Stranded assets: The trillion-dollar decommissioning challenge

The cost of decommissioning stranded assets could be as high as $8 trillion across conventional and renewable energy sources, new research suggests

With the energy transition now well underway and inflows into renewable assets growing, investors are facing a new challenge: What happens if these assets have reached the end of their life cycle? The cost of decommissioning stranded assets could be as high as $8 trillion across conventional and renewable energy sources, new research suggests.

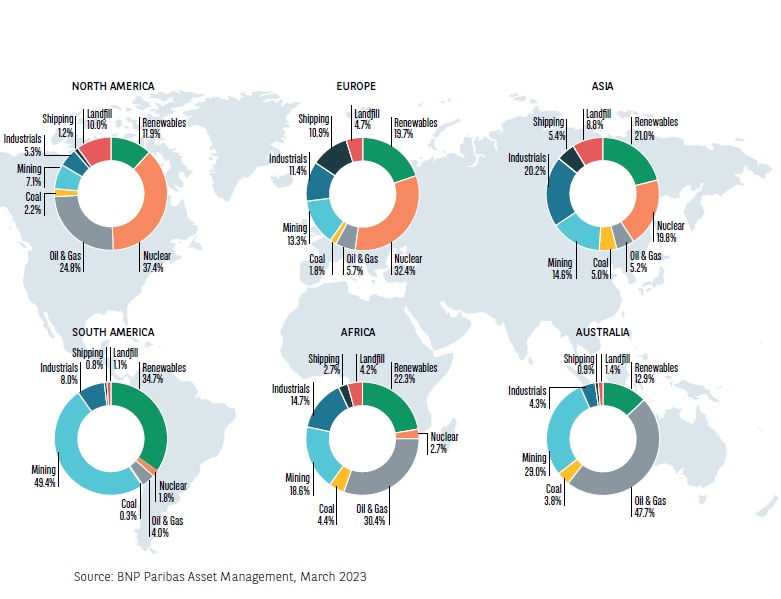

The estimated cost of decommissioning assets in the energy sector had risen dramatically over the past three years with the Asian continent bearing half of the total financial burden globally, according to a recent report by BNP Paribas.

In 2020, the French asset manager estimated that the total cost of decommissioning stranded assets in the energy sector could hit $3.6 trillion. However, factoring in the decommissioning costs for the renewable energy, shipping, industrials and landfills sectors, this figure has now risen to $8 trillion, the report warns.

Renewables impact

Asia is by far the most exposed, it could end up footing a bill of more than $3.8 trillion, almost half of all total decommissioning costs. This is in part due to its larger exposure to the mining and industrials sectors which account for $555 billion and $769 billion respectively. But the cost of responsively disposing of renewable energy infrastructure accounts for $799 billion, making it the costliest sector to decommission, the research reveals.

The distribution of decommissioning costs varies significantly by continent. While Europe and North America face the largest risk in decommissioning nuclear energy infrastructure, Africa and Australia will be hardest hit in the oil and gas sector and South America in mining.

Globally, disposing of nuclear energy infrastructure remains the priciest sector, it accounts on average for almost a quarter of all costs. But the second most expensive sector to decommission going forward will be renewable energy, which accounts for more than 19% of all costs globally.

The BNP Paribas research also reveals that there is still a significant amount of uncertainty embedded in estimating the cost of discarding of energy infrastructure. In Germany, where the government has pledged to phase out nuclear energy, the cost of decommissioning nuclear infrastructure is set at $1.4 billion per gigawatt of generating capacity. The UK handles an even more conservative estimate of $2.7 billion, while France, where nuclear remains a key source of power, has budgeted for only $300 million per gigawatt.

Balance sheet blind spots

For investors, a key challenge is that these costs of stranded assets are currently not accurately priced in. Share prices of the world’s largest oil and gas firms have been rising, but estimates of the costs of decommissioning stranded assets vary greatly. What is more, few companies have taken action to pre-fund decommissioning risks.

Another way of looking at this is to assess whether the assets that are currently on energy companies’ balance sheets are likely to generate sufficient revenues to fully cover the capital invested. This estimate is not only based on today’s prices for energy assets, but also factors in forecasts for future valuations, as an article series produced by Carbon Tracker earlier this year points out.

Effectively being asked to mark their own homework, energy companies have been extremely optimistic in budgeting for the retirement costs of oil wells. By planning to retire them in 50 to 70 years, they have pushed down the estimated costs of retiring these wells, the energy market's equivalent of a pensioner taking out a 50 year mortgage.

But these plans do not align with the aims to keep global temperatures well below 1.5 degrees, as Carbon Tracker’s founder Mark Campanale points out: “There’s going to be an awful lot of oil refinery capacity the world doesn’t need in a 1.5 degrees world, that’s going to have to be written down. We’re not seeing the discussion we’d expect to see by companies as an audit risk item” he warns.

Campanale also points out that the world economy has a carbon budget of about 300 gigatonnes left before crossing the 1.5 degree target, but there are currently about 3,600 gigatons of CO2 in the world’s known coal, oil and gas reserves alone, almost a third of which is held by publicly traded energy firms. In other words, the world’s existing fossil infrastructure already exceeds the world’s carbon limits more than tenfold, without factoring in the potential impact of new oil and gas developments.

“There’s going to be an awful lot of oil refinery capacity the world doesn’t need in a 1.5 degrees world, that’s going to have to be written down. We’re not seeing the discussion we’d expect to see by companies as an audit risk item”

This also chimes with the latest Net Zero Roadmap released this week by the International Energy Agency which predicts that fossil fuel demand will drop by 80% by 2050. Consequently “no new long-lead-time upstream oil and gas projects are needed. Neither are new coal mines, mine extensions or new unabated coal plants” the IEA stresses.

For institutional investors, both the lack of clarity on the potential costs of decommissioning stranded assets and corporations reluctance to price these represent material portfolio risks, not just to listed energy firms in their portfolio. Carbon Tracker estimated in 2020 that there were about $30 trillion of fixed assets in the fossil fuel system with repricing having potential knock on effects on at least a quarter of global equity markets.

Moreover, the physical effects of rising global temperatures could also hit infrastructure and real estate valuations, with investors at risk of losing more than 50% of their unlisted infrastructure portfolio due to extreme weather events, according to a new study by EDHEC business school.

Planning ahead

But BNP Paribas’ latest research also outlines some options for corporations to improve the financing of decommissioning energy assets. And with renewable energy accounting for the second most expensive ticket to decommission, it becomes clear that the decommissioning challenge does not end in a net zero world.

Companies could pre-fund decommissioning costs through on a “pay as you go basis”, an approach that to some extent applied at some oil, gas and nuclear firms. Other options are a transfer of liability through divestment or pre-funding decommissioning reserves. Finally, energy companies could also aim to transfer the risk to insurance providers. However, the case of the coal industry illustrates that some assets may end up becoming effectively uninsurable.

BNP Paribas argues that energy companies could learn from the insurance and pensions industry, where liabilities tend to be matched, either through an (LDI) portfolio of government bonds, repos and swaps or by putting a cashflow driven investment (CDI) approach in place. Among these options, BNP Paribas advocates the use of a portfolio of private market investments in combination with fixed income assets to match long-term liabilities, much like cash flow driven investments pursued by the pension industry.

The jury is out whether the energy industry will take this advice on board. But given the scale of the decommissioning challenge, institutional investors may want to take a closer look whether the companies they invest in have put realistic risk modelling scenarios in place.