Asset owners turn greener worldwide but dark clouds are gathering fast

For most asset owners decarbonisation is now a key factor when allocating capital, although concerns about geopolitical uncertainty and inflation are growing: 'it's time to be discerning'

Sustainability and impact investing are increasingly dominating the agenda of asset owners around the world, with decarbonisation gaining momentum as a key factor when allocating capital.

However, investors take very different approaches in various parts of the world, and have set priorities and targets vastly different from each other.

Moreover, more than half of all asset owners are anticipate that geopolitical uncertainty and rising inflation will negatively impact their portfolio performance in the next 12 months, combined with tapering of monetary policy and stagflation.

These are the main results from Schroders’ 2023 Institutional Investor Study, a global review of perspectives from 770 pensions, life companies and endowments.

The research shows that sustainability, impact and decarbonisation are themes that run through asset owner attitudes, especially with respect to investment in private markets.

For example, half of all EMEA asset owners view sustainability and impact as important motivators for investing in private markets. However, this is hardly a priority for investors in Latin America, Schroders found.

The asset manager analysed the investment perspectives of 770 global institutional investors on the investment landscape, sustainability and private assets.

The respondents represent a spectrum of institutions, including corporate and public pension plans, insurance companies, official institutions, endowments and foundations, collectively responsible for close to $35 trillion in assets.

Net Zero Investor's Annual Conference | 11th December 2023 | London

Sustainability drive

London-based Andy Howard, global head of sustainable investment at Schroders pointed out that “we are starting to see some new trends emerging as investors continue to grow and evolve their approach to sustainability.”

The report showed that institutional investors are increasingly focused on climate-based thematic exposures and the impact of their investments.

“This implies asset owners want to take a more nuanced approach to sustainable investing than in the past,” Howard pointed out.

“They increasingly consider integration to be a given and instead want to take advantage of more focused opportunities.”

He stressed that “as the world grapples with regime shift and the trends of deglobalisation, decarbonisation and demographics on the investment landscape, sustainability themes are becoming increasingly important, creating new opportunities for companies and investments that provide sustainable products and services. As a result, investors are looking to identify and allocate capital to these emerging sustainable investment themes.”

The research also shows a growing focus on impact investing: 59% identified this as a preferred approach, compared to 34% in 2020.

“What is clear is that asset owners are seeking to deliver positive outcomes by investing sustainably, followed by avoiding harm and supporting transition through active ownership,” Howard noted.

Sustainability themes are becoming increasingly important, creating new opportunities and investments. Investors are looking to identify and allocate capital to these emerging sustainable investment themes.”

However, there are vast regional differences, with integration listed as one of the preferred approaches in Latin America, and representing a sizeable contribution in North America, as opposed to Europe, the Middle East, Africa and the Asia-Pacific region, where it ranks lower.

Engagement themes

Corporate governance has been highlighted as the top engagement theme for the second year in a row, the Schroders report stated.

Climate continues to be a key priority for institutional investors, ranking second globally followed by human capital management.

“This year’s study highlights institutional investors’ desire to see real world investment outcomes through active ownership,” the researchers wrote.

When asked about key features of an engagement strategy, asset owners indicated that their priorities are tangible evidence of real world outcomes (56%) and evidence of improved financial performance (44%).

However, a host of challenges remain. A lack of transparency around sustainability data and reporting (46%) and unclear definitions around sustainability (50%) continue to be a major challenge for investors, whilst performance concerns are still a barrier though less so than in last year’s Schroders survey, namely 46% in 2023 versus 53% in 2022.

Also read

AP6’s green chief on investment choices, pressuring managers and mitigating climate risks

“Sustainability is a complex and multi-faceted topic,” Howard said. “It is also ever-changing, whether that be through new research, expanding data availability, regulation or government action.”

He pointed out that “investors adopt a variety of approaches to sustainable investment, reflecting their values and investment objectives.”

Asset owners mentioned the exclusion of certain activities and sectors (54%) and engagement and voting (52%), which in practice can be used to support all sustainable investment approaches.

Respondents’ focus on impact is clearly growing, rising from 34% in 2020, 48% in 2022 and now 59%. Impact is ranked first by investors across Europe, the Middle East and Africa (63%) and Latin American asset owners (64%).

“This mirrors our experience that a growing number of institutional investors are focusing on understanding the impacts of their investments on real world social and environment challenges,” Howard said.

Decarbonisation

The researchers said they are seeing “a huge surge” in the energy transition around the world as nations move from fossil fuel reliance to greener energy sources.

Countries are likely to rapidly accelerate the decarbonisation of power generation as emissions need to fall by more than 40% in the next seven years as a vital step toward meeting net zero requirements by 2050, the report stated.

“The shift to net zero emissions represents a new key structural trend for the global economy. It will require a radical change in the energy system and in other key sectors of the economy.”

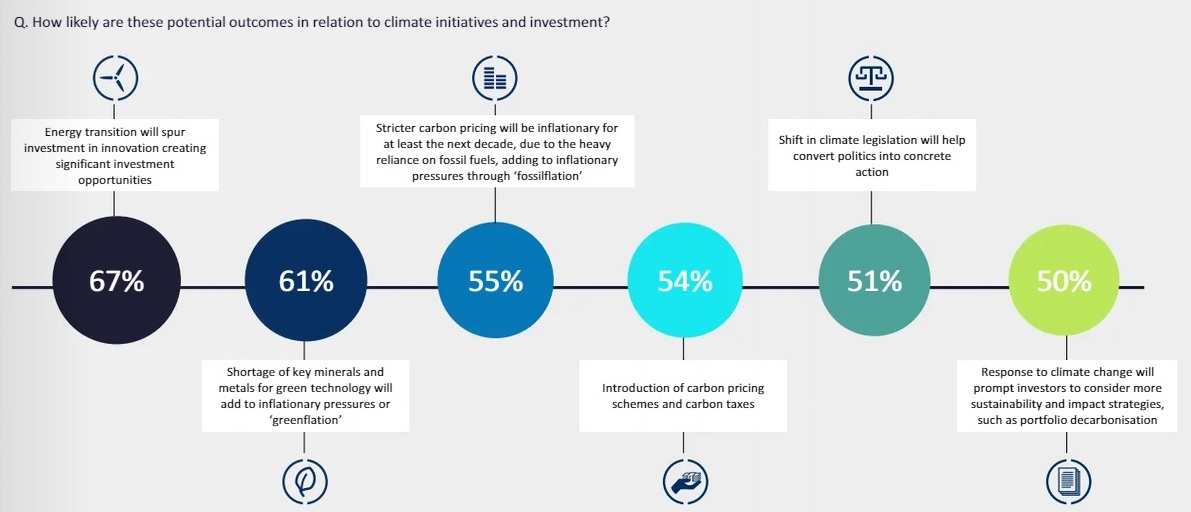

This sentiment is clearly supported by the findings in the report: 67% of investors agree that the energy transition will spur investment in innovation thereby creating significant investment opportunities.

Similarly, 46% of global investors believe that infrastructure/renewables are best and more investment opportunities are presented by the energy transition/decarbonisation though greater exposure to private assets.

At the same time, many investors also think that decarbonisation could have an inflationary impact; 61% agree that shortages of key minerals and metals for green technology will add to inflation.

Meanwhile, 55% think that stricter carbon pricing will be inflationary for at least the next decade.

Regional differences

Regionally, North American investors (68%) and Asian-Pacific region investors (66%) are most likely to agree that shortages of key minerals and materials will add to inflation.

In addition, Asia-based investors (59%) are the most likely to agree that the response to climate change will prompt investors to consider more sustainability and impact portfolios, in comparison to 37% in North America.

Looking at the report, Irene Lauro, an environmental economist in London, said “it is no surprise asset owners expect the energy transition will spur on innovation.”

She sees globally that investment in key technologies is rising, with innovation set to be another important force disrupting the global economy.

“The energy transition will support activity across the entire sustainable energy value chain, creating many opportunities for investors as the expansion of green energy technologies keeps gaining traction."

Looking ahead, dark clouds are gathering though.

Over half of all asset owners expect geopolitical uncertainty (55%) and rising inflation (53%) to have the greatest impact on portfolio performance over the next 12 months.

“Geopolitical uncertainties are putting a four-decade long period of globalisation to the test, not least amid signs the world is heading in a more ‘protectionist’ direction,” the report concluded.

Tapering of monetary policy (48%) and stagflation (42%) follow suit.

“These two issues are directly related, with stagflation that particularly vexing combination for asset values of slowing growth and accelerating,” the researchers wrote.

Regionally, Europe-based investors (59%) are the most likely to have concerns over geopolitical uncertainty, ahead of the Asia Pacific (APAC) region (52%) and North American investors (51%).

This is likely because of the greater impact of the Russia-Ukraine conflict on countries in Europe.

Meanwhile, for North American asset owners, rising inflation appears less of an influence on their portfolios, 50% vs. 55% for APAC investors and 53% for European investors.

Asset owners based in the US and Canada also appear to be less fearful of stagflation, 34% vs. 47% for APAC region investors and 46% for European investors.

“Markets continue to be caught in the cross currents of concerns about rate increases and worries about recessionary risks,” explained Johanna Kyrklund, group CIO and co-head of investment at Schroders.

“Institutional investors’ allocations to equities may increase as asset owners intend to capitalise on the opportunities presented by the deglobalisation, decarbonisation and demographic trends,” she said.

“With concerns about high inflation and high interest rates, valuations matter. A renewed focus on valuations rather than speculative growth may be required,” Kyrklund continued.

In terms of the impact on portfolio performance, the study found that a number of issues are increasingly on the radar of investors: rising inflation, hawkish monetary policy stances, global conflicts and stagflation.

“We believe it’s time to be discerning, analytical and valuation-focused once again,” Kyrklund concluded.

Also read

Why floating offshore wind could be the next frontier in renewables