Never let a crisis go to waste: inside the WEO 2022

Net Zero Investor’s head of research delves into the World Energy Outlook 2022, a report documenting how today’s energy crisis could change the trajectory of the transition.

Each year, the International Energy Agency (IEA), issues a report that documents in detail its observations of and predictions for the global energy system: a finger on the pulse, if you will. The World Energy Outlook (WEO) is, consequently, a report tracked by many.

This year, the pulse revealed an energy crisis as ubiquitous as it is complex. Yet, WEO 2022 finds space for gradual optimism and echoes Winston Churchill’s logic for forming the United Nations in the aftermath of the Second World War: never let a [good] crisis go to waste.

The crisis in question is the global energy market shock that emanated from Russia’s invasion of Ukraine and led to the weaponisation of energy supply chains, surging energy prices and rampant inflation. Gas prices and European markets, according to the IEA are the primary, although not the only, causes of the crisis. Looking at the data, the IEA notes: “Oil has been expensive before, but there is no precedent for the import bills for natural gas in 2022.”

Looking back

The WEO 2022 begins with a reminder: energy crises are a defining feature of global economic history. Always were, always will be. In most cases, the story is a familiar one: a country, or a group, that exerts overwhelming political influence on energy markets manipulates supply, leading to higher prices, inflation and, consequently, economic carnage in importing countries. In other words, crises have been about asymmetries in resource endowment – who has how much? – and dependence – who supplies who?

The most notable of energy crises were the oil price shocks of the 1970s. The IEA itself was formed in 1974 as a response to one of them. The WEO 2022 suggests that although what happened in the 1970s shares some common traits with 2022’s crisis, the latter is more complex. This is mostly because the 1970s were about oil, and today’s crisis has multiple moving parts – oil, gas, electricity, renewables and so on.

This matters for how governments respond: in the 1970s, the prescription was “reduce oil dependence”, but in 2022, the WEO prescription reads “change the nature of the energy system itself”.

According to the IEA: “The starting point for today’s decision-makers is fundamentally different from that facing their counterparts in the 1970s.” The symptoms might be similar, but this is not the same patient and probably not the same illness.

Energy crises incentivise governments to move to protect consumers by controlling rising energy prices and securing energy availability by all means necessary, even if it requires looking towards fossil fuels.

Net-zero silver linings

When the IEA says the starting points are different, does that matter? In short, yes. This is the source of the IEA’s gradual optimism and the crux of WEO 2022.

The concern with energy crises is that they incentivise governments to move to protect consumers by controlling rising energy prices and securing energy availability by all means necessary, even if it requires looking towards fossil fuels. There is some evidence of this happening in Asia and Europe, said Laura Cozzi, a co-author of WEO 2022, at the launch. IEA executive director Fatih Birol reiterated these concerns. “Is the current energy crisis going to slow down or accelerate clean energy transitions?” Birol asked.

Yet, the data shows that a slowdown is unlikely. The main reason is that, compared to the past, today’s crisis responders have more tools at their disposal, including a pivot to clean energy technologies that does not seem far-fetched. A crisis playbook, with the silver lining of net-zero prospects.

In the years leading up to 2022, governments had been increasing clean energy investments, albeit at modest growth rates. Over the past two years, this increase has become more pronounced. Governments across the world are expanding clean energy investments at unprecedented rates. How do we know that?

The WEO cites cases from across the globe, from Japan’s “green transformation” programme and the European Union’s “Fit for 55” package to the US’s Inflation Reduction Act, and finds signs of momentum. Some emerging markets have signed up as well. China has increased the ambition of its clean energy targets and India has embraced solar as the pillar of its transition.

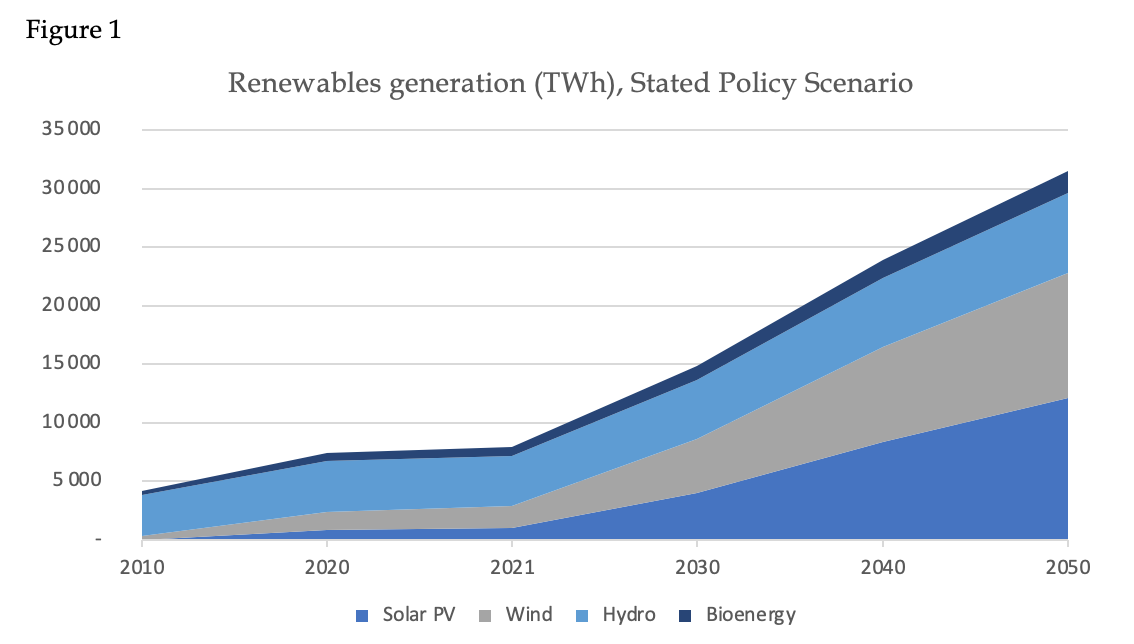

This is momentum of some magnitude. So much so that the IEA’s expectation is that these policies translate into $2trn in clean energy investments by 2030. It still falls short of the $4trn needed to align with the 1.5°C scenario, but one can hardly ignore the historical significance of this momentum: The IEA’s prediction of a 90% increase in renewables generation by 2030 is noteworthy to say the least (see Figure 1).

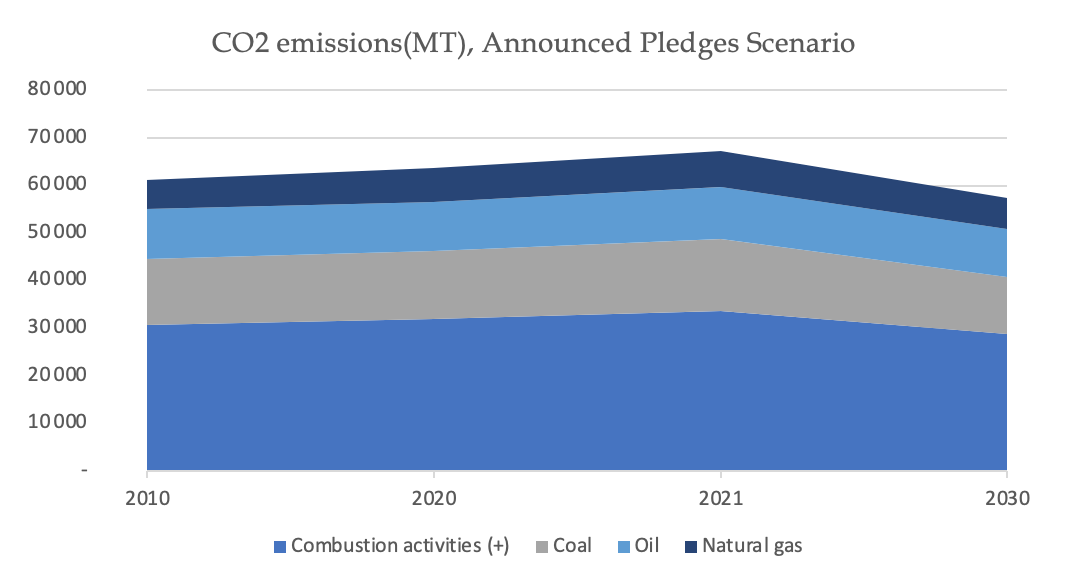

The second source of the IEA’s gradual optimism is fossil fuel peaks. The turn towards fossil fuels as a response to the crisis, that Cozzi mentioned, is temporary according to the WEO data. For the first time in its history, the IEA is forecasting fossil fuel demand to peak and emissions to fall within this decade (Figure 2).

“Fossil fuel emissions have risen every decade since the industrial revolution” said Tim Gould, another WEO co-author. Gould’s point was that going forward, all the IEA scenarios expect rising growth, rising energy demand, but diminishing use of fossil fuels based on how governments have responded to this crisis. “That is why we are calling this a pivotal moment in energy history”, said Gould.

Is the current energy crisis going to slow down or accelerate clean energy transitions?

Geopolitical cause and effect

Finally, the WEO reminds us that when it comes to energy, one cannot ignore politics Every energy crisis has a geopolitical cause and effect.

Russia’s role in the 2022 crisis, and Europe’s response, means that a core artery of global energy trade has reached a point of no return. Gould stated at the launch: “We assume there is no way back for the EU-Russia gas relationship. That relationship was built up over 50 years on the basis of trust and that trust has disappeared.” The WEO predicts in no uncertain terms that the “golden age” of gas trade is over largely as a consequence of this shift.

On the other hand, politics matters for the transition too. The WEO 2022 argues that if we have learnt anything from this crisis, it is that political fragmentation and friction do more damage than we think: “The crisis has undercut the trust and collaboration that are essential to ease the journey to a net-zero emissions system. A lack of sequencing and co‐ordination, both within countries and internationally, would also be very damaging to the prospects for a people‐centred process of change”.

A “messy transition”, as the report calls it, is likely but could be avoided. It all depends on what this crisis is remembered for.

Atharva Deshmukh is Net Zero Investor’s head of research.