Green hydrogen: still too niche for institutional investors?

While some asset owners are taking a pioneering first-mover approach, others struggle to find appropriate investment opportunities

Its proponents argue that green hydrogen is critical for decarbonising hard-to-abate sectors where alternative solutions are either unavailable or difficult to implement, but the gas still has a long way to go to fulfil this mission.

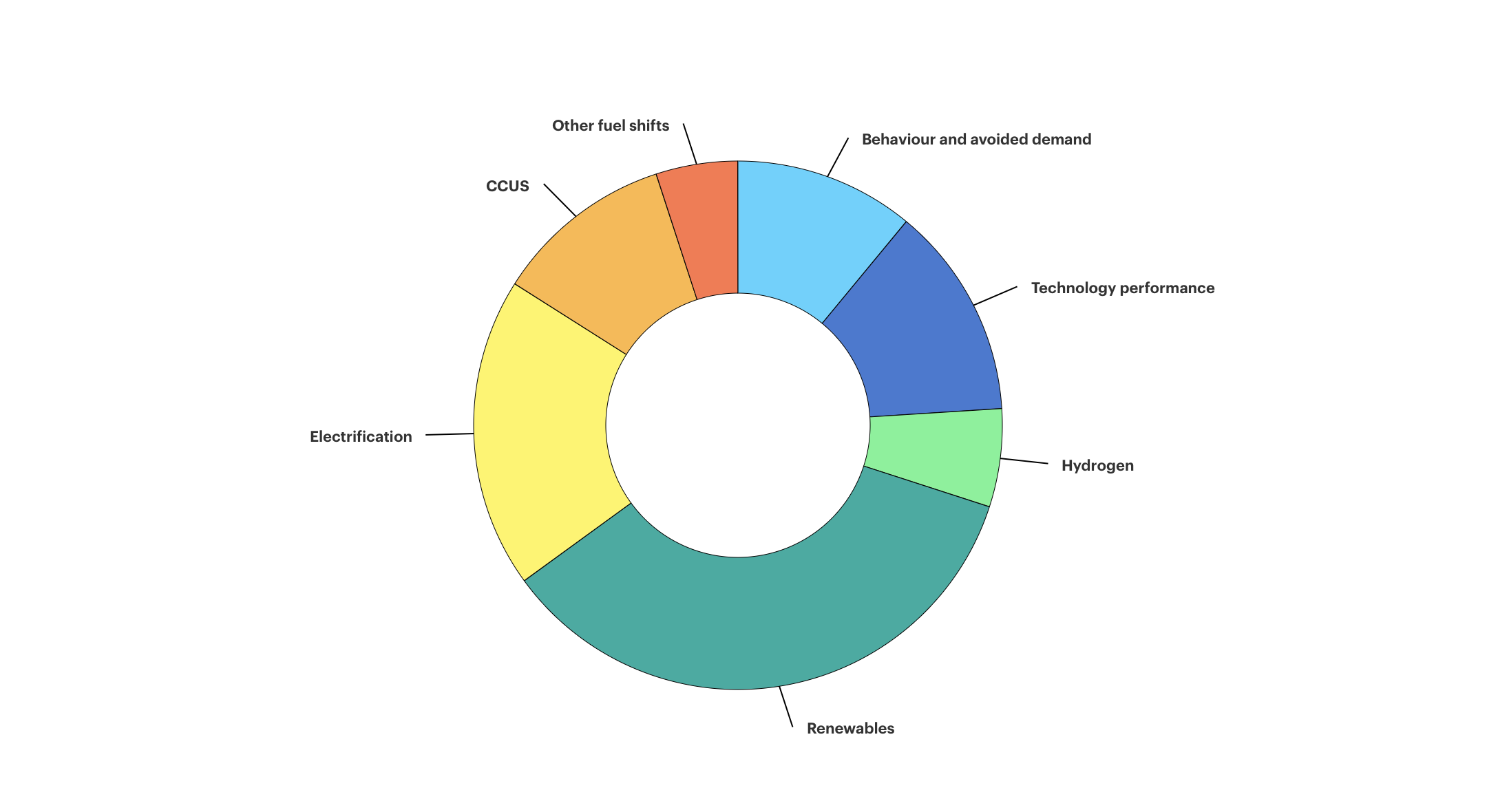

Novel applications in heavy industry and long-distance transport – the key hard-to-abate sectors earmarked for hydrogen - account for less than 0.1% of hydrogen demand, whereas they should account for one-third of global hydrogen demand by 2030 to reach net zero by 2050, according to the International Energy Agency.

From an asset owner’s perspective, green hydrogen is still a niche area, accounting for only a very small proportion of the overall amount of capital allocated to energy transition infrastructure, despite the high levels of media attention.

The main issue is that hydrogen often struggles with the “TECOP” risk assessment for investability. TECOP is a prompt list used in risk identification to examine the technical, environmental, commercial, operational, and political factors of a project.

One key technical risk is a lingering uncertainty around which of the many industrial processes used to produce green hydrogen will ultimately become the market leader.

In addition, the commercial viability of green hydrogen projects is still highly dependent on some form of government support in many cases.

That hasn’t stopped asset owners like Canada Pension Plan (CPP) from championing a first mover approach.

Green molecules

CPP has been looking at hydrogen opportunities for around three years now.

As hydrogen opportunities straddle different asset classes, CPP’s public markets team as well as its venture capital team have been examining different entry points across the value chain.

The fund recently unveiled an initial €130 million investment in the Dutch hydrogen project developer Power2X, acquiring a majority interest.

“The European market is quite interesting because of an ability to develop projects close to the customers,” said Bill Rogers, managing director of sustainable energies group at CPP Investments.

Power2X projects include ErasmoPower2X, a €1 billion solar and hydrogen plant, and MadoquaPower2X, a €1 billion industrial-scale hydrogen and green ammonia project.

Power2X aims to become a long-term developer, owner and operator of next-generation energy assets with a focus on green hydrogen and other clean molecules such as green methanol and ammonia.

The term “green molecules” refers to the application of green hydrogen and its derivatives, including green ammonia and green methanol, to decarbonize non-power, hard-to-abate industrial activities.

These green molecules can act as direct replacements for process feedstocks or transportation and heating fuels, the companies claim.

CPP has also acquired Pattern Energy, which is developing green hydrogen projects in Canada, and ReNew, which is based in India, where an abundance of cheap solar power and limited natural gas makes green hydrogen more cost competitive than other regions.

Schroders also advocates an early-mover approach.

"We believe there will be significant deployment into hydrogen-related assets over the medium to long-term, and this is essential to meeting net-zero targets," wrote Prabaljit Sarkar, Schroder's infrastructure Investment Director, in a recent blog.

Over time, "many more projects are expected to emerge" to match the risk profile that debt providers typically look for and become “bankable”. In the meantime, those who are willing to be flexible and seize the opportunities available today stand to benefit from early-mover advantage, Sarkar said. Opportunities in the emerging markets may provide the “leap frog” effect, reducing time to adoption and increasing overall positive impact.

UK asset owners explore hydrogen

In the UK, Wandsworth Pension Fund recently announced plans to invest up to £80m in two energy transition funds based on non-traditional renewable projects such as battery storage, green hydrogen and other carbon reduction investments.

The Border to Coast Pensions Partnership has invested €100m in the Clean Hydrogen Infra Fund as part of its plan to build a portfolio of investment opportunities that support global decarbonisation.

Managed by Hy24, the Clean Hydrogen Infra Fund focuses on investments across the clean hydrogen value chain, from production and conversion to storage, supply and usage.

The UK insurance giant Aviva is also exploring green hydrogen. "Renewables is a highly specialised marketplace so we have brought together the expertise to match," said Nick Major, MD, commercial lines, General Insurance at Aviva.

Greenwashing risk

While some car producers like Renault Group have embraced hydrogen, critics argue that hydrogen production still isn’t green and efforts should focus on using hydrogen only for sectors where alternatives aren’t available, in line with the International Energy Agency recommendations.

“We believe there’s a clear pathway for the large-scale deployment of green hydrogen in hard-to-abate sectors like shipping and heavy industry,” said Bill Rogers, managing director of sustainable energies group at Canada Pension Plan Investments. “It’s less clear whether hydrogen is the right solution for other sectors, such as light vehicle transportation.”

Critics have also noted significant greenwashing risks across multiple scenarios. For example, the promise of abundant green hydrogen in the future has given some European utilities a reason to push building power plants that would burn natural gas now but switch to green hydrogen later on.

If, for whatever reason, green hydrogen doesn’t become sufficiently abundant, then these power plants could simply keep on burning natural gas.

Another concern is inefficiency in the production and storage of green hydrogen, which could mean the gas doesn’t become cost effective enough to deploy at a large scale.

Public funding for the hydrogen sector totals $146 billion worldwide to 2030, according to BloombergNEF. Germany tops the list with $28.6 billion, while the UK has committed $1.9 billion.

Early Days

It is still early days for institutional investors considering the green hydrogen value chain.

“Some infrastructure managers have been looking at hydrogen projects within the context of their border infrastructure portfolios,” said Amarik Ubhi, Mercer’s global head of infrastructure. Given that these opportunities can straddle different risk/return profiles, both energy transition private equity managers and infrastructure managers are looking at opportunities.

Ubhi notes that some private markets managers have launched dedicated funds to focus on the hydrogen value chain. Such funds cover not only production, but also transportation, transmission, storage, and end usage.

“This is an area that institutional investors are starting to consider, if not actually allocate capital to meaningfully at this stage, as it remains one of the more niche, emerging areas of the broader energy transition theme,” he added.

Too niche for some

Green hydrogen is still too niche for pension funds like NEST, which tends to prefer to focus on proven technologies and other energy transition infrastructure investments, such as car charge points, than emerging technologies.

“Hydrogen is often seen as a kind of holy grail for certain aspects of the energy transition, but the infrastructure is going to take a long time to develop,” said Katherina Lindmeier, senior responsible investment manager at NEST.

In the meantime, investors faces “significant cost barrier to entry”, which is also true for other emerging technologies, such as small modular reactors for nuclear.

The International Energy Agency (IEA) notes that announcements for new projects for the production of low-emission hydrogen “keep growing”, but only 5% have taken firm investment decisions due to uncertainties around the “future evolution of demand, the lack of clarity about certification and regulation and the lack of infrastructure available to deliver hydrogen to end users”.

On the demand side, hydrogen demand keeps growing, but remains concentrated in traditional applications – not the hard-to-abate sectors where the use-case is clearest.

More policy support needed?

The IEA affirms that a growing number of countries are releasing national strategies and adopting concrete policies to support first movers. But the delays in the implementation of these policies and the lack of policies for demand creation are preventing the scale-up of low-emission hydrogen production and use.

To get on track with the net zero by 2050 scenario, the agency calls for accelerated policy action to create demand for low-emission hydrogen and unlock investment that can accelerate production scale-up and deployment of infrastructure.

As it stands, the US and the EU have taken the lead in policy action, while China is furthest ahead in deployment.

“We have seen incredible momentum behind low-emissions hydrogen projects in recent years, which could have an important role to play in energy-intensive sectors such as chemicals, refining and steel,” said IEA Executive Director Fatih Birol. “But a challenging economic environment will now test the resolve of hydrogen developers and policymakers to follow through on planned projects. Greater progress is needed on technology, regulation and demand creation to ensure low-emissions hydrogen can realise its full potential.”