How climate-driven are stock exchanges in emerging markets?

With equities being the asset class of choice for climate-driven investment in emerging markets, stock exchanges have a vital role to play in facilitating the energy transition

For investors who set sail for net zero opportunities in emerging markets, listed equity is often the first port of call. According to a new survey of asset managers, 81% reported an exposure to listed companies in emerging markets. The survey was conducted by Mercer and covered over 200 global asset managers who collectively manage assets worth $30 trillion.

The results indicate an increasing investor appetite for emerging market listed equity.

“Managers expect asset owner appetite for emerging market allocations to increase, but exposure to private markets, alternatives and real assets remains limited”, the survey says.

While listed equity seems to be the asset class of choice for institutional capital, the underlying strategy of investing in the energy transitions in emerging markets is simultaneously shaping asset allocations.

Listed equity-driven asset allocations into emerging markets point toward the importance of stock exchanges in facilitating a climate-friendly interaction between asset owners, asset managers and asset classes.

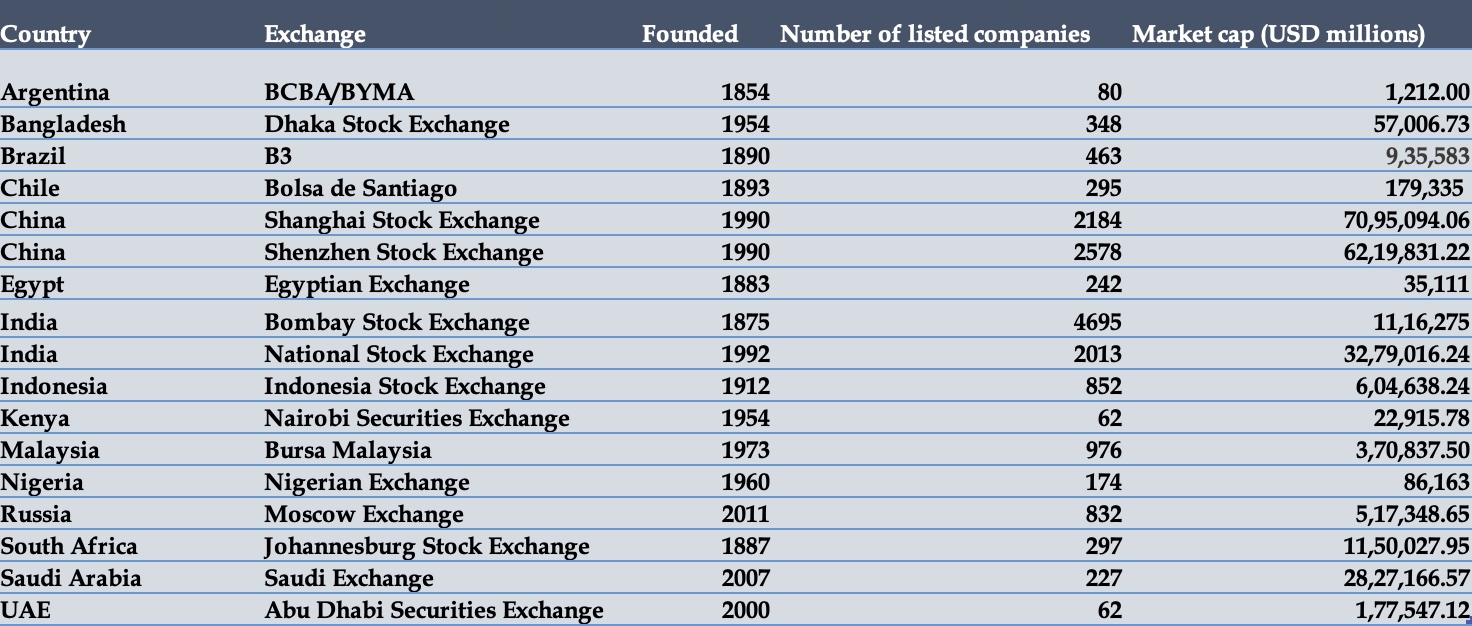

Just how climate-driven are stock exchanges in emerging markets? Data from the sustainable stock exchanges initiative, helps shed some light on a fundamentally multi-faceted question.

Managers expect asset owner appetite for emerging market allocations to increase, but exposure to private markets, alternatives and real assets remains limited

Age and maturity in Asian exchanges

Historically - most, not all, of the developing world relied on debt markets to finance growth. The emergence of equity financing is therefore a relatively recent phenomenon in some cases. Consequently, institutional experience varies across countries. Some exchanges have been around for longer.

China’s Shenzhen stock exchange is young – it has its roots in the early 1990s when Beijing decided to introduce stock markets into the Chinese economy. India’s Bombay Stock Exchange, on the other hand, is over 143 years old. Established in 1875, it was Asia’s first stock exchange.

Age, however, has little to do with scale and maturity. Despite their recent emergence, China’s stock exchanges are much larger in market capitalisation terms. The Shanghai stock exchange, also formed in 1990, has a market capitalisation of over $7 trillion. Some of China’s largest companies in renewable energy are listed on the Shanghai exchange – including China Three Gorges Renewables, which operates the world’s largest hydroelectric power plant.

Across Asia, stock markets have deepened and matured. Even though exchanges in other regions such as Latin America are much older. Stock exchanges in China, Malaysia, Indonesia and India are examples of this trend.

“Asia is the most prevalent region for investment, while public equity is the most commonly invested asset class across all regions”, the Mercer survey found.

Listing rules

A defining feature of climate-driven stock exchanges is the set of listing rules that companies are subject to. The extent to which these rules incorporate environmental disclosures and standardize their measurement is therefore a crucial factor.

Several stock exchanges in emerging markets require listed companies to provide environmental disclosures, often clubbed together with wider ESG disclosures. In Indonesia, for instance, 852 listed companies are required by the country’s Financial Services Authority to submit annual sustainability reports.

In 2021, Kenya’s stock exchange released detailed guidance on environmental disclosures for listed companies, which is now a requirement imposed by the exchange. At the time, the director of the Nairobi Securities Exchange, Isis Nyong’o Madison said, “This is a major step towards making finance more sustainable, in order to ensure better allocation and channelling of capital towards sustainable and transitioning assets”.

Not all exchanges see eye to eye with Madison. Exchanges in Bangladesh, Chile and Russia do not require listed companies to comply with any disclosure rules. Even in China, disclosures were introduced in phases and selectively applied. For instance, until 2017, only “key polluter” companies were subject to mandatory disclosures. China’s mainland exchanges still lack coherent, mandatory disclosures as part of listing requirements.

Green bond segments

For investors, fixed income is the second-most attractive asset class in emerging markets. 40% of respondents to the Mercer survey said they had exposure to fixed income assets (in emerging markets). Here too, stock exchanges have a role to play.

Some exchanges have provided a platform for investors to access green bonds. South Africa’s Johannesburg Stock Exchange listed its first green bond 10 years ago. The relatively small issuance of $140 million bond was offered by the city of Johannesburg.

Over the years, issuances have increased in value. In 2022, the Abu Dhabi Securities Exchange announced the secondary bond listing for Sweihan PV Power Company which operates one of the world’s largest solar plants - Noor Abu Dhabi. The company raised $700 million through the bond listing.

India’s National Stock Exchange offers investors access to the country’s sovereign green debt instruments maturing in 2028 with an average yield of 7.2%. Following India’s entry introduction into the sovereign debt issuers club in 2023, the country’s stock exchanges have played a vital role in raising debt capital aimed at financing grid scale solar and wind projects.

Here too, not all exchanges think alike. Malaysia’s Bursa Malaysia has a market capitalisation of over $370 billion but does not offer a sustainable bond listing segment. Neither do exchanges in Bangladesh, Kenya or Egypt.

Exchanges in emerging markets differ in their climate awareness. While some have embraced standardised disclosures and green bond segments, others have yet to join the conversation. As capital allocations into these economies increasingly favour both listed assets and transition-linked opportunities – stock exchanges will become a critical piece of the net zero investment puzzle in emerging markets.