Asia: the net-zero battleground

When it comes to achieving global progress on climate goals, investors should look to the East.

In his opening remarks at the inaugural Transition Finance Towards Net Zero conference in Singapore, the country’s top central banker, Ravi Menon, highlighted the relevance of Asia to the global net-zero agenda, “Asia”, said Menon, “this is where the battle against climate change will be won or lost”. The managing director of the Monetary Authority of Singapore (MAS), went on to back up his claim: “Asia accounts for half of the world's greenhouse gas emissions and is home to about 60% of the global population.”

Menon’s point is as logical as it is weighty. What makes the battle against climate change in Asia uniquely significant? Why is that question worth asking? Broadly speaking, two answers stand out: vulnerability and path dependence.

Region at risk

For one, the effects of climate change are felt intensely. In 2019, Indonesia took the decision to relocate its capital from Jakarta to a province on the island of Borneo. Among the many factors influencing that decision was the stark reality of a sinking Jakarta: by some estimates, a quarter of the city could be submerged by 2050. Was the Jakarta decision a canary in the coal mine?

Like Jakarta, the rest of Asia’s vulnerability to a warmer planet is ubiquitously considered a reason for concern. Its exposure to the severe consequences of more frequent, more intense adverse weather changes is alarming.

According to research from consulting firm McKinsey outcomes such as rising flood risk and temperatures are expected to lead to elevated levels of infrastructure risks and food security concerns. For example, the McKinsey report finds “about $1.2tn in capital stock in Asia is expected to be damaged by riverine flooding in a given year by 2050”.

Of all these factors, topography is perhaps Asia’s greatest vulnerability. According to the UN’s Economic and Social Commission for Asia and the Pacific (UNESCAP), Asia is the world’s most disaster-prone region and 2.4bn people live in low-lying coastal areas, regions particularly susceptible to rising sea levels. This translates into a disturbing reality: for every two-metre sea level rise, 180m Asians could be displaced, according to the UN Development Programme.

People, firms and assets in Asia are operating at a heightened sense of climate vulnerability.

Path dependence: the law of enduring influence

Secondly, solving the transition puzzle in Asia is a complex activity. Asia is a region where rapidly rising electricity demand is met by historically fossil-fuel intensive energy supply chains. Asian energy security is heavily reliant on these supply chains.

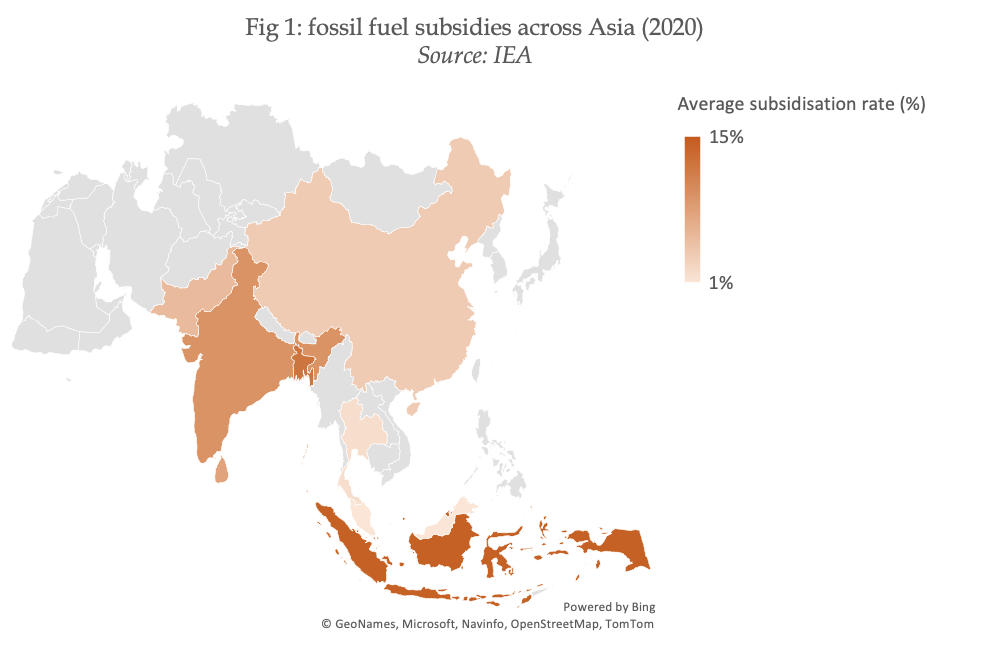

The law of enduring influence applies. One need not look further than the prevalence of subsidies in Asia’s fossil fuel sector to get a sense of the kind of challenge decarbonising Asian energy markets entails (see Fig 1)

Menon mentioned in his remarks: “About 85% of the energy consumed in Asia comes from fossil fuels and Asia’s demand for energy is projected to double in 2030”. This makes the economic, social and political weight of the fossil fuel industries, a force to be reckoned with. A force that, one might expect, will oppose fast-paced decarbonisation given the economic hit it would take. According to the IEA, job losses in Asia’s fossil fuel sector could total 1.75mn by 2030, based on the “announced pledges” scenario.

Skin in the game: the promise of stewardship

The reality is that institutional investors have skin in the game in companies that occupy the commanding heights of Asian energy supply chains. This would imply that, akin to Western practices, engagement is critical.

In July 2022, the Asia Investor Group on Climate Change (AIGCC) released a report that helps shed light on the current state of play.

AIGCC’s report investigated its engagement programme targeted at the utilities sector, which accounts for 23% of global GHG emissions. Investors with a collective assets-under-management (AUM) of $10trn have signed up to the programme.

They have been pushing some of Asia’s most carbon-intensive companies to publish targets, commit to coal phase-outs and provide credible disclosures. For examples, AIGCC members pushed to get Malaysia’s Tenaga Nasional Berhad to commit to a 2040 coal phase-out which led to the company providing updated emission-reduction targets.

As evidence from elsewhere suggests, investor expectations are powerful instruments of change. Whether or not it works in Asia generally, it is too early to tell, but engagement is ongoing, and the evidence from AIGCC seems positive.

Long way ahead

So what is the end game? To start with, targeting a peak for coal consumption in key markets such as India and China is critical. On a recent Net Zero Investor podcast, Nandikesh Sivalingam, director of the Centre for Research on Energy and Clean Air, said: “Even though the consumption of coal is increasing and we see more coal power being generated, the inertia that the sector had five years back, that has died down drastically”.

Building on this fresh, albeit slow momentum, Sivalingam expects to see coal peak in India by around 2030.

On the other side of the equation, keeping the “well below 2°C” vision alive means investments to the tune of $13.9trn in Asia’s green energy supply chains by 2040. Adhering to Paris Agreement targets would mean a highly ambitious target of 50-85% share for renewables in energy supply by 2030 for South and Southeast Asia according to Climate Analytics, a research provider. The equivalent 2019 figure is just 9%.

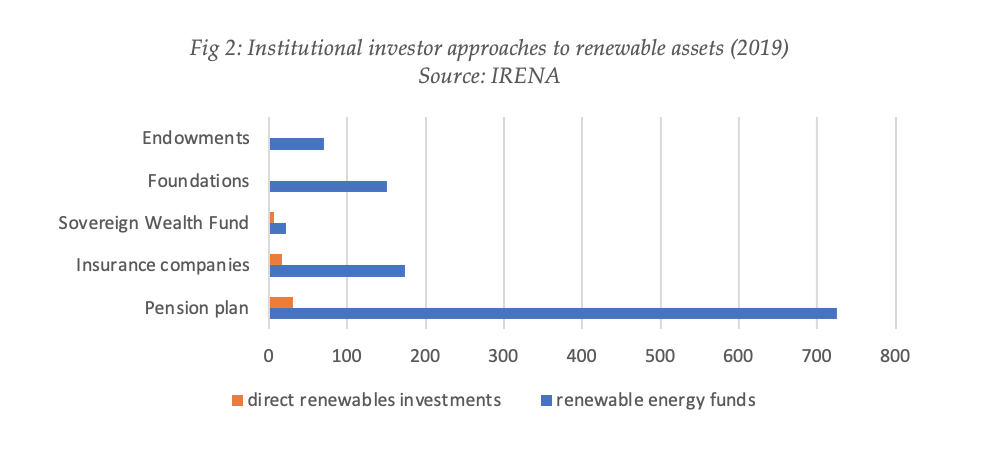

Rapid deployment of institutional investor capital in Asia’s renewable energy assets, is of critical importance. In 2019, a survey by the International Renewable Energy Agency found that institutional investors, including over 700 pension funds, choose to invest in renewables through dedicated funds (Fig 2). Less than 5% of Asia’s surveyed institutional investors have similar exposures.

If what Menon says is right, rethinking Asia’s position in global net-zero portfolios seems apposite. When it comes to achieving climate goals, investors should have eyes on the East.

Atharva Deshmukh is Net Zero Investor’s head of research.