COP28: could investors be hit by a sudden phaseout of fossil fuel subsidies?

Ahead of COP28, Net Zero Investor takes a closer look at the distribution of subsidies across the globe. To reach global climate change targets a scale back of subsidies is essential. But could this impact the investment case for these assets?

Government backing for oil, coal and gas industries has been an integral part of the energy market from day one, as we explored in our latest feature on the history of fossil fuel subsidies. But could a scale back in subsidies come back to bite investors?

Distribution of subsidies

Despite climate pledges, 2022 was a record year for fossil fuel subsidies. Driven by the war in Ukraine and a global push for energy security, countries across the globe handed out a record $7trillion in subsidies to the oil, gas and coal industry, according to IMF figures.

In the same year, investors saw a steep rise in the profits of oil and gas firms, driven by a combination of rising commodity prices and government backing.

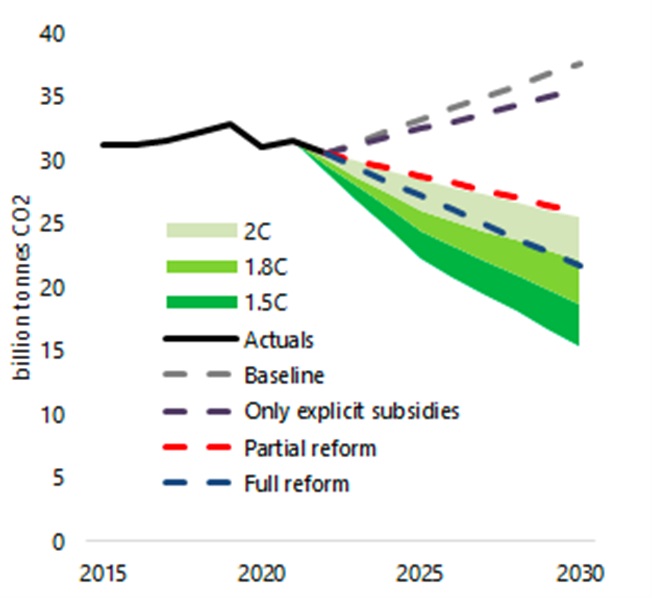

Moreover, the IMF predicts that fossil fuel subsidies are likely to rise until at least 2030. The IMF also warns that subsidies result in inefficient capital allocation, they impose a significant fiscal cost and most importantly they can distort economy-wide incentives to decarbonize.

To meet their climate targets, countries will have to drastically scale back their fossil fuel output. Ahead of the 28th COP summit, a key question for investors will be whether we could see a reversal of government subsidies among the nations with the highest levels of government backing.

In absolute terms, China is by far the largest subsidiser of fossil fuels, having handed out more than $2.2 trillion in government support in 2022. It also derives more than half of its energy supply from coal.

It is closely followed by the US, which spent around $150bn on subsidising the coal industry in 2022. Similarly, Russia spends nearly a quarter of its GPD on backing its fossil fuel industries.

Hedging their bets?

Over the past few years, with interest rates having been low major economies such as the US and China appeared to be hedging their bets by providing significant subsidies to both fossil fuel industries and renewables. But the IMF warns that this might provide a costly disincentive to invest in renewables.

Folland warns that they might be shooting themselves in the foot: “From the outside, it looks like they are hedging their bets or having their cake and eat it. But it is sending really confusing signals to investors. What they would need to see are much clearer signals that the governments are getting behind the transition, that is where the money needs to go as well.

What investors needed above all was clarity, he adds: “Investors need a clear commitment from governments that they will phase out fossil fuels by a set date will send an important signal to investors that they are serious about moving from high to low carbon economies” he warns.

In contrast, Tan Huck Khim, head of alternatives at Fullerton argues that the effectiveness of this two-pronged approach should be understood in the context of the level of economic development of individual countries.

Asia’s energy needs are still growing and coal happens to be one of the cheapest options for countries like China and India and Indonesia, the bulk of whose energy still comes from these sources. Acknowledging that this was a contentious topic, he cautions against finding once size fits all solutions: “You still need to meet the gap in terms of funding for energy. Asia still requires quite a bit of energy. Unlike Europe, most of Asia’s coal fired power plants are still fairly new. You're looking at an average age of five to 10 years for most of Asia, compared to, say, 30/40 years for coal fired power plants in Europe. “

Given this structure, it is going to be very difficult to transition away from coal. This is why the MDBs efforts on blended finance for the energy transition is going to be very important” he explains.

Outlook for COP28

With COP28 taking place in the United Arab Emirates, the eight largest producer of fossil fuels, observers have been sceptical whether progress on scaling back state support for polluters could be reached.

Not only had the last COP Summit in Sharm el Sheikh ended up on a pessimistic note, with countries failing to agree on scaling back fossil fuels, many countries, including Russia, the US, China, India, Brazil, Norway the UK and Nigeria have since scaled up on new oil and gas production.

But there are some indications of a change of heart on fossil fuels, the EU could be leading the charge. The European Parliament’s environmental committee approved a resolution at the beginning of November which calls for a phase out of all fossil fuel subsidies by 2025 at the latest. It is also pushing through ambitious new rules to crack down on methane pollution in the energy sector.

Richard Folland, head of Policy and Engagement at Carbon Tracker says there is a clear disparity between political pledges to the Paris Agreement and fossil fuel subsidies: “There is a clear disparity there, despite G7 declarations, things have gone in the opposite direction. Whatever emerges out of COP 28 will send a strong signal to investors. The sort of thing we are all looking for is a clear commitment from governments on phasing out fossil fuel subsidies.

"The EU has iteratively proven its position on fossil fuel phase outs. In Sharm el Sheikh all of them couldn’t come behind it but now they have a clear position on phasing out fossil fuels, we know that there are still disagreement inside the EU but it should definitely at in the forefront of arguing for tangible action” he predicts. Folland is more sceptical of the stance taken by countries such as the UK and Norway and warns that their backing for new oil and gas projects was sending mixed signals to investors.

"We know that there are still disagreement inside the EU but it should definitely be at the forefront of arguing for tangible action."

A potentially even more powerful indicator that things might be changing was a meeting between US president Biden and Xi Jinping just weeks ahead of the COP 28 summit. While the leaders of the world’s biggest CO2 emitters did not yet commit to ending fossil fuels, they agreed to scale back methane emissions.

Another factor which so far has received relatively little coverage is the impact of rising interest rates on subsidy packages. State backing for the energy sector is extraordinarily expensive, as last year’s $2.2 trillion in fossil subsidies for the US alone and the $369 billion Inflation Reduction Act illustrate.

Next year, a record $8.2 trillion in US government debt will mature and be refinanced at significantly higher rates. Governments across the globe will face a similar predicament. With the cost of borrowing skyrocketing, this might dampen their appetite to fund energy industries of any kind, be it fossil fuels or renewable energy.

Investment risk

This raises questions on whether fossil fuel subsidies could be scaled back sooner than markets think and if investors in fossil fuels still riding the wave of easy money could be in for a hard landing.

Climate risk modelling scenarios such as those conducted by the European Central Bank and the European Systemic Risk Board (ESRB) form the basis of climate risk modelling for European Pension Fund Portfolios. Their risk modelling scenarios are based among others on a sudden sharp increase in carbon prices, for example through the introduction of carbon taxes.

But carbon pricing could also rise implicitly through a scale back of government backing. The IMF, which positions itself as an advocate of “free market economics” has positioned itself against fossil fuel subsidies. It says that raising fuel prices to their “fully efficient levels”, in other words, to cut all subsidies, could lead to a stark drop in emissions to 43% below baseline levels in 2030. This could not only put the world on track to meet the targets set in the Paris Agreement, but could also raise $4.4 trillion, 3.6 percent of global GDP, in revenue by the end of the decade. In a world of easy money, governments across the globe have been unwilling to heed its recommendations. But this might change as the cost of borrowing rises.

The latest climate stress tests conducted by the ECB and ESRB warn that European Insurers and Pension Funds are exposed to a series of interlinked climate risks, from sudden surges in carbon prices to heightened default risks which could be accelerated by increased physical effects of climate change. In the event of a disorderly transition, insurers and pension fund could see up to a quarter of their asset values being wiped out, the European finance watchdogs warn. These financial damages could be mitigated in the event of an orderly transition.

In a polarised world, the future for fossil fuel subsidies remains uncertain. But given the scale of potential damages, investors might do well to position their portfolios to the energy transition ahead of policy announcements, rather than reacting to them.

This article has been produced with additional contributions by Thomas Helm.

Also read:

COP 28 and fossil fuel subsidies: Will history repeat itself?