Piling up: complex, time-consuming climate reporting increasingly a daunting task

Amid globally expanding sustainability standards, with the ISSB taking centre stage, reporting requirements are increasingly draining time and resources

The sustainability reporting landscape is rapidly consolidating, with the green principles of the International Sustainability Standards Board (ISSB) gaining momentum worldwide.

Aligning with a recognised reporting framework is crucial to increase transparency and provide a more detailed focus on relevant data and KPIs.

That is why investors around the world are generally enthusiastic about the ISSB's inaugural ESG standards, particularly since more and more countries are confirming they plan to adopt or implement the principles.

For example, key players in the world of sustainability reporting standards and the wider investment community responded overwhelmingly positive to the recent announcement by the UK government to largely duplicate the ISSB framework.

However, as reporting requirements become more detailed, more in-depth and more tailored, they are increasingly taking up large amounts of time and resources at investors, their investee companies, banks and other key actors.

In fact, at nearly three in four companies now three or more internal teams need to scrutinise and sign off on any climate statements, sustainability reports or related disclosures.

Moreover, most impacted entities have appointed at least one employee to oversee climate-related reporting, a jump of 6% compared to last year, according to fresh data that was shared with Net Zero Investor.

The need to have dedicated staff is underpinned by the fact that most companies are now required to comply with two or more global regulations, the research from the London Business School found.

That is why the general consensus within the community is that ISSB's ESG standards offer several advantages. They establish a global set of sustainability disclosures, creating a common baseline for issuers of all sizes, sectors, or locations.

This uniformity in communication drives convergence with other reporting requirements and efficiencies in data capture across geographies.

It enables companies to deliver robust reporting efficiently and cost-effectively, particularly beneficial for businesses operating in multiple jurisdictions.

Discussing the research findings with Net Zero Investor, Alex Edmans, professor of finance at London Business School, said that “what struck me is the dichotomy between practitioners of all levels agreeing they find value in climate reporting while managers in the trenches are saying their companies are not applying the same diligence to such reporting as they do to financial reporting.”

Edmans and his team found that, while 62% of C-level executives strongly agreed that their companies apply the same level of diligence to climate reporting as they do to financial reporting, only 32% of managers and senior managers share the same sentiment.

Likewise, nine in ten executives said their organisations have appointed someone to an ESG-specific role, compared to less than seven in ten of managers who said the same.

This suggests a significant disconnect between senior leadership and staff and could mean businesses are not fully prepared to comply with emerging climate regulation, Edmans warned.

Also read

Uncle Sam vs John Bull: the irresistible investor appeal of Biden’s IRA

For the survey, 926 professionals took part in the U.S., UK, Germany, France, the Netherlands, Australia, Japan, and Singapore.

For Edmans, it was no shocker that businesses dedicate more time and resources as “it’s no secret ESG is receiving heightened attention in boardrooms or that increasingly complex frameworks, standards and regulations are presenting new challenges in reporting."

"Managers in the trenches are saying their companies are not applying the same diligence to climate reporting as they do to financial reporting.”

Executives overwhelmingly agreed that there is value to be found in sustainability reporting, with 90% of respondents to Edmans' survey stating that in the next two years having a strong reporting programme will give their organisations a competitive advantage.

Additionally, results of the Workiva-commissioned research further indicated the longer a company has been reporting on climate and ESG issues, the more likely they are to have realised a return on their green initiatives.

Respondents from organisations that have been reporting on their green efforts for five years or longer are more likely to state that ESG has generated cost savings and improved brand awareness and reputation for their companies, compared to those that have been reporting on ESG issues for two years or less.

Global standard

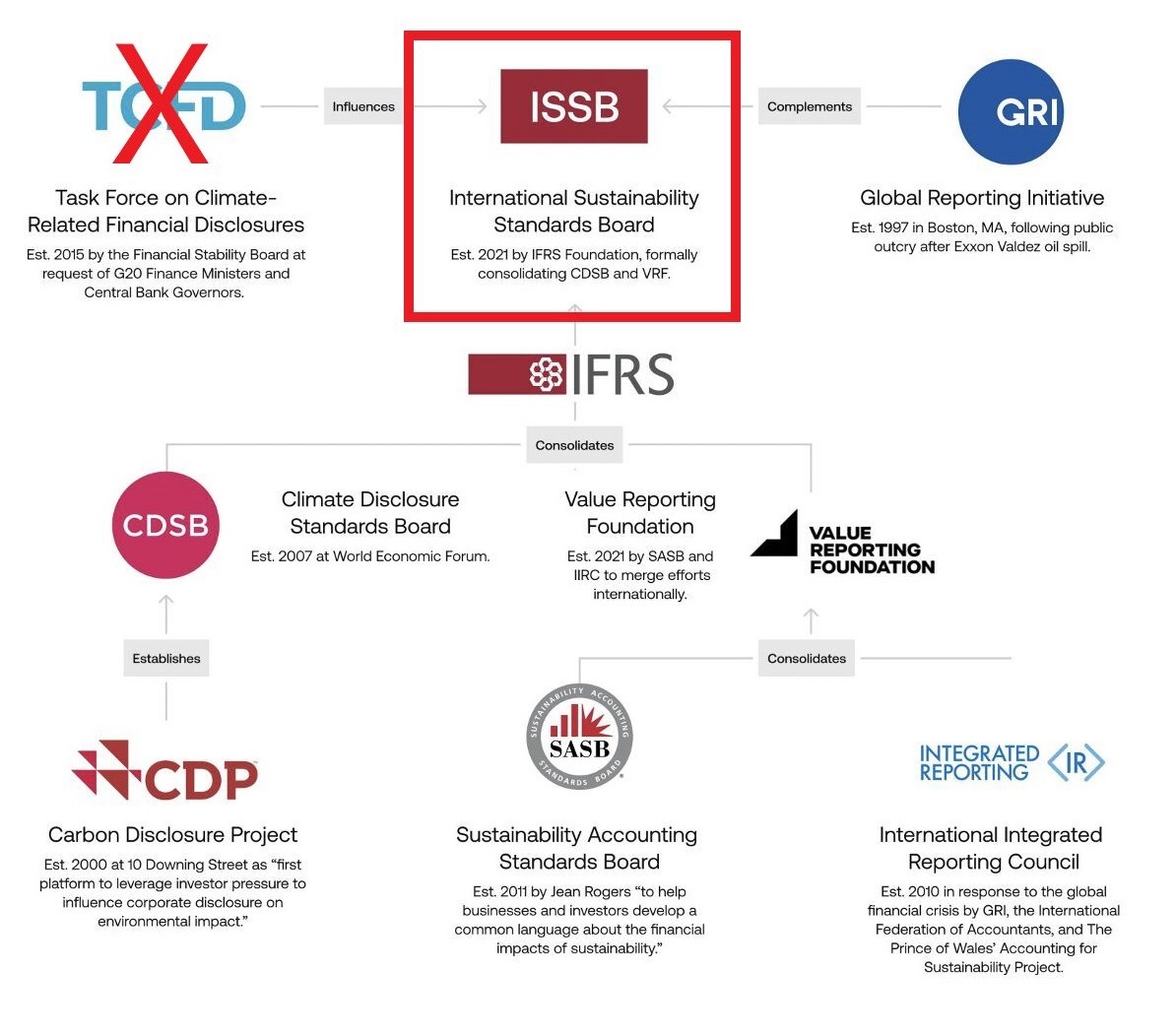

All reporting eyes are now on the ISSB. Initially launched following the COP26 climate conference in Glasgow in 2021, the ISSB aims to develop standards for a global baseline of sustainability disclosures.

The framework enables companies to provide comprehensive sustainability information to global capital markets.

Last month, it was confirmed that the ISSB is to merge with the Task Force on Climate-Related Financial Disclosures (TCFD), considered a critical step forward in unifying the current climate disclosure maze, even though the decision was met with scepticism by some industry insiders.

However, the adoption of the ISSB's standards could still present potential challenges.

The global applicability of the ISSB's standards depends on individual countries and companies' willingness to implement them, which could be challenging due to varying regulatory landscapes and enforcement mechanisms.

The standards demand high transparency and detailed reporting, posing a challenge for companies lacking the necessary systems or processes.

"Meeting these requirements may necessitate investment in new technologies or processes, which could be costly and time-consuming," stressed Paul Woods, director of sustainability & ESG at UK-based Arrow Global, a European-focused alternative asset manager specialising in private credit and real estate.

Woods' statement is backed up by the London School of Economics survey as there is a growing belief among practitioners that technology is a key component of any sustainability reporting regime.

Nearly all respondents (95%) agreed that having adequate technology is critical to successfully managing the climate reporting process, an increase of nearly a fifth compared to last year, and close to all agreed that access to technology and data will play an essential role in making decisions to advance their ESG strategy.

Woods added that "the introduction of the ISSB's standards could also lead to a polarisation of reporting frameworks, causing inconsistencies and complicating comparisons."

In what was hailed as a major victory for the ISSB, the UK government announced recently that in Britain, the country's upcoming corporate disclosure scheme - the Sustainability Disclosure Standards (SDS) - will be underpinned by the reporting principles of the ISSB.

The SDS will use the ISSB framework as a baseline, with plans for the new regulation to be rolled out by July of next year. It will be a disclosure scheme covering sustainability-related risks and opportunities that companies face.

The British government stressed any “UK endorsed standards will only divert from the global (ISSB) baseline if absolutely necessary for UK specific matters.”

The UK's move to follow the ISSB's approach has also been welcomed by Mark Babington, the executive director of regulatory standards at the Financial Reporting Council, the watchdog responsible for regulating auditors, accountants and actuaries, and setting the UK's Corporate Governance and Stewardship Codes.

However, Babington did warn: "There is a process which needs to be followed."

He told Net Zero Investor: "We're working with the government and other regulators to basically develop a mechanism to endorse the use of the ISSB in the UK."

Babington pointed out that pressure on investors, managers and investee companies is likely to jump significantly, particularly since the government will still need to consider which companies they want to report using the standards.

"This measure is being implemented by the UK to restore its competitive position as an internationally desirable venue for businesses."

"Just like financial reporting, reporting on sustainability issues will be taken into consideration when making resource-allocation decisions."

Using the ISSB norms will make UK company disclosures comparable for investors globally, the UK government clarified.

"The disclosures required by these standards will help investors to compare information between companies, thereby aiding decision-making; supporting the efficient allocation of capital, and smooth running of the UK’s capital markets," it added.

Alexis Normand, chief executive of carbon accounting firm Greenly, said that “UK adoption of these standards is a significant step in the right direction when it comes to consolidating the fragmented landscape of disclosure frameworks globally."

But he stressed: "Just like financial reporting, reporting on sustainability issues will be taken into consideration when making resource-allocation decisions."

To assist with implementing the ISSB’s first two standards, IFRS S1 and IFRS S2, within the upcoming SDS, the UK government has established two committees, the Sustainability Disclosure Technical Advisory Committee, and the Sustainability Disclosure Policy and Implementation Committee (PIC).

PIC’s membership consists of UK government departments and regulators, including the Bank of England, the Department for Energy Security and Net Zero, the Department for Environment, Food and Rural Affairs, and the Financial Conduct Authority (FCA).

Also read

Nature finance: are biodiversity credits moving too fast?