Mining for Net Zero: Is a green commodities crisis around the corner?

Part II of NZI’s Mining for Net Zero series examines the implications of projected shortages in critical minerals needed for green technologies

A disconnect between short-term pricing cycles and long-term demand could result in a green commodities crisis in the next few years, investor and mining sources tell Net Zero Investor.

An inability to meet the increasing demand for critical minerals that are essential components of green technologies, such a crisis would be disastrous for the transition to net zero.

Unlike fossil fuel technologies, their renewable counterparts require far more critical metals and minerals.

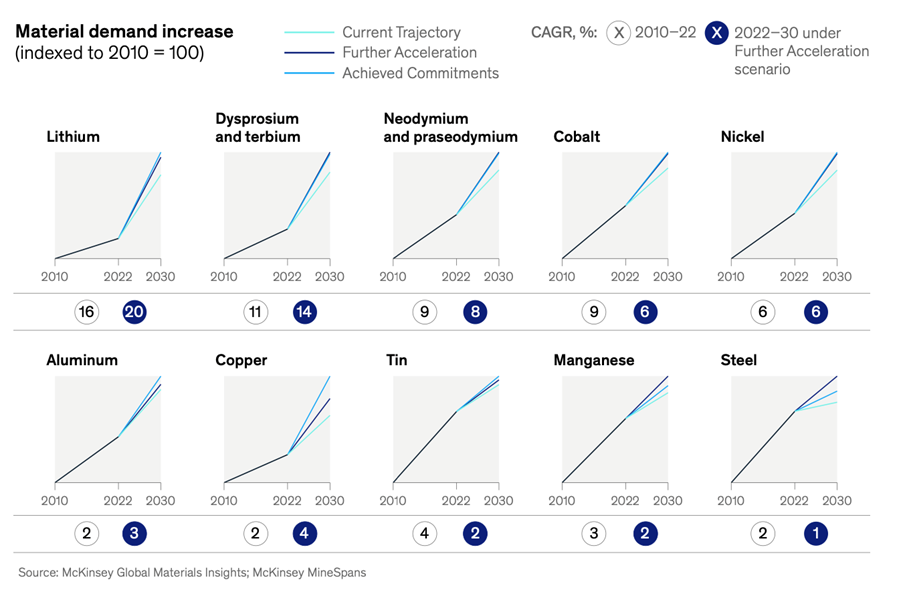

A recent McKinsey report found that even with the current decarbonization trajectory trending toward 2.4°Celsius, the supply of many minerals and metals embedded in key lower-carbon technologies will face a shortage by 2030. While some materials such as nickel may experience modest shortages (approximately 10 to 20%), others such as dysprosium, a magnetic material used in most electric motors, could see shortages of up to 70% of demand.

Short-term price cycle disconnect

Andrew Bailey, CEO of MinEx CRC, the world’s largest mineral exploration collaboration, says, “The problem is that the projected long-term shortage of critical minerals is not adequately reflected in the short-term commodity-price cycle. For example, everyone knows that there will be a global shortage of copper fairly soon. Still, counterintuitively, copper prices are currently dropping due to the short-term impact of China’s slowdown. And when prices drop, there’s less incentive to invest, despite the known long-term demand.”

Given that it takes an average of 14 years to get critical minerals from exploration to supply chain, it could be too late to ease the pressure by the time the shortage hits. Supply constraints would make green technologies harder to build and scale to the extent needed for the transition.

Bailey adds, “These minerals will be critical, but they're just not critical yet; that’s the conundrum.”

Iron ore, which is essential for building wind turbines, is still only 70% of its price a year and half ago, according to Bailey.

It is also worth noting that discovery is a high-risk game for miners, as around only one in a thousand exploration prospects become mines. Often it takes the push of the short-term commodity price cycle to catalyse action.

That said, the disconnect isn’t total, according to Bailey. The short-term lithium price, for example, has taken off, stimulating interest and investment and, as a consequence, supply. However, lithium processing plants are expensive and take a long time to build. So even with lithium, there’s still a significant lag in the system.

Net zero under threat

Adam Mathews, chair of the Global Investor Commission on Mining 2030 and chief responsible investment officer at Church of England Pensions Board, says the whole net-zero transition is “under threat if we don’t ensure mining is able to meet demand”. Even with optimal levels of efficiency, substitution, and recycling, a huge growth is required across the whole sector. Like Wilson, he also stressed the problems caused by the enormous delay, usually around 14 years, between expanding or opening a new mine and actual production.

"We need to completely rethink the way we look at the sector, and, above all, have the confidence to invest in it at the scale needed to meet demand both in the present and the future.”

Similarly, the McKinsey report suggests that unless mitigation actions are put in place, shortages would hinder the global speed of decarbonization because customers would be unable to shift to lower-carbon alternatives. Moreover, these shortages would lead to price spikes and volatility across materials, which in turn would make the technologies in which they are embedded more expensive and further slow adoption rates.

Additionally, many mines that need to be expanded are in areas that are home to indigenous communities.

Mathews adds, “As investors, we need to understand the demand, the issues it will cause, and the interventions needed to ensure that the sector can grow in a responsible way, with positive impact on local communities, and minimal negative impact on the environment.”

Growing awareness not translating into action

Organisations such as the international Energy Agency (IEA) emphasising critical minerals, a case in point is the IEA's Critical Minerals and Clean Energy Summit due to take place in Paris in September.

With even some electric car manufacturers setting up their own mining operations, Matthews notes a growing awareness among G7 nations of the importance of securing supply chains for the transition.

“At least part of that awareness is a scramble to respond to China, which has long since recognised the importance of these minerals and effectively cornered the market,” he says.

However, growing awareness has yet to translate into, say, a better valuation of mining companies or the way investors allocate capital. “Our portfolio actually has a fairly minimal exposure to mining as a proportion of the fund. We need to completely rethink the way we look at the sector, and, above all, have the confidence to invest in it at the scale needed to meet demand both in the present and the future.”

Asset owners are still “treating the sector as they always have, rather than elevating it to a more strategically important field”.

Nor will circular economy principles be enough to ease shortages. Matthews says, “However much we recycle – and we need to do everything we can to rapidly scale recycling and reuse – it will not get us out of the coming supply crunch.”

State invention

When market dynamics fail to deliver, policy interventions tend to be the answer. However, Western governments have been slow to the green commodities table, Bailey laments.

He says, “Between 60 and 90% of most critical green minerals still come from China. If the flow of minerals out of China stops, that would be really disastrous, so more work needs to be done to safeguard their supply from other sources.”

Commodities like lithium are actually relatively widespread, meaning if governments start looking for them, they can find them, though it's still “a really long process from discovery to supply chain, even when it's fast tracked”.

__________________________________________________________________________________________________________________________________________

Also read

Mining for Net Zero: why investors need to engage more with miners

__________________________________________________________________________________________________________________________________________

While Western governments are starting to wake up to the need to support the green transition, as demonstrated by game-changing stimulus packages like the US’s Inflation Reduction Act, in the mining space, such interventions can be more focused on onshoring processing plants than discovery or extraction, Bailey says.

“After many years of inaction, a large number of governments, particularly in the G7, are now trying to identify mineral sources,” says Matthews. “A minerals race is starting to happen at the state level. However, it is very late in the day. This has been a massive blind spot.”

For example, G7 countries have committed to a Five-Point Plan for Critical Minerals Security, supported by the IEA.

Race to the bottom

Responsible sourcing is easier when supply is plentiful, but when shortages occur, states and other actors may be willing to make ethical compromises to secure supply.

The energy crisis triggered by the Ukraine war clearly demonstrates the extent to which states look to revert to problematic practices, such as coal-fired power stations, when demand outstrips supply. Indeed, coal was one of the most sought after commodities in 2022.

For a sector as sensitive as mining, such a dynamic could have devastating impact on human rights and the environment.

“Getting greater transparency of emissions intensity for critical green minerals is important,” says Rob Wilson, executive director of resources at Australia’s Clean Energy Finance Corporation (CEFC). “There are some instances where you see less environmentally friendly product coming into the market around the world, and when supply chains get constrained, customers take whatever they can get.