Is the dominance of the magnificent seven bad news for your carbon footprint?

Could US stock market concentration become a stumbling block on the road to net zero?

Global stock market concentration has been at the front of many investors mind, nowhere more so than in US, where the “magnificent seven” (Mag 7) command nearly a third of the S&P500. While this has been identified as a potential investment risk, could it also become a problem on the road to net zero?

Equities are still a cornerstone of many institutional portfolios. They account for more than half of the average Australian portfolio and 47% of US pension investment, according to the Thinking Ahead Institute’s latest asset allocation survey. Equity allocations are lower in Europe and Japan, where they hover around a third of the average pension portfolio.

Moreover, the Mag 7 have also been a key driver of stock market returns accounting for almost half of all S&P500 growth over the past year. Given their dominance in developed market indices, the Mag 7 are likely to feature in institutional equity portfolios.

The picture is particularly striking for defined contribution funds which tend to have higher allocations to equities. For example, the Mag 7 stocks alone account for 8.5% of Nest’s 2040 Retirement Countdown Fund and are also the fund’s top seven shareholdings.

But the climate impact of the world’s biggest tech firms has so far received relatively little coverage. Net Zero Investor took a closer look at the carbon footprint of the Mag 7 stocks, Amazon, Alphabet, Apple, the Meta Platforms, Microsoft, Nvidia, and Tesla.

Moore’s emissions

While the road to net zero is often seen as a linear path as fossil fuels are gradually being replaced by renewables, the Mag 7 pose a significant challenge to this idea of linearity.

While it is hard to generalise across seven businesses that range from social media platforms over electric vehicles to microchips, there are some commonalities. For one, these businesses are not only growing exponentially, they tend to be energy intensive.

Six of the Mag 7 largely rely on computing power to provide technology, products and services. To that end, their operations run on two resources – electricity and water. Their use is concentrated in data centres, where Moore’s law comes to life.

Moore's law, named after Intel co-founder Gordon Moore, observes that the number of transistors in an integrated circuit doubles about every two years. In a nutshell, this means that the amount of energy required to power microchips is declining rapidly, a powerful driver to reduce the carbon footprint of these tech firms. The question is whether Moore’s law can keep up with the rapid growth of the sector.

Ambitious targets

Another common theme for the Mag 7 is that they tend to have ambitious net zero targets in place.

Alphabet plans to half its carbon footprint across Scope 1, 2 and 3 by 2030. Scope 3 emissions currently account for more than 75% of the overall emissions but water usage and the recycling of existing products could become key stumbling blocks.

The picture is very similar for Amazon, Apple, Meta and Microsoft, where Scope 3 emissions also account for the bulk for their carbon footprint. NVIDIA and Microsoft stand out for showing a relatively higher commitment to net zero.

Microsoft, for example aims to be carbon negative by 2030. It plans to deliver on that largely through investments in its climate innovation fund. By the end of the decade, it will still emit 5MMTCo2e. It intends to expand its “carbon removal” assets such as forestry and soil to such an extent that they effectively offset its existing carbon footprint.

Tesla is somewhat of an outlier on net zero targets, it is the only one of the Mag 7 that does not have a clear deadline in place and is only gradually starting to disclose its carbon footprint. Supply chain emissions are a major stumbling block for the EV manufacturer. While its Scope 1 emissions account for only 2 MMTCo2e, its supply chain emissions are estimated to account for at least 30 MMTCo2e.

Net Zero Investor's Nature Positive Investment Forum

24 April, London Stock Exchange sign up here

Shift to renewable energy

To mitigate their impact, tech companies are increasingly switching towards renewables. Take for instance, NVIDIA – the company that has dominated headlines in recent times.

In the 2023 financial year, NVIDIA purchased 249,429 MWh of non-renewable energy. The remaining 44% of NVIDIA’s energy consumption was supplied from renewable energy sources. By 2025, the company is aiming to get that number up to 100%. Currently, a third of its data centres run on renewable electricity.

“Data centres are already about 1-2% of global electricity consumption and that consumption is expected to continue to grow. This continued growth is not sustainable, neither for operating budgets nor for our planet” says Jensen Huang, the company’s chief executive.

For companies such as Alphabet, which runs 200 data centres in 60 countries, Mr. Huang’s concerns seem both real and consequential.

Powering their operations with renewable electricity is a focal point in transition planning at other Mag7 members too. Amazon, Microsoft and Meta all market themselves as one of the world’s largest purchasers of renewable electricity.

“We are the largest corporate buyer of renewable energy in the world for the third year in a row" says Kara Hurst, VP, worldwide sustainability at Amazon in the company’s latest sustainability report.

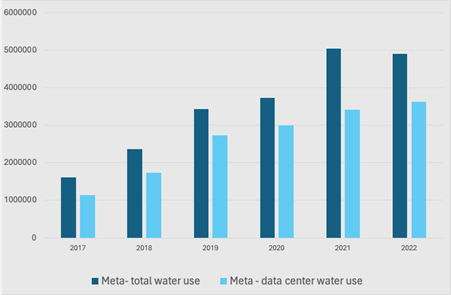

In addition to electricity to power them, data centres use large amounts of water for cooling.

“Within our global footprint, our data centres generate the highest percentage of our energy use, water use and GHG emissions” says Rachel Peterson VP, data centre strategy at Meta.

Over 70% of Meta’s water use is attributable to its data centres:

For Tesla too, efficient water use is part of the company’s identity. Its lower per-unit water use is what sets it apart from competitors using internal combustion engines.

Mag7 Investment Inc.

A few of the Mag7 are also investors in their own right. They have direct and sizeable investment exposure to the world of climate solutions and climate technology.

In 2020, Microsoft launched the climate innovation fund, with the goal of investing $1bn in climate technology. Since its inception the fund has invested early-stage capital in companies working on sustainable aviation fuels, direct air capture and energy efficient construction technology.

In 2019, Amazon set up a dedicated fund for venture capital financing for climate technology soon after. The “Climate Pledge Fund” has an initial funding of $2 bn. So far it has invested in well-known companies such as Rivian - the electric vehicle manufacturer, ZeroAvia - the sustainable aviation company and Moxion Power – a battery technology company providing clean energy to film production companies including Amazon.

More recently, Apple joined the ranks through its “Restore Fund” which invests in “nature-based carbon removal projects”. In April 2023, the company pledged another $200m to the fund.

Limits of growth

Overall, the Mag 7 appear to perform relatively better on net zero targets compared to some of their large cap peers, a reason which might explain why they feature prominently in climate-tilted indices. These will continue to be resource-intensive businesses. But so far, they have faced almost no investor pressure.

Last year, just three of the seven firms faced climate-related shareholder resolutions at their AGM's. None of the proposals dealt with operational emissions reduction and all were rejected by the boards.

So far, their transition strategy has focused on powering data centres with renewable energy and financing climate solutions. As institutional portfolios embrace the financial attractiveness of the Mag 7, the effectiveness of the latter's emission reduction plans might increasingly come under scrutiny".