Room to Play: How stock market listing impacts Asia’s largest emitters

Climate laggards in Asia tend to have free float of less than 50%, does this affect their climate ambition?

In 1992, Deng Xiaoping – the former Chinese leader - toured southern China in a quest to fine tune China’s economic reforms. In so doing, the then 87-year asked a critical question – “are stock markets good or bad?”

There was only one way to find out. Deng Xiaoping’s southern tour unleashed a wave of public listings.

China was not alone. By the turn of the millennium, Asia’s corporate behemoths lined up to register their equity on the region’s stock markets.

But public offerings come with much more than just capital. Climate engagement is one of many side effects – with ownership and control up for grabs, listing allows investors to steer domestic decarbonisation.

Yet, engagement in Asia is far more complex. Some large emitters list only a portion of their equity, which could constrain investor engagement in the region.

Using publicly available information on Asia’s largest listed emitters, Net Zero Investor research suggests a link between free float, the proportion of unrestricted shares in total equity, and climate ambition:

62% of Asia’s climate laggards have a free float of less than 50%.

The List

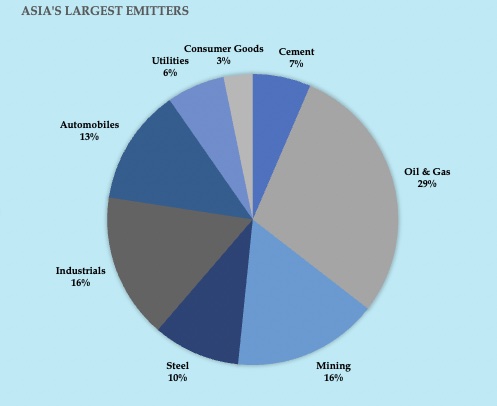

Investor coalition Climate Action 100+ publishes a focus list – 171 companies that the group believes are at the heart of the global race to net zero. Of these, 34 are in Asia.

A closer look reveals that these companies operate in eight key sectors – ranging from oil and gas and mining to steel and automobiles. With a collective market cap of $3.2 trillion, they are some of the region’s largest and most profitable enterprises.

The laggards and their float

Based on the last round of CA 100+ assessments, companies in Asia can be classified based on their climate ambition. This reveals that 16 companies on the Asia focus list had still not set credible targets to achieve net zero by 2050 or sooner. If partial targets are considered, that number rises. Why then, is climate ambition lacking?

A striking trend in the data is that 62% of these laggards had a free float of less than 50%. For these firms, investors' room to engage with these firms was restricted to less than half of the firm's equity.

There are two main sources of this constraint: First, in many cases the parent company and promoters hold a controlling stake.

Consider the case of United Tractors, the Indonesian industrials conglomerate. Even though its shares trade on Jakarta’s stock exchange, the parent company, Astra International owns 59.5% of the company.

Similarly, China’s state-owned oil and gas giant CNPC owns over 80% of PetroChina – its listed subsidiary.

Second, as discussed in a recent Net Zero Investor article, Asia’s states are powerful asset owners in their own right. The region’s state-owned investment companies hold significant stakes in listed companies.

China’s SAIC Motor Corp, is simultaneously state-owned and publicly listed. Less than a quarter of its equity is outside state control.

Similarly, at India’s Oil and Natural Gas Corporation less than a third of equity is held by institutional investors. 58% of the company is owned by the state.

Exceptions

There are however, outliers. Even companies with more than 50% free float have found themselves in hot water –

In June 2023, Danish pension fund Akademiker Pension and Dutch pension fund APG co-filed a resolution at Toyota – the Japanese carmaker. The resolution targeted the company’s climate lobbying.

“After more than two years of intense investor engagement with Toyota, it has unfortunately not been possible to reach common ground with the company on its lobbying activities”, the asset owners said in a joint statement.

Indonesia’s Bumi Resources, Taiwan-based Formosa Petrochemical Corp and China’s Anhui Conch Cement Company are other examples.

Surely, correlation does not imply causation. However, the fact that firms who are less open to investors are also often climate laggards highlights the distinctive challenges to engagement in Asia and could be indicative of the effectiveness of stewardship on climate change in the region.