Merciless exodus: what do NZIA’s departures mean for decarbonising insurance liabilities?

Insurers have been leaving the Net Zero Asset Owners Alliance (NZIA) in droves. This raises concerns over the carbon footprint of their liabilities

2023 has been a difficult year for the Glasgow Financial Alliance for Net Zero (GFANZ), the coalition of financial institutions which formed during the COP 26 Climate conference in Glasgow to foster collaboration on climate change.

The group has become a target of the anti-ESG movement in the US, starting with several banks threatening to leave the network unless a ban on financing coal projects was dropped.

More recently, the Net Zero Insurance Alliance (NZIA) has been in the eye of the storm.

Having attracted a network of more than 20 global insurers since its inception, the NZIA has in recent months faced a series of departures, as a host of insurers, including Swiss Re, Munich Re, Tokio Marine Holdings and even its chair, AXA having left the alliance. As of mid-June, the network only lists 14 members on its site.

The U-turn on international collaboration around climate change raises concerns, not just about the knock in impacts for GFANZ more broadly, but also how it might affect efforts to decarbonise insurance liabilities.

Unlike other asset owners, like pension funds, whose carbon footprint is predominantly limited to the investment portfolio, insurers also have to consider the carbon footprint of their liabilities, for example in underwriting oil and gas projects.

While many insurers remain a member of the Net Zero Asset Owner Alliance (NZAOA), this coalition tends to focus on the carbon footprint of assets. In contrast, the NZIA is unique in that it imposed reporting obligations for assets as well as liabilities.

Legal threats

Primary driver for the prominent departures were legal threats by anti-ESG groups such as Consumers’ Research, who allege that the collaboration on climate change is anti-competitive and violates anti-trust laws.

These threats apply to insurers more so than to other financial institutions because in the US, insurers are regulated by the state, rather than by federal government explains Peter Bosshard, program director at the Sunrise Project and coordinator of the international Insure Our Future Campaign.

“This gives a handy leverage to those red states politicians who have now identified ESG as the latest topic in their culture wars and they can make life difficult for insurers."

“This gives a handy leverage to those red states politicians who have now identified ESG as the latest topic in their culture wars and they can make life difficult for insurers.”

But the anti-trust threats themselves do not have a lof of merit, according to Cynthia Hanawalt, a senior fellow at the Sabin Center for Climate Change Law at Columbia Law School.

“It's helpful in the antitrust context to think about categories of behaviour. What GFANZ is doing – information sharing, target setting - is not unusual: voluntary industry standard-setting and trade associations have long been permissible under U.S. antitrust laws,” Hanawalt said.

While Hanawalt sees reasons why collaboration between competitor firms might invite scrutiny, she is also confident that caselaw has sufficiently developed to distinguish between industry groups that have pro-competitive value, and where they cross the line into antitrust violations.

This view is seconded by Bosshard, who added that insurers would not have entered these networks without assessing the risks first.

“From the start, in-house legal departments have been really strict about avoiding anti-trust risks, particularly German insurers were extremely cautious about that, to the extent that NZIA does not put any obligations on its members to move away from fossil fuels.”

A cop out?

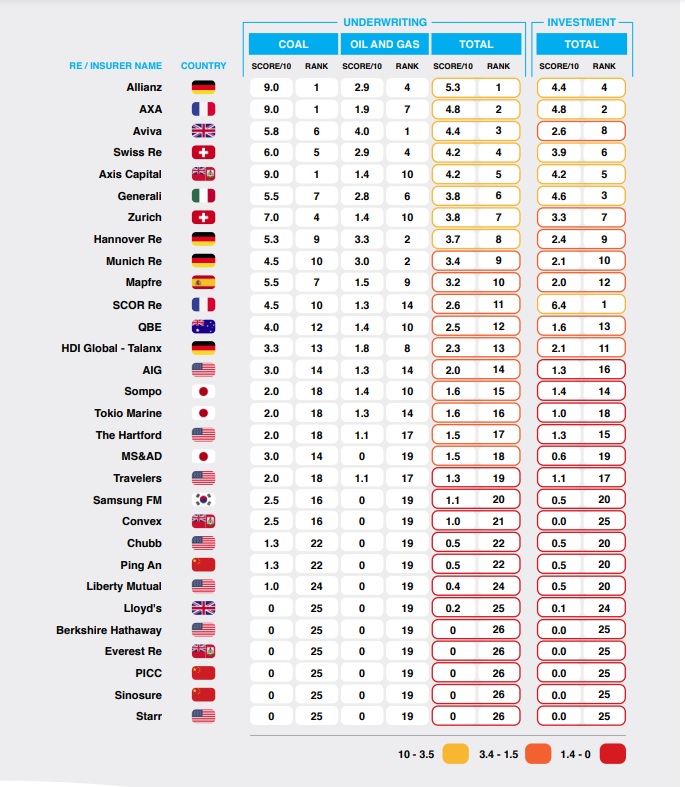

Does this mean that the departures are simply a cop out? Not quite, believes Bosshard. He highlights that many of the firms who have left have scored relatively well on Insure Our Future’s 2022 Scorecard, which assesses not just carbon exposure in investment portfolios, but also the underwriting of coal, oil and gas projects.

Nevertheless, exposure to the US was the primary driver for the departures believes Bosshard.

“It was no coincidence that almost all insurers who left had a big part of their revenue from the US firms like Allianz, Generali and Aviva no not have a big part of their revenue coming from the US and are still members but firms like Munich Re has more than 30% its revenue coming from the US and Swiss Re more than 40% and so for them it is a much bigger slice of their revenue” explained Bosshard.

“It's helpful in the antitrust context to think about categories of behaviour. What GFANZ is doing – information sharing, target setting - is not unusual:

Net Zero Investor has approached the insurers in question for a comment. Only Munich Re and Swiss Re opted to comment, with both firms stressing that the anti-trust threats were indeed the primary factor for their departures but that they will remain committed to their net zero targets.

Poor timing

But the timing of these departures should nevertheless raise eyebrows. The NZIA has adopted its first Target Setting Protocol in Davos earlier this year, which has established uniform reporting standards for carbon emission developed in collaboration with the Partnership for Carbon Accounting Financials (PCAF).

These standards provide insurers not just with a framework on how to measure and report greenhouse gas emissions, they also set specific decarbonisation targets. Insurers who are members of the NZIA would have been required to report on these targets from July this year on.

Net Zero Investor has reached out to the insurers who have left the alliance but so far, none have explicitly confirmed whether they will continue to uphold the NZIA targets, despite having left the alliance.

Departures from the alliance mean that there is now less peer pressure on insurers to reduce their underwriting activities for coal, oil and gas projects.

This is a concern that even GFANZ itself acknowledges: “These political attacks are now interfering with insurers’ independent efforts to price climate risk, which will harm policyholders, main street investors and local economies. Despite these political headwinds, we will continue to support insurers' efforts to manage climate risk and develop transition plans” a spokesperson for the network told Net Zero Investor.