The silence score: how active are the world’s biggest investors on climate stewardship?

NZI takes a closer look at the stewardship practices of some of the world’s biggest investors in fossil fuels – and finds significant differences

“Stewardship? What is stewardship?” Asked a receptionist at one of the world’s largest asset managers, in an indifferent tone. Her lack of interest chimed with that of the company she worked for. Despite being one of the biggest investors in fossil fuels globally, very little information about the firm’s engagement with such companies is disclosed to the public.

In contrast, other major investors in fossil fuels employ dozens of people to engage with the companies they invest in and produce detailed stewardship reports. But does the production of glossy brochures on stewardship truly signify more action on climate change?

In the first instalment of the Silent Majority Series, we shone a spotlight on some of the biggest investors in fossil fuels. We now take a closer look at their stewardship track record over the past year, based on their 2022 Stewardship Reports, to highlight the varying degrees of engagement on climate with the companies they invest.

No disclosures – firms swimming naked on climate risk?

Perhaps the most extreme case is Berkshire Hathaway, which invested an approximate $40bn in the energy sector since the beginning of the year alone, including a 25% stake in Occidental Petroleum, the firm also owns 7% in Chevron. This is in addition to its existing exposure through holding company Berkshire Hathaway Energy.

Despite this significant allocation to fossil fuels, only one paragraph in the group’s annual report has been dedicated to its management of climate risks and the firm does not disclose individual voting or engagement decisions.

Similarly, Geode Capital Management, a US asset manager with more than $1 trillion in assets provides only very limited information on its proxy voting stance, the word climate change features neither in its proxy voting policy nor its two-page stewardship report.

Could a lack of climate reporting and engagement leave these firms swimming naked when the tides are rising?

Meanwhile, most large asset managers, from State Street over Vanguard to BlackRock, produce annual responsible investment reports which in between 60 to 150 pages lay out in depth how much the company in question cares about the planet and what it has done to engage with companies it invests in. But does this amount to more ambitious action on climate change?

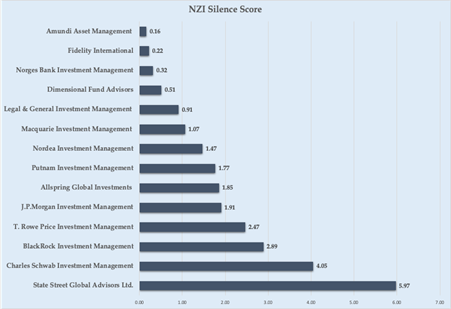

Relative silence score

Based on the company’s AUM and the number of its climate-related engagement activity, Net Zero Investor developed relative Silence Score which offers an indication where the company in question stands on engagement. This score has been standardised to correct for outliers and emphasise the relative placement of the company compared to its peers.

Higher scores indicate lower levels of engagement activity in relation to the company’s size.

For example, Capital Group, which is one of the ten largest investors in fossil fuels and has $2.2 trillion in AUM, has reported less than 200 engagements on environmental issues last year, compared to Norges Bank, which manages $1.3 trillion but has reported more than 800 climate related engagements.

BlackRock, the biggest investor in fossil fuels, scores relatively high when it comes to the levels of engagement. The firm, which manages $8.5 trillion in assets (by the end of 2022) and has reported more than 2000 incidents of climate related engagement last year.

But this measure comes with three disclaimers. First, definitions of climate related engagement vary significantly between firms.

State Street and Invesco for example report 331 and 215 incidents of engagement on environmental matters respectively but do not break these down to climate related subjects. This also applies to Vanguard, which reports 1,802 counts of engagement but it is unclear how many of those are related to environmental or climate issues.

BlackRock on the other hand specifically counts climate related engagement and only counts in-person interaction. For this Score, we counted climate and environmental – in person engagement.

This leads to an overestimation bias for companies which have only disclosed broader environmental engagement, we have indicated this with a “*” sign.

Excluding the companies who have only provided limited information, the results look somewhat different.

Second, this Silence Score does not include companies who haven’t filed any stewardship and engagement information on climate change. This includes Vanguard, the second largest investor in fossil fuels.

Similarly, Fidelity Investments, the third largest investor in fossil fuels is also missing from the picture as it has not disclosed climate related engagements in its 2022 stewardship report. In comparison, Fidelity International has revealed these figures and scores second.

Third, and perhaps most importantly, a high level of engagement does not necessarily mean a high level of commitment to tackling climate change. Firms could always be voting with the board and still score high on the Silence Score.

The score is based on publicly available information, largely disclosed by the companies themselves, it is therefore by no means perfect. But based on these measures, some significant differences between asset managers can be revealed that might not immediately transpire from their detailed stewardship reports.

Backing the board

These figures obscure several crucial facts. One, it doesn’t consider the investment focus of the manager in question. An active manager may have a lower engagement count because it has already limited its exposure to some fossil fuel heavy companies, the same applies to managers offering more indices with a low-carbon tilt. Similarly, managers with more fixed income products will by definition have a lower engagement count.

But more crucially, voting at an AGM does not imply voting for more ambitious climate targets. When seen through this prism, the voting track record of managers looks very different.

BlackRock voted with the board in 99% of all instances. It is still relatively more likely to support shareholder proposals on environmental issues than on social and governance issues. Out of 119 shareholder proposals on environmental issues filed last year, BlackRock backed 28 and rejected 91.

Similarly, Vanguard backed only 9% of environmental shareholder proposals in the US and none in Europe, the UK, Australia or Asia. It also voted with the board on all environmental proposals filed in Europe, the UK and US. Similarly, State Street voted on 4,490 shareholder proposals, but in 90% of all occasions, it rejected them. At the same time, it backed 83% of all management proposals.

In contrast, Amundi, scored relatively well on the Silence Score, backed 87% of shareholder proposals on climate and took quite an active stance in pushing for more ambitious climate targets among some of the world’s largest banks and fossil fuel companies. This also applies to LGIM, which rejected more than 66% of the “Say on Climate” proposals put forward by companies themselves.

Norges Bank’s Investment Management division scored high on its overall engagement count, but opposed only 6% of board proposals, which is similar to Capital Group, who rank lowest in terms of engagement count.

A trend towards disengagement?

What transpires from the 44 stewardship reports we ploughed through is that while there has been a growing number of shareholder proposals on climate, investors have become less likely to back them. In 2021, BlackRock supported 285, almost half of all shareholder proposals globally, this dropped to 133 in 2022.

BlackRock said that while it assesses proposals on a case-by-case basis, it is more inclined to back proposals based on enhanced disclosure standards and likely to object to proposals “intended to micromanage companies.”

According to BlackRock, examples of shareholder proposals that were too specific include demands to cease the financing of traditional energy, requiring the alignment of business models with 1.5⁰C scenarios and setting absolute scope 3 GHF emission reduction targets.

This sentiment is echoed by asset managers across the board. Vanguard for example observed: “a trend toward more prescriptive requests in such proposals dictating the pace of a company’s climate transition strategy or asking a company to exit a business line or otherwise change its strategy” the group said in its annual stewardship report. Consequently, the firm did not support any shareholder proposals on climate change in 2022.

This even applies to LGIM, which is ranked as a relatively active manager on the NZI Silence Score. The investor had in the past backed Follow This Resolutions at major oil and gas firms but opted to reject them this year.

Speaking to Net Zero Investor, Michael Marks, head of Stewardship at LGIM, said that the Follow This Resolutions filed at oil and gas firms this year were not the same as those in previous years. “The resolution this year was much narrower and very specific in the expectations of those companies” Marks argued.

But he also argued that this didn’t change LGIM’s direction of travel on climate change engagement more generally: “We are not here to run the companies, as shareholders that is not our responsibility. We are here to call out areas of concern, areas where we expect boards to be focused on and holding executives to account and we felt that the follow this Resolutions were too specific in the expectations of those companies.”

“We are not here to run the companies, as shareholders that is not our responsibility."

“A rueful situation”

Yet this suggestion was vehemently denied by Ursch McKenzie, head of Legal at Follow This, the group said it had worked closely with asset managers in drafting the text.

“Our request does not differ significantly from previous years; in fact, this year we have only requested Scope 3 medium-term targets while previous year requested Scope 1, 2 and 3, short-, medium- and long-term targets.

McKenzie argued that trend towards describing shareholder resolutions as too prescriptive meant that companies were effectively absolved from mitigating their contribution to climate change: “It is a rueful situation that investors decry our proposals as too prescriptive. Our request is straight-forward and clear, while leaving the choice of strategy for how to reach these targets up to the company. We simply request that the company align its targets with the goals of the Paris-agreement” he stressed.

"The high oil prices brought on by the exacerbation of the energy crisis resultant from Russia’s invasion of Ukraine, has resulted in investors being unwilling to sacrifice the short-term profits those high prices enable. "

He also suggested that higher oil and gas prices were instead the decisive factor in driving the lack of investor support.

“The underlying rationale, which cannot be stated explicitly by investors, is that the high oil prices brought on by the exacerbation of the energy crisis resultant from Russia’s invasion of Ukraine, has resulted in investors being unwilling to sacrifice the short-term profits those high prices enable. What they seem to miss is that they can still garner these short-term profits while maintaining pressure on companies to make the necessary adjustments to their strategies in the medium- and long-term” he stressed.

Asset managers in turn make the case that more ambitious shareholder proposals on climate change do not address a “material business risk” for the underlying companies. This stance differs significantly from that put forward by asset owners, who have campaigned for more ambitious climate targets.

Also read

Who are the silent majority?