Who are the silent majority?

Who are the investors opposing more ambitious climate targets for the world's biggest emitters?

Stewardship on climate change has reached a stalemate, with support for activist net zero targets waning. While an outspoken minority of activist investors still campaigns for Paris alignment, a silent majority of shareholders is backing the U-turn on climate change among the world’s biggest carbon emitters. In this first instalment of a four-part series, we unearth the key actors representing this silent majority.

Scaling back on ambitions

When Colin Baines, stewardship manager at the £58 billion LGPS pool Border to Coast teamed up with a group of his pension fund peers to meet BP and discuss their energy transition plans, he soon sensed that someone important was missing at the table.

The British oil and gas giant had just presented its investors with a major reversal of its climate targets. Having set out relatively ambitious targets just three years ago, the surge in energy prices has sparked a scaling back of ambitions.

Baines says that BP’s plan has been abandoned with “with seemingly no consultation from shareholders at all.”

The speed of this turnaround is puzzling for Baines. “Only last year, they released their climate transition plan and within just six months, they jettison it, after getting an overwhelming shareholder mandate” he criticises.

When he and his peers sat down with BP executives, they were being told that BP had engaged with other investors who supported the firm’s change of heart, but BP did not disclose the names of these supporters nor provide evidence.

There is a problem with absenteeism, shareholders simply voting with management by default without giving it a second thought, that is one of the major challenges we are facing, to get them to be active

Reimagining energy

In 2020, BP CEO Bernard Looney announced the firm’s “new purpose of reimagining energy for the people and the planet.”

In practice, this meant the establishment of clear 2050 net zero targets for BP’s oil and gas operations, a 50% cut in the carbon intensity of its products. The firm also pledged to cut its hydrocarbon output by 40% by the end of the decade and increase the share of investments in renewables compared to investments fossil fuel extraction. These measures would have put BP ahead of its peers globally in their net zero ambitions.

But three years on, the group presented investors with a change of plans. Hydrocarbon output targets had now been reduced to 25%, rather than 40% and the group continues to invest a similar amount in fossil fuel.

The U-turn appears to have paid off. When BP announced its climate ambitions in 2020, its share price plunged from 495 GBX to 254 GBX year on year. But when the firm then revealed the scaling back of its net zero targets earlier this year, the share price surged above the 500 GBX mark again, a trend which was also influenced by a record £23 billion in profits in 2023.

A similar pattern can be observed at Shell, which also backtracked on its climate ambitions. In 2020, the firm’s share price plunged from 2,256 GBX to 1,297 GBX, it has now recovered to 2020 levels as the Anglo-Dutch oil giant scaled back on its climate targets.

In contrast, share prices at US-listed oil and gas firms that did not launch similarly ambitious pledges have been rising steadily over the same period. For example, Exxon Mobil’s share price has risen by more than 23% since 2020 and Chevron’s valuations grew by more than 70%.

Baines never did get to meet the anonymous backers of BP’s U-turn, but both the share price trends and voting patterns speak for themselves. Support for climate activist resolutions at BP has dropped to 16% this year, from more than 20% in earlier filings.

He believes that the lack of progress is due to investor absenteeism, rather than outright sabotage. “There is a large group that are absent and that is a real problem because management take that as tacit support. There is a problem with absenteeism, shareholders simply voting with management by default without giving it a second thought, that is one of the major challenges we are facing, to get them to be active”, he argued.

The key players

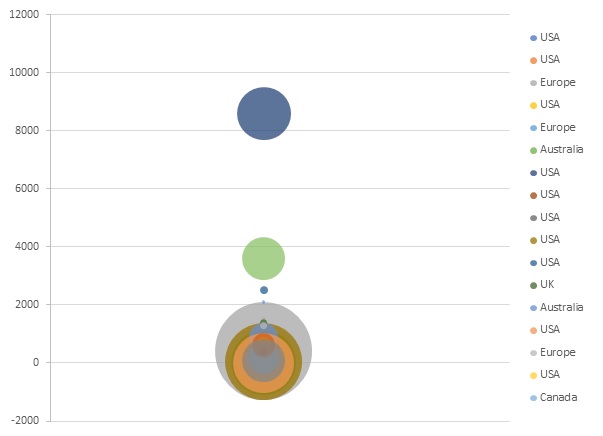

Net Zero Investor dug deeper into this allegation by focussing on the ownership patterns of listed companies in the Climate Action 100+ focus list, a group of 171 companies that have been identified as being key to driving the climate transition.

While these companies tend to have quite diversified ownership structures, public listing disclosures reveal that a handful of the world’s largest asset managers soon emerged as the largest shareholders in these firms. Most of the players fall between $500 million and $2 trillion in assets under management. We also have key outliers with over $4 trillion assets under management – these include but are not limited to the big three (Chart 1).

As is to be expected, given the size of the US market, these tend to be predominantly US based firms with the big three asset managers, BlackRock, State Street and Vanguard dominating the picture. This is largely due to their size, given that they hold more than $10 trillion in assets under management and collectively own more than 40% of the US fund market, according to Morningstar.

But tracing down detailed ownership patterns is complicated because investments are often placed through different subsidiaries. For example, BlackRock owns Australian mining giant BHP through BlackRock Investment Management and BlackRock Advisors (UK).

While American firms represent an overwhelming majority of asset managers by AUM, other managers include UK and Europe-based firms. Smaller managers include Singapore (Tamasek Holdings) and South Africa (Coronation Asset Management). This reflects the economic clout of capital exporting countries in stewardship and engagement.

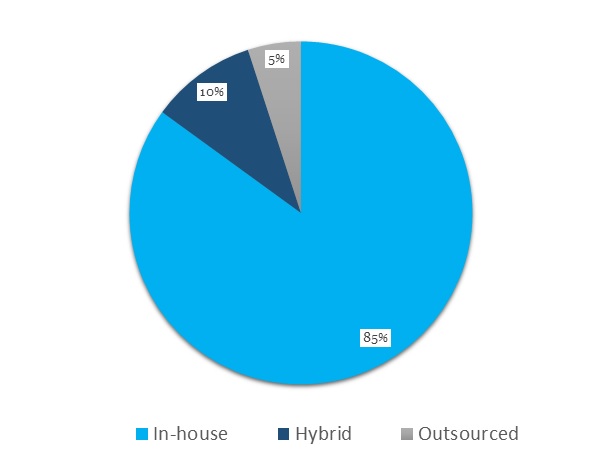

The majority of these managers, some 85%, are executing their stewardship and voting functions in-house, 10% pursue a hybrid model and only 5% have fully outsourced their stewardship efforts (Chart 2).

Bigger and better?

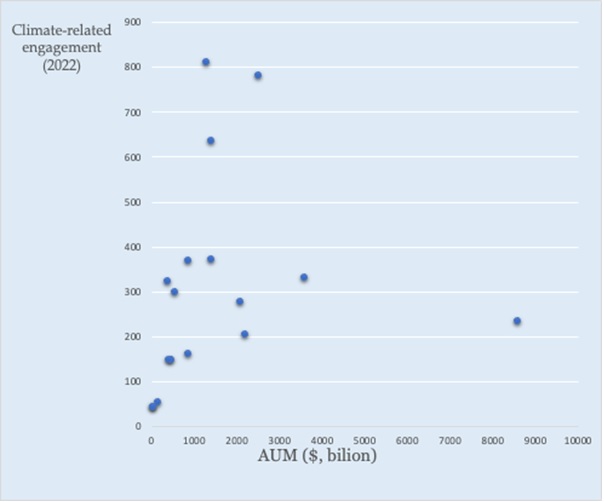

But despite having in-house capacity, when it comes to stewardship, bigger is not always better. Data extracted from the 2022 responsible investment and stewardship reports reveals that the size of asset management firms does not necessarily correlate with their levels of engagement.

On the contrary, more than 800 climate related engagements were conducted by investors with less than $2 trillion in assets (chart 4). One example is Norges Bank, which has $1.3 trillion in assets under management and executed 810 climate related engagements, from backing resolutions to communication with the firm’s management.

That is three times the engagement activity of BlackRock, which has $8.5 trillion in assets under management and cast just 234 votes that signalled concern regarding a company’s climate risk management during the 2022 proxy season. BlackRock says that its non-voting-based engagement was larger.

Smaller players also engaged last year – LionTrust Asset Management has approximately $31 billion in assets but engaged with 44 companies (Chart 3).

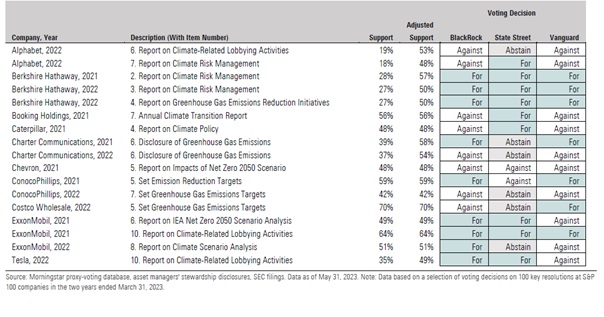

Still, even among the big three, there are significant differences when it comes to engagement, as research by Morningstar reveals. BlackRock and State State Street tend to be much more likely to back ESG resolutions, the firms backed 55% and 60% of ESG resolutions last year, while Vanguard backed less than a third, 28% of proposals.

A more detailed look among voting patterns for the big three reveals that they tend to be much more likely to accept reports on climate related lobbying activities than backing the introduction of hard and fast targets, as Morningstar research reveals (chart 5).

Asset managers backing down?

One trend that might warrant a closer investigation is the fact that asset managers also appear to have performed a U-turn on climate change. The Follow This Resolution on climate targets has been put forward consistently since 2016. In 2021, BlackRock did back the resolution, in 2023 it didn’t. A similar pattern can be observed among some of the UK’s biggest asset managers, including LGIM, abrdn, Schroders and Aviva.

BlackRock said in its latest Investment Stewardship Report that “measuring the quality of stewardship by the number of votes for or against management is an oversimplification of the issues that investors must contemplate. For one, it fails to acknowledge the progress that many companies are making year-on-year. It also misses other factors like the nature, quality and number of shareholder proposals that come to a vote every year.”

The investment giant also highlighted that 2022 saw a “marked increase in the number of shareholder proposals on environmental and social issues. Many of these did not address a material business risk for the company or were overly prescriptive.”

This suggests that the bone of contention here appears to be the establishment of more ambitious interim targets.

But the ambition of the Follow This Resolutions has not changed dramatically over the years. While the 2021 Follow This Resolution at the Shell AGM suggested that absolute emissions should be reduced “substantially" by 2030. The 2023 Follow This Resolution instead calls for “large scale absolute emission reductions.”

Crucially, the 2023 resolution took place against the context of the world’s oil and gas sector having made “almost no progress towards the Paris Agreement goals since 2021” according to the CDP Oil and Gas Benchmark report.

With the clock to 2030 ticking, while the targets of shareholder resolutions for the biggest emitters may not have been dramatically altered, their share price has certainly changed.

This article is part of a series. In the next instalment Net Zero Investor will zoom in on the stewardship practices at the world’s biggest investors in fossil fuels.