findings from a tracker launched by CDP, a disclosure initiative, tells a worrisome story of where things stand.

The initiative [CA 100+] has a clear strategic focus on moving from corporate disclosure to the implementation of credible transition plans

Phase Two

2030 is both far too near and far into the future. From an emissions reduction perspective, 2030 is not far away. Similarly, for large pension funds, the demographic of their membership and the intergenerational nature of climate change, 2030 marks a critical juncture in their fiduciary duties.

Yet, for some boards who focus on three or five year project cycles it might seem distant enough to “wait and watch”. For politicians too, many of whom occupy their offices for five year terms, 2030 might seem too far to reach out for.

All this means that holding companies to account, on their stated emissions reduction plans over the next six and a half years is crucial to that elusive 1.5°C warming limit. The enforcement of which is more likely to be market-based. The CA 100+ “phase two” is a blueprint to that end.

“Building on the success and lessons learnt from the first five years, Climate Action 100+ now enters its next phase for the critical period up to 2030…. the initiative has a clear strategic focus on moving from corporate disclosure to the implementation of credible transition plans”, says Stephanie Maier, global head of sustainable and impact investment at GAM Investments, an asset management company and a CA100+ signatory.

The State of Play

A corporate climate action tracker published by CDP makes it possible to assess where things stand. The state of play, as far as target attainment is concerned, sets the stage for the challenge that investors will grapple with.

The tracker analyses data from around 10,000 companies including 91% of the FTSE 100 and 80% of the S&P 500 universe 2019 onwards.

A constraint in the methodology is an assumption of linearity. As CDP acknowledges, corporate emissions reduction can be non-linear: some companies front load their reduction which could slow down later while others particularly in hard-to-abate sectors might go for the reverse strategy: deeper cuts in emissions might take time to show up.

However, the current message, based on three years of disclosures, is one that requires urgent attention:

“The tracker shows only 24% of disclosing companies, covering 5% of emissions, are on track to meet their targets”, says Paul Dickinson, CDP’s founding chair.

CDP defines “on track” as a company that has either reached or is expected reach an emissions reduction level its own long-term target requires within a year’s delay.

The proportion of companies that are aligned with their plans has increased since 2019 but in absolute terms, it remains low. Looking at the data, about 43% of companies in the S&P 500 are either on track or are expected to be soon enough. This compares to 62% of FTSE 100 companies.

The tracker shows only 24% of disclosing companies, covering 5% of emissions, are on track to meet their targets

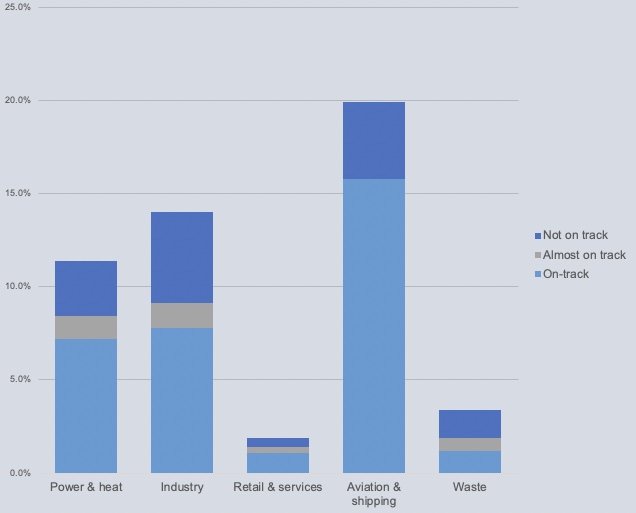

Crucially, one way of staying “on track” is to reduce ambition and aim for lower emissions cuts. The CDP dataset shows this trade-off at work, particularly from a sectoral perspective.

At first glance, the sector with most companies on track is aviation and shipping. The chart above shows that companies within this sector that are judged to be “on track” represent over 15% of the sector's emissions. In comparison, for the industrial sector, that number is under 8%. Over 500 companies in the industrials sector are not on track to achieve what they set out to do.

However, companies in shipping and aviation tend to have lower emissions reduction ambitions. It likely reflects the on-going innovation challenges such as with scaling sustainable aviation fuels. Consequently, the sector has the some of the lowest proportions of companies setting targets approved by the Science-Based Targets Initiative, according to the CDP indicator for target ambition.

Five years of active ownership has led to a plethora of ambitious corporate decarbonisation targets. The next seven years, will be about accountability. Come 2030, companies staying true to their word will become a necessary condition to achieve the even more ambitious 1.5°C goal.