Green investment efforts fading as support for net zero votes evaporates

Net zero efforts among investors are stalling in a number of key markets, most notably the U.S., as support for green motions is declining rapidly

As this year's proxy season is over, it is becoming increasingly evident that net zero efforts are stalling in a number of key markets, most notably the United States, the world's largest investment space.

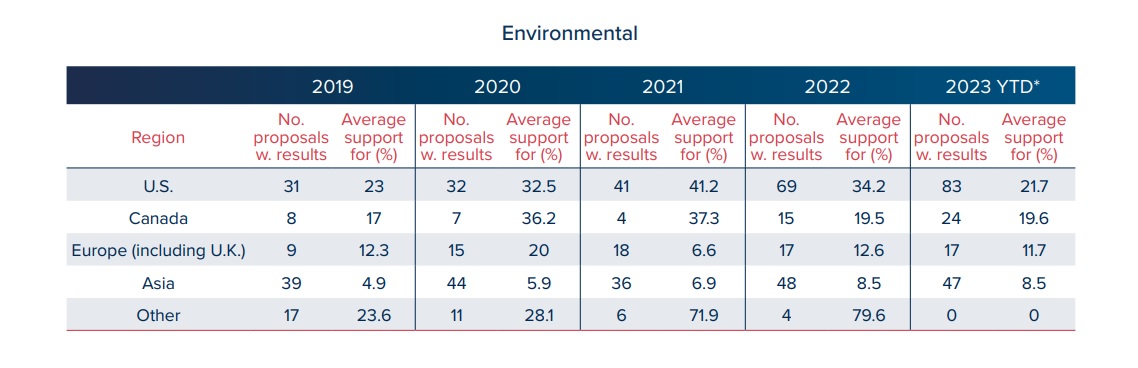

In fact, there is less appetite for green shareholder proposals across the board, with only 2.4% of environmental-related motions winning majority support this proxy season, compared to 10.1% in 2022.

The major decline is largely driven by the impact from this year’s newly enacted universal proxy card (UPC), including its effects on activists’ success rates and proxy fights, according to a new analysis by Diligent Market Intelligence, shared with Net Zero Investor.

A universal proxy card lists the names of all duly-nominated director candidates for election at an upcoming shareholder meeting, regardless of whether the candidates were nominated by management or shareholders.

Prior to the rule’s adoption, companies and dissident shareholders sent separate proxy cards listing only their own slate of nominees for board of directors. It was difficult for shareholders to mix and match management and dissident nominees unless they attended a company’s annual meeting in person.

In addition to the rule change, a number of global trends, such as the impact of ESG against a backdrop of politicization and inflation, have forced investors to abandon their investee companies' net zero ambitions.

Primary examples here are Europe facing a near-unprecedented cost-of-living crisis and Asia experiencing another year of increased demands to improve investment returns.

For activists, this was a less active year than it might otherwise have been thanks to a banking crisis, depressed European markets and a dearth of M&A.

Only in Asia – and notably in Japan and South Korea – did proxy fights really take off, according to Josh Black, vice president at Diligent.

And despite none of the five climate change shareholder proposals in the European energy sector winning majority support this year, average support has increased to 14.3%, compared to 10.2% in 2022.

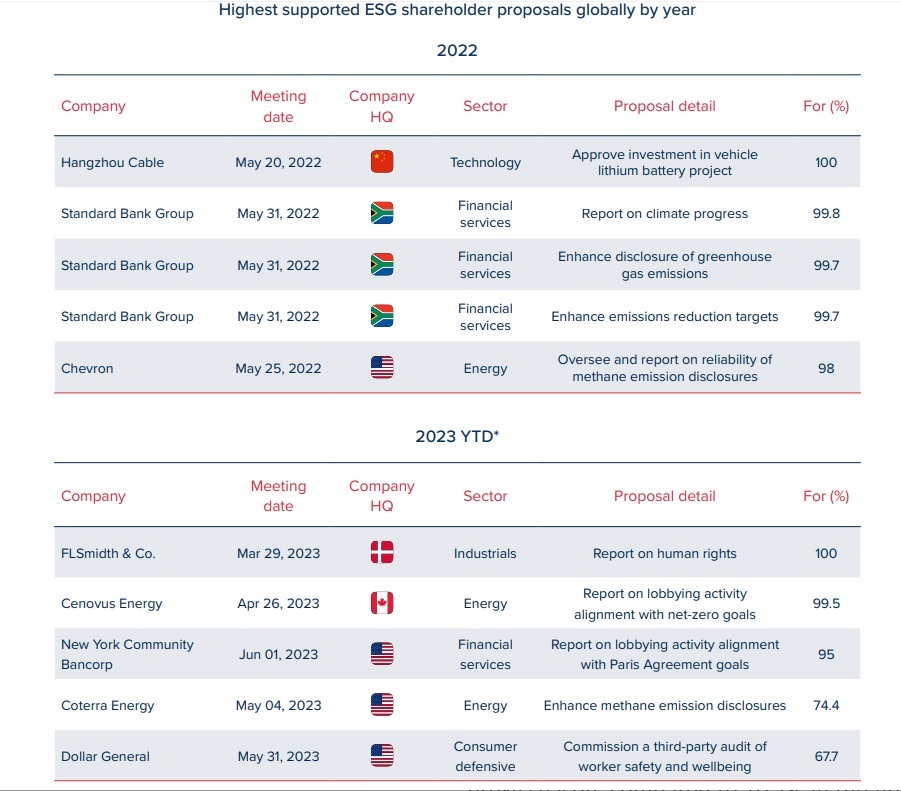

One such proposal seeking medium-term Scope 3 emissions targets at TotalEnergies won 30% support, up from 17% support the last time it was subject to a vote in 2020.

"Only in Asia – and notably in Japan and South Korea – did proxy fights really take off."

"While the U.S. proxy season was dominated by the introduction of the universal proxy card and battles over ESG against a backdrop of politicization and inflation, Europe faced a cost-of-living crisis and Asia another year of radical demands to improve returns," Black commented.

"These real-world factors impacted hundreds of shareholder meetings this year," he added.

"So, for ESG supporters, this was another mixed year. Support for environmental and social shareholder proposals was mostly down in the U.S. and Europe, where they are most common."

The picture, however, was somewhat clouded by a wide variety of motions, including some anti-ESG proposals that dragged down averages.

"A strong pass rate for climate change proposals in the U.S. is worth calling out, as is the appeal of pro-union and lobbying disclosure proposals. Such issues prove that support for ESG is not all dried up," Black continued.

Managers

Black's findings were underpinned by a new report this week that concluded that support for climate-related resolutions was on the rise until last year, when a considerable drop took place, with the average asset manager supporting just 50% of climate-relevant resolutions.

Particularly, U.S.-based asset managers displayed a trend of voting against a large portion of climate-related resolutions in 2022.

The average U.S. manager supported just 36% of climate resolutions, compared to 50% in 2021, InfluenceMap found, as reported by Net Zero Investor yesterday.

For instance, a number of the asset managers assessed were unsupportive of scope 3 emissions disclosure as part of the U.S. SEC climate disclosure rule, including BlackRock, Vanguard, and J.P. Morgan Asset Management.

This U-turn comes as an anti-ESG movement is rapidly gaining momentum in the world's largest investment market, with some state legislators seeking to limit investors’ use of ESG factors and the phase-out of fossil fuel investments.

In fact, with $72 trillion in cumulative assets under management, the world's 45 largest asset managers "continue to hold equity investment portfolios misaligned with Paris Agreement goals, while their efforts to drive the transition through stewardship have stagnated," the report stated.

Discussing the recent trend, McKenzie Ursch, legal advisor at activist shareholder group Follow This, attributes the dwindling shareholder support for climate and net zero-related motions to a change in tack on the part of proxy advisors.

“If you look at the support our proposals have received in the past, both Institutional Shareholder Services and Glass Lewis have tended to support us,” Ursch said.

“This year, we only received support for our resolution at TotalEnergies from ISS, and that doesn’t really make sense."

He added that "Chevron and Exxon Mobil are miles behind where TotalEnergies is in mitigating their climate impact, so to advise for a proposal at TotalEnergies and against identical ones in the U.S. doesn’t make sense.”

Follow the money

Finally, Black singled out one topic that combined ESG, activism and shareholder proposals in 2023, namely remuneration.

This proxy season saw a spate of remuneration-themed shareholder proposals, mainly asking that severance packages be put to a shareholder vote.

"Rebellions on 'say on pay' votes were flat or down in almost every region, suggesting lessons had been learnt from past proxy seasons," Black concluded.

Also read

Most management giants misalign as net zero efforts dwindle