BERS’ investment lead: ‘climate change is an un-diversifiable risk’

Antonio Rodriguez leads the investment office about NYC BERS. He sat down with Net Zero Investor to discuss divestment, diversification and the anti-ESG pushback

Climate change has been high up on the agenda for the five New York City Public Pension Funds. Collectively, they manage more than $250 billion on behalf of the City’s 750,000 public servants through the Office of the New York City Comptroller.

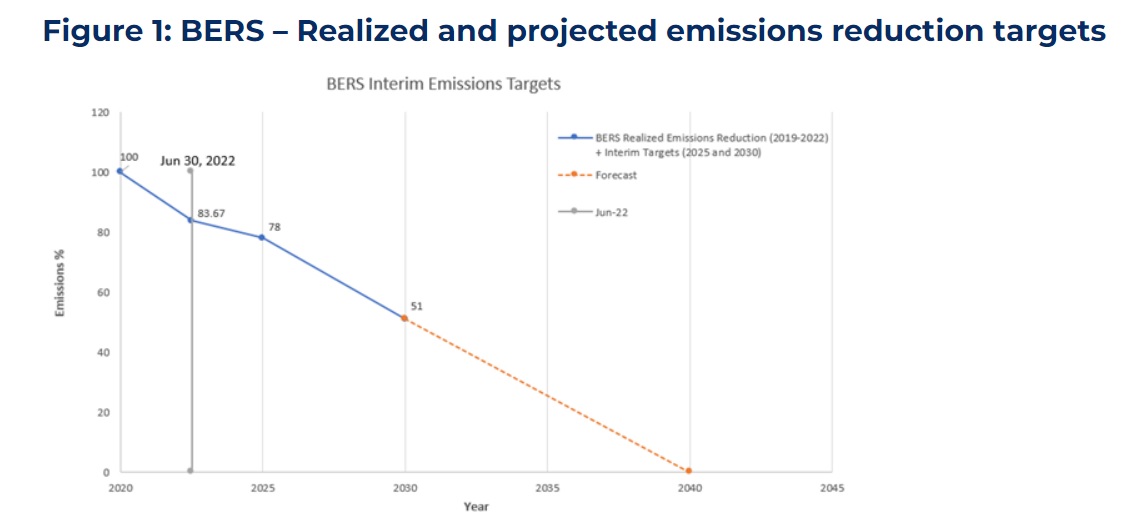

Earlier this year, three of the City’s funds, Teachers, NYCERS, and BERS – announced their Net Zero Implementation Plans, aimed at their net zero by 2040 targets into practice.

The three funds went beyond engagement and opted to divest from some of their most carbon-heavy assets.

A decision which brought them into hot water with four of their own members who, in May this year, with the backing of anti-union campaign group Americans for Fair Treatment took them to court for an alleged breach of their fiduciary duties.

New York City Comptroller Brad Lander described it as “a weak attempt by anti-ESG, anti-union forces to undermine the decisions by our pension system trustees to assess the very real risks of climate change to their portfolios.” But will it affect the System’s approach to tackling climate change in their investment portfolios?

Net Zero Investor caught up with Antonio Rodriguez, director of Investment Strategy at the $9 billion New York City Board of Education Retirement System (BERS). Rodriguez has been instrumental in setting up BERS' investment office and led its first independent manager selections process.

While he declined to comment on the ongoing case, he argues that broader anti-ESG pressures will not prevent the implementation of the fund's 2040 target.

Can you tell us a bit more about your approach to stewardship?

New York City has a fantastic stewardship programme through the Office of the Comptroller. Their office of corporate governance, led by Mike Garland, Yumi Narita, and John Adler are some of the best in the business.

We have a proxy committee that meets twice a year, establishes the goals for corporate governance and proxy voting. Our board of trustees and the executive committee oversee those broad guidelines and the office of corporate governance are the ones who are suggesting priorities, point out successes from prior engagement and where we want to go next year.

This is run almost entirely separately from the asset allocation and portfolio construction side of the fund. I do believe we could do a better job of aligning them sometimes.

But overall, the best aspect of the centralised New York City process is that you have the strength of five systems working together to improve corporate governance.

Does that mean that that the systems always must have similar positions?

No, each of the five systems have their own guidelines and responsible investment principles. If I characterise BERS, we probably sit in the middle when it comes to things like corporate governance and climate solutions. We are progressive but also tend to be comfortable with market terms.

In some ways it is the best of both worlds, you can have your customisation and your viewpoints reflected in the implementation whilst also having the strength of systems working together.

How does this then affect your stance on climate change? You have recently divested from some fossil fuel companies?

Yes, we have divested from certain fossil fuel reserve owners in 2021. This decision is really concentrated on exploration production companies. But engagement is still the major focus for our system.

The New York City funds are part of CA100+, we will follow the lead of other larger asset owners for engagement there and support their resolutions. One of our recent focus areas is also engagement with utilities.

But it has brought you in the firing line with the anti ESG movement. Does this limit your ability to act on climate change?

We talk to our counterparts across the country. But there are headlines and then there is what is going on day-to-day.

The headlines often do not reflect the reality of how investors and companies are thinking. I don’t see the impact of the pullback on engagement on these issues in practice. Do they call them ESG? Or something else? If it’s the nomenclature that gets you into trouble, perhaps just do the work.

So stewardship on climate change could just be branded as good fiduciary practice or risk management?

Exactly, and without the headaches. For example, our real estate managers, regardless of whether they call something ESG or not, want to save on energy cost. You don’t want to be backing down but you also don’t need to make things more difficult for yourself.

How big of an impact has the decision to divest left on your overall portfolio?

Not very big, they accounted for less than one percent of our portfolio.

Has this been a bit of a storm in a teacup?

It is. While these divestments are bigger than some in order of magnitude, I don’t think there is any problem in building a well-diversified portfolio without these names.

But you do now have less exposure to the energy sector in your portfolio. Does this also mean losing out on short term profits?

Yes of course, this is like any other active management decision. The bigger picture is that there has been a rigorous amount of study behind this decision.

Can you give some examples of your engagement efforts in utilities?

Yes, Southern Energy and Duke Energy are the two companies where the systems have done a lot of engagement on reducing the carbon footprint and diversify their energy mix away from natural gas.

And how does this then tie into your net zero by 2040 target?

We passed this target alongside two of our other sister systems, right now this is in alignment with the Office of the Comptroller.

Because we are externally managed, we will reduce our carbon footprint more through the manager selection process rather than through security selection process.

In the beginning, it can be about something as simple as establishing if our managers have science-based targets and how they integrate it into their processes.

I am more on the asset allocation and portfolio construction side, so I would then think, what does this mean for our value managers for example? How do we construct portfolios without being completely and utterly overweight tech, which we already are. And how do you align a net zero target with a very successful corporate engagement strategy and create portfolios that don’t have massive active tilts?

Or, if climate is going to be our tilt, does that mean that our entire risk budget is spent?

We have all accepted this is the direction we need to go, but how do you fit the parameters into the risk budget that you are allowed? That is going to be interesting conversation for plans like ours over the next decade.

"If it’s the nomenclature that gets you into trouble, perhaps just do the work"

Is this increased risk coming from being overly concentrated in tech stocks? What are the other risk factors that are increasing?

For instance, we had to divest from some assets. And to the degree that climate solutions are part of any asset allocation, those opportunities are disproportionately in private markets.

In the context of my underlying liabilities and cashflow considerations as a pension fund, that is a multi-variant risk problem.

The next question is, how do you build a climate change-resilient portfolio? This is going to affect beta’s all over the place. And I don’t think you can build a climate change resilient portfolio, that is an oxymoron.

90% of our folks live in New York City, what does climate change mean for them in their retired years? We have to try to build a portfolio that allows more space for solutions, engagement and investment in new technologies. I can’t overload in any one area. I can’t overload in private markets when I need cash over the next ten years.

These are two separate things you mentioned, investing in climate solutions, but these solutions might still be exposed to climate risks.

A 100%. But I believe climate change is an un-diversifiable risk. I can be underweight oil and gas all I want but when the affected universe is literally the globe then there’s nowhere to hide. It shifts the entire curve of returns, rather than just your place on the curve.

But when we discuss climate change, risk to the portfolio will most likely pale in comparison to risks to our members and sponsors. Portfolio risk can be managed if not necessarily mitigated.

You show me a plan that is still getting cash in, and I’ll show you a plan that has a fighting chance. But the portfolio risk can be managed once I know how much I want paid out, then we can work on that.

We also need to think about what happens to our sponsor. Money going into our pension fund is money that can’t be spent on building to be climate resilient and money that is spent [on climate resilience is money that isn’t going into our fund. I am less concerned about the portfolio risk and more about the risks to our plan, these two are not necessarily the same thing.

The City needs to be able to fight a number of different fires at the same time.